Week ahead – Fed countdown begins amid US inflation data and geopolitical risks

- Fed Chair Warsh’s first meeting approaches as key US inflation data could reshape expectations.

- Oil prices remain elevated as US-Iran talks continue; tariffs also return to the spotlight.

- ECB is expected to hike; will it be a one-off move or is July live?

- BoC to stand pat, aussie eyes Chinese CPI data, while the yen awaits the BoJ meeting.

- Strong US data could keep the dollar supported; euro may suffer if ECB adopts a balanced tone.

Fed meeting in sight but risk events linger

The countdown to the biggest event of the year so far, the first Fed meeting under Chair Warsh on June 17, has officially commenced. Next week’s key events could serve as the best appetizer for Warsh’s first press conference, although market participants will probably be distracted by developments elsewhere.

The fresh hostilities in the Middle East put a temporary pause on the prevailing optimism, but there is still lingering hope for an initial US-Iran deal, which addresses Iran’s nuclear future at a later date. Notably, US President Trump even allegedly disagreed with the Israeli PM Netanyahu as the latest Israeli operations in Lebanon threaten the agreement with Iran.

Oil prices remain elevated, but investors are reacting more calmly to headlines. That said, hopes for a swift drop in oil prices look baseless as it would require a full normalization of oil supply routes that could take months to achieve even if an agreement is announced today.

Meanwhile, the US administration has announced its intention to replace the 10% global tariff imposed under Section 122, which expires in July, with new Section 301 tariffs. The new levies will vary between 10%-12.5%, with China, India, Japan and South Korea facing the higher proposed rate. These levies are expected to commence during July, following a country-by-country review.

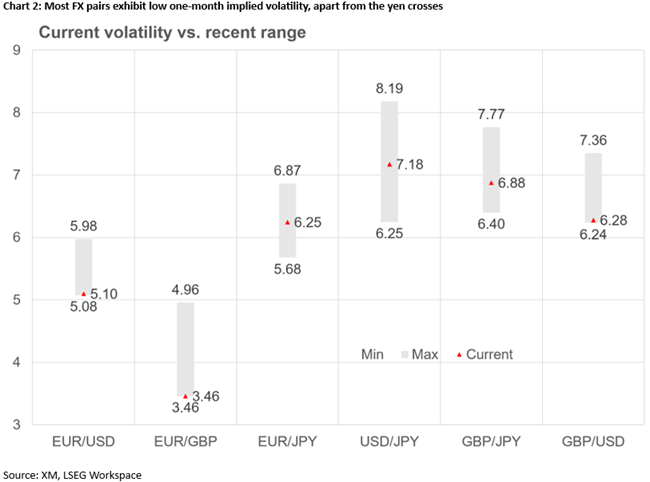

Surprisingly, market volatility remains relatively subdued across the asset classes. In particular, the one-month implied volatility for both euro/dollar and gold has crashed to the lowest level since mid-January, while the S&P 500 volatility has also been edging lower, almost reaching February’s levels. On the other hand, yen pairs and the Nikkei 225 index are experiencing increased volatility ahead of the critical BoJ meeting.

