US Dollar Weekly Forecast: The hunt for 100.00

- The US Dollar ended the week in quite a positive mood.

- Solid NFP results eclipsed steady uncertainty around the Middle East.

- Markets now expect the Fed to hike rates by 25 basis points in December.

The week that was

A quite promising week saw the US Dollar (USD) trade with gains on almost every day, while the outstanding Nonfarm Payrolls (NFP) figures released on Friday lifted the US Dollar Index (DXY) to new two-month highs near its psychological 100.00 barrier.

Indeed, the post-NFP jump also sent US Treasury yields bouncing, pushing maturities to multi-day tops across the curve, as market participants have now started to pencil in around a quarter-point interest rate hike at the Federal Reserve’s (Fed) December event.

Now, about geopolitics. The hopes of a US-Iranian deal that could eventually reopen the Strait of Hormuz and, with it, gradually normalise global shipping flows have started to dwindle, and they remain mired in the never-ending uncertainty stemming from the White House and the Iranian regime. No surprises there.

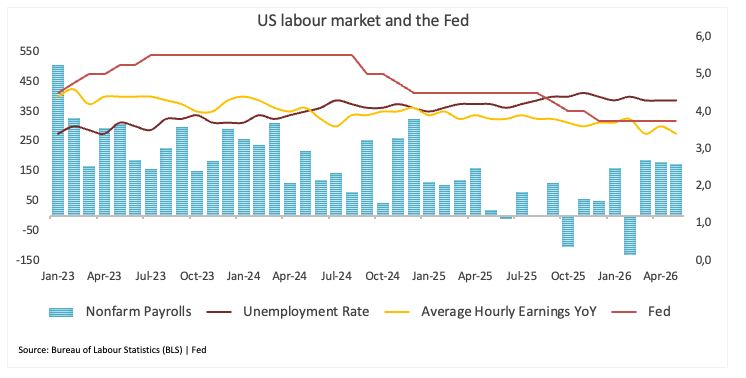

On the data front, the week was exceptionally successful: both manufacturing and services, as measured by the Institute for Supply Management (ISM), exceeded consensus in May, while the labour market shone brightly after stronger readings from the ADP report, JOLTs job openings, and NFP.

Yes, US exceptionalism is back.

The debate is shifting: Are rates restrictive enough?

If there was one common thread running through this week's barrage of Fed speakers, it was that inflation remains the central concern, even as policymakers acknowledge that the economy continues to hold up remarkably well.

The labour market, despite showing signs of moderation, still widely views itself as being in balance. Several officials pointed to stable employment conditions and a lack of meaningful deterioration in hiring trends, reinforcing the view that the US economy is far from slipping into a recession.

That resilience is precisely what is complicating the inflation battle.

Beth Hammack (Cleveland) noted that inflation remains too high and continues to move in the wrong direction, although she stressed that inflation expectations have not yet shown signs of becoming unanchored. She also highlighted the resilience of businesses and households despite tariffs, geopolitical tensions and the prolonged conflict in the Middle East.

Those geopolitical developments were a prominent theme in the week's remarks. Officials repeatedly acknowledged that higher energy prices are feeding into inflation pressures, while uncertainty surrounding the conflict continues to cloud the policy outlook.

John Williams (New York) argued that inflation has risen "quite a bit" in recent months, driven by a combination of energy costs, tariffs and growing demand linked to artificial intelligence. Even so, Williams remains relatively comfortable with the current policy setting, describing interest rates as being in the right place and signalling little urgency to move in either direction.

Not everyone sounded quite so relaxed.

Lorie Logan (Dallas) warned that policy may not be restraining the economy as much as many assume, pointing to strong corporate earnings, accommodative financial conditions and resilient economic activity. Against that backdrop, she suggested that we cannot rule out additional rate increases later this year.

Jeffrey Schmid (Kansas City) echoed a similar sentiment, saying inflation remains the biggest threat to the economy. He openly raised the possibility that the Fed may eventually need to tighten policy further if price pressures fail to ease, while reiterating the importance of maintaining the credibility of the 2% inflation target.

Taken together, the message from Fed officials was not one of imminent action, but neither was it one of comfort. Policymakers continue to see an economy that is growing, a labour market that remains healthy and inflation that is proving stubbornly persistent.

Bottom line: The Fed still appears content to sit on the sidelines for now, but the conversation is no longer centred on rate cuts. Increasingly, officials are debating whether policy is restrictive enough and whether inflation could eventually force them to do more rather than less.

Speculators are watching closely, still unconvinced

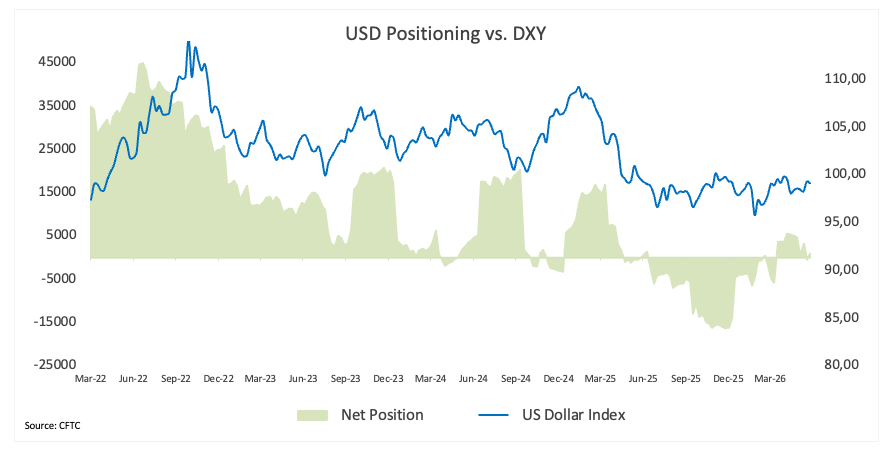

According to the latest data, non-commercial players shifted to net longs on the US Dollar, resuming the trend that kicked in back in mid-March and rapidly reversing the previous week’s hiccup. Indeed, speculative net longs rose by 850 contracts for the week ending May 26, according to the Commodity Futures Trading Commission (CFTC).

