Waiting for Powell’s baton to drop

The Baton drop

Amid a relative dearth of market-moving inputs, today’s session was less about fresh catalysts and more about waiting for the conductor’s baton to drop. A weak Empire Fed survey was hardly a showstopper, yet both bonds( in price) and equities drifted higher, each leaning on the expectation that Wednesday’s Fed meeting delivers the first rate cut of the Trump era.

In traders’ minds, the cut is already written in ink — the suspense is whether Powell frames it as the start of a gentle easing cycle, or whether the Fed sees something sharper in the cards should the labour market crack faster than expected. The base case is clearly the former, but the latter can’t be dismissed, because the jobs data will always force the Fed’s hand in this cycle..

The surface looks euphoric: the S&P has surged past 6,600, while the Nasdaq strung together its longest winning streak since 2023. The spotlight, though, remains on a narrow cast — the Mag7 galloping higher, Alphabet swelling into the $3 trillion club, Tesla catching a bid after Musk’s billion-dollar stroke of the pen. Meanwhile, the S&P 493 lags, the Dow can barely hold green, and breadth thins with every step up the staircase. It’s a market held aloft by a handful of giants, which makes the heights both dazzling and precarious.

Rates, for their part, eased 2–3 basis points across the curve — a nod to growth concerns as much as dovish policy. The dollar slipped to two-month lows, and traders fled toward the usual refuges and continue to embrace “ Anyting but the Dollar”.

Gold blasted into new record highs, fueled not just by a weaker greenback but by persistent whispers that China is buying multiples(10X) more than it officially discloses.

-638935711220660324.jpg)

H/T Shanghai Futures

When China is stockpiling gold at record levels ( and 10 X the reported level), it tells you everything you need to know. The world’s second-largest economy isn’t scrambling for shiny inert metal out of some cultural fascination with jewelry. They’re hedging against fiat dilution, plain and simple. When central banks and governments flood the system with liquidity, when debt towers over GDP, and when the reserve currency itself is being leaned on to fund perpetual deficits, the logical escape hatch is tangible assets. Gold isn’t a relic here — it’s the insurance policy against the slow erosion of purchasing power. China is simply reading the same playbook every trader does: when trust in paper wanes, bars beat bonds and the dollar.

Why doesn’t China fully disclose its gold buying? Simple — they don’t want the price to run away from them any faster than it already is. Every ton they quietly slip into reserves is another chunk off the market, but the minute they trumpet the scale, they bid against themselves. Better to buy in the shadows, let the market stay complacent, and keep accumulating before the rest of the world catches on. But now that the cat is out of the bag, is $3800 on the cards sooner than expected?

Oil, meanwhile, paused in consolidation after last week’s whipsaw, neither breaking nor buckling. Bitcoin had its latest bout of nausea before steadying, a reminder that liquidity floods lift all boats, even the leakiest ones.

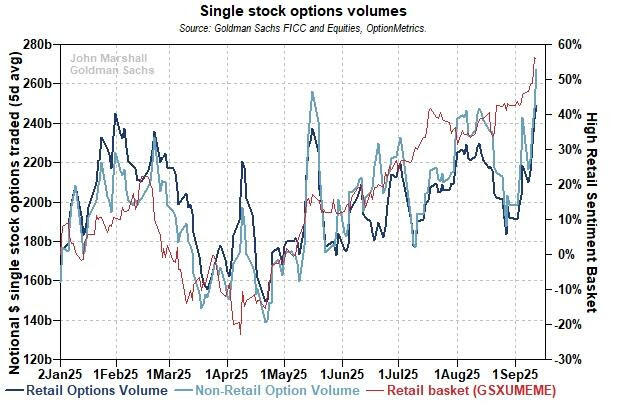

The retail crowd has led the party too, with flows into NDX and SPX accelerating through September. Often dismissed, retail has proven a leading indicator throughout most of this cycle, and right now, they are shouting conviction from the rafters.

H/T Goldman Sachs

That faith could be tested this week: Powell’s tone, the dot plot, and any reference to inflation being “anchored” or labour “weakening faster than expected” will dictate whether the rally stretches further or stalls out. The market wants speed; the Fed may prefer caution.

History tells us the first cut after a pause can cause a market hiccup, as investors ask what the Fed sees in the shadows. But longer-term patterns are bullish — the S&P has typically gained double-digits a year out. The risk is that markets have already front-run too much of that optimism, with volatility gauges flatlining as if turbulence were impossible.

The real story is one of concentration and complacency. The Mag7 continue to pull the cart while the rest of the market shuffles behind, yields drift lower as though recession risks are comfortably managed, and gold shines brightest when confidence should be highest. This is the tension heading into Wednesday — the orchestra warming up, the audience leaning forward. Powell’s baton comes down next, and the market’s performance will depend on whether he plays a lullaby or a requiem.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.