Pivotal US data releases

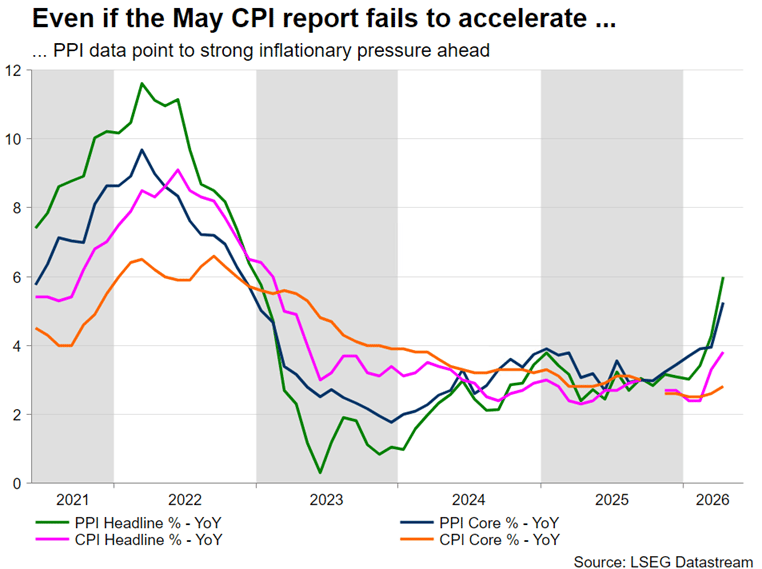

This calmer volatility profile could materially change next week as the June CPI and PPI reports on Wednesday and Thursday respectively will be in the spotlight. Very early forecasts point to another acceleration in both the headline and core CPI indicators to 4.2% – the highest level since June 2023 – and 3% respectively, sending shockwaves across markets.

While an elevated inflation report could be seen as temporary by Fed doves, the producer price figures remain a real headache. The headline year-on-year indicator is seen jumping north of 6.5%, the highest level since January 2023, and likely opening the door to further CPI acceleration given the lag between the two reports. Notably, the likely stronger inflation prints might be followed by another record low reading in Friday’s preliminary University of Michigan Consumer Confidence index, causing alarms about consumer spending.

Confirmation of these early forecasts might not materially increase the chances of a hawkish meeting the following week, but it will surely seriously complicate Warsh’s first few weeks on the job. The new Chair was selected by Trump due to his dovish credentials, but it will be difficult for Warsh to ignore the ballooning inflationary pressures. At his May confirmation hearings, he insisted on the need to restore Fed credibility and shrink the balance sheet, raising questions about his true colours.

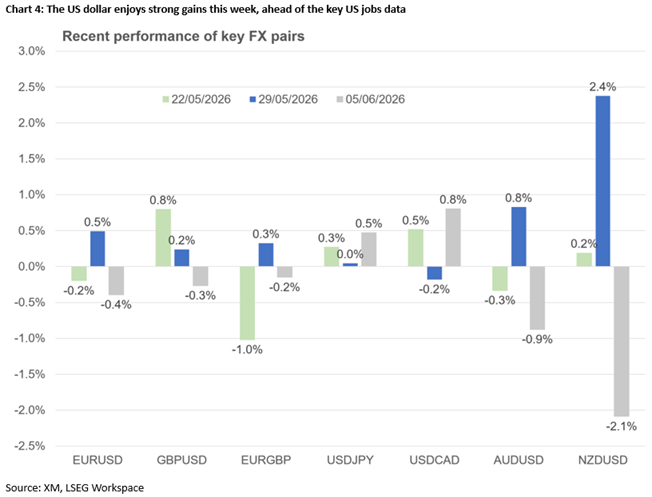

The US dollar has been the protagonist of the week. With Trump apparently opting for a muted tariff strategy, the dollar might yet prove more resilient than forecast. A US-Iran resolution would push euro/dollar higher, but the favourable yield spread, the continued equity inflows and the strong economy could shield the dollar from posting significant losses. If the Fed opts for a more hawkish stance, on the back of strong inflation prints, then the dollar might enjoy a strong June.

ECB to hike but will it remain hawkish?

Alongside the US data, Thursday’s ECB meeting could increase expectations for a more hawkish Fed meeting. President Lagarde et al. are widely seen announcing the first rate hike since September 2023, essentially acknowledging that the adverse scenario is materializing. An agreement reopening the Strait of Hormuz would be welcomed by ECB members but will not be sufficient to pause Wednesday’s rate hike.