In addition, open interest went up for the second consecutive week, reaching the highest level since early December 2025 at nearly 42.3K contracts.

There appears to be a consolidative trend between 97.50 and 100.00 for now. If the idea of a rate hike at some point in Q4 begins to gather serious traction, along with persistently healthy fundamentals, USD-bulls could regain conviction and start tilting the scales toward a more sizeable net long positioning and thus reinforce the case for a higher Greenback in the months to come.

Price pressures are making an unwelcome comeback

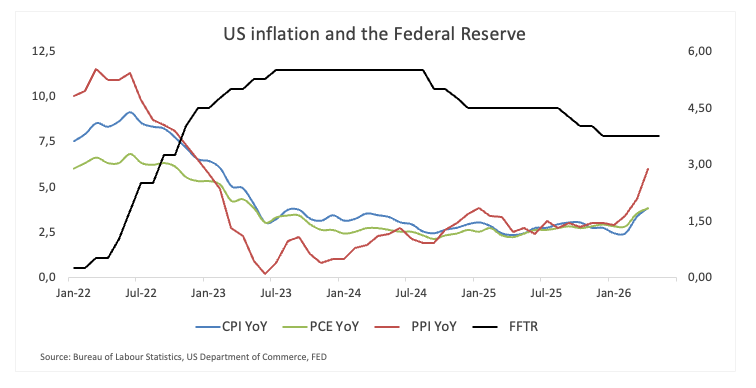

As widely anticipated, inflation picked up notably in April.

Headline Consumer Price Index (CPI) inflation accelerated to 3.8% YoY from 3.3% in March, while core CPI, which strips out food and energy costs, rose to 2.8% from 2.6%.

The latest figures raise an uncomfortable question for policymakers and investors alike: what if the disinflation story that dominated the first part of the year is already beginning to lose momentum?

A renewed surge in Oil prices following the continued closure of the Strait of Hormuz has added fresh inflationary pressure to the mix. At the same time, the delayed effects of US tariffs are only now starting to work their way through supply chains and into consumer prices.

Taken together, it is exactly the kind of backdrop markets were hoping to avoid: inflation proving stubborn just as the economy continues to show remarkable resilience.

The next test for markets

Attention now turns to next week's Consumer Price Index (CPI) report.

Markets will be watching closely to see whether the data confirm the message that inflation remains uncomfortably above the Fed's 2% target and may stay there for longer than previously expected.

Beyond the data, investors will continue to track developments in the Middle East, the trajectory of Oil prices and the situation around the Strait of Hormuz, all of which are increasingly shaping expectations for monetary policy.

Fed speakers have entered the blackout period ahead of the June 17 meeting, where the central bank is expected to keep its steady hand, adding to rising bets that rates could stay elevated for much longer than initially thought.

Has the market underestimated the Fed?

For most of 2026, investors operated under a relatively simple assumption: the Fed’s next significant move would eventually be towards lower interest rates.

That view is becoming increasingly difficult to defend.

Sticky inflation, resilient economic activity, higher energy prices and renewed supply-chain disruptions have all complicated the path back towards policy easing. Perhaps more importantly, Fed officials no longer appear fully convinced that inflation will continue drifting lower without additional help from restrictive policy.

None of this necessarily points to an imminent rate hike.

It does, however, suggest that the hurdle for rate cuts has risen considerably.

For the US Dollar, that matters.

Higher-for-longer rates should continue to underpin Treasury yields and offer support to the Greenback.

Should inflation remain elevated and energy markets continue to face disruptions linked to the Middle East conflict, a return above the psychological 100.00 level could become a realistic scenario sooner rather than later.

The final mile remains the hardest

If there is one lesson from recent months, it is that bringing inflation down from very high levels is often easier than eliminating the last stretch of price pressures.

For now, that may be the Dollar's biggest source of support.

Markets may simply have underestimated how difficult the final phase of the inflation fight was always going to be.

Technical Analysis

In the daily chart, Dollar Index Spot trades at 100.02. The near-term tone is bullish as price holds above the 55-day, 100-day and 200-day simple moving averages clustered around the mid-98s, reinforcing a constructive backdrop after reclaiming the 99 handle. Momentum is strong, with the Relative Strength Index at 65, leaning toward overbought territory, while a modest Average Directional Index reading near 21 suggests the uptrend is developing but not yet extended.

On the topside, initial resistance is located at 100.64, ahead of a more significant barrier at 101.98. On the downside, immediate support emerges at 99.50, followed by the 55-day SMA around 98.96 and the 200-day and 100-day SMAs near 98.62 and 98.56 respectively; below these, further cushions sit at 97.62 and then deeper supports at 95.56, 95.14 and 94.63.

(The technical analysis of this story was written with the help of an AI tool.)

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.