Additionally, based on the ongoing commentary from ECB officials, the discussion at the ECB tower in Frankfurt will also evolve around the severe scenario, which, in principle, could justify a series of rate hikes. A July rate hike will not be pre-announced, but Lagarde can easily guide expectations if the hawks demand such action, while a similar message could also be conveyed by the staff forecasts, if the 2026 headline and core CPI figures are revised aggressively higher. Consequently, the usual press conference will attract market interest, increasing the pressure on Lagarde to minimize her usual mistakes.

Despite the more hawkish ECB stance, the euro has been failing to rally aggressively against the dollar. A rate hike on Thursday might cause a brief euro appreciation only if it is accompanied by hawkish commentary. But even then, growth concerns could eventually dent euro appetite. What could materially change the euro’s outlook would be the end of the Ukraine-Russia war and the normalization of EU-Russia trade relations.

BoC meets, aussie eye key Chinese data and the yen hopes for a miracle

On Wednesday, the Bank of Canada is expected to stand pat, as the council is very worried about the weakening labour market and waning growth. The weaker April CPI report and the Q1 GDP figures cancelled any hawkish thoughts. The BoC’s mind will also be on the challenging US-Canada trade relationship in light of the USMCA review in July and the latest headlines about the US imposing a 10% tariff on certain imports from Canada.

There is also a busy schedule for the aussie, but only the June Westpac consumer sentiment survey could attract market interest. That said, disappointing CPI and PPI data from China on Wednesday could also prove market-moving. Both the loonie and the aussie could be on the wrong foot next week, adding to the decent losses already recorded.

Meanwhile, with dollar/yen hovering just below 160, it looks like the Japanese Finance Ministry has opted to wait until the BoJ meeting on June 16. If markets are not content with the expected BoJ rate hike and overall rhetoric, then the BoJ will be forced to intervene aggressively.

Equities pumped up, crypto market in disarray, gold shows some signs of life

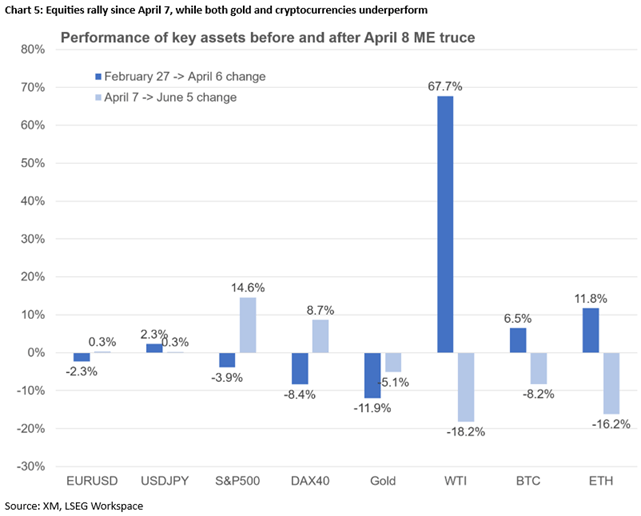

US equity indices continue to monopolize market flows and remain near their record highs. The AI frenzy has taken a small hit from Broadcom earnings, but it will take more than a mediocre report to dent appetite. That said, next week’s earnings announcements from both Oracle and Adobe, and the SpaceX IPO might add fuel to current concerns, with investors remembering overstretched valuations. From a trading perspective, the pace of the rally since late March has been exponential, rising 20% in just over two months. Hence, a correction might be necessary to strengthen the foundation of the current upleg. But are investors going to react maturely to a 5% drop towards the 7,000 area?

Finally, the situation is less rosy for gold. The precious metal remains almost exclusively driven by the US dollar, while also being marred by continued selling from countries aiming to support their currencies and/or replenish their lost oil revenues. An upside surprise in next week’s US data releases could support the dollar and materially undermine the current tentative signs of stabilization.

Author

Achilleas joined XM as an Investment Analyst in November 2022. He holds a BSc in Business Economics from Middlesex University and a MSc in Mathematical Trading and Finance from Bayes Business School, City University.