Wages and Productivity

The US monthly employment data has been the single most important high frequency economic report. It was a key in the recession of the Great Financial Crisis, and it was an important metric of the recovery.

Recent reports have been distorted by the storms in late Q3 and early Q4. September jobs growth fell to 18k and October bounced back to 261k. Before the distortions, this year's average, through August, was 176k, nearly identical with last year's average of 187k. Economists expect nearly 200k net new jobs were created in November.

Job growth, unemployment and underemployment have moved more than the Fed had expected. The focus since earlier this year has been on the easing of price pressures. In the traditional thinking, headline inflation converges to core inflation, and core inflation converges to wage growth. Average hourly earnings are reported with the non-farm payroll data and interest in it seems to be overshadowing the job creation or unemployment metrics.

Average hourly earnings may have been distorted by the storms, as well. They were unchanged in October and are expected to have risen 0.3% in November. Hourly earnings were flat last November, so due to the base effect, the year-over-year pace will match the November 2018 monthly increase. It is expected to accelerate to a 2.7% pace from 2.4% in October. This probably overstates the case and the December comparison will be more difficult (December 2016 average hourly earnings rose 0.3%). Over the past 24 and 36 months, the average year-over-year pace of hourly earnings is steady after having gradually risen to stand at 2.5%-2.6%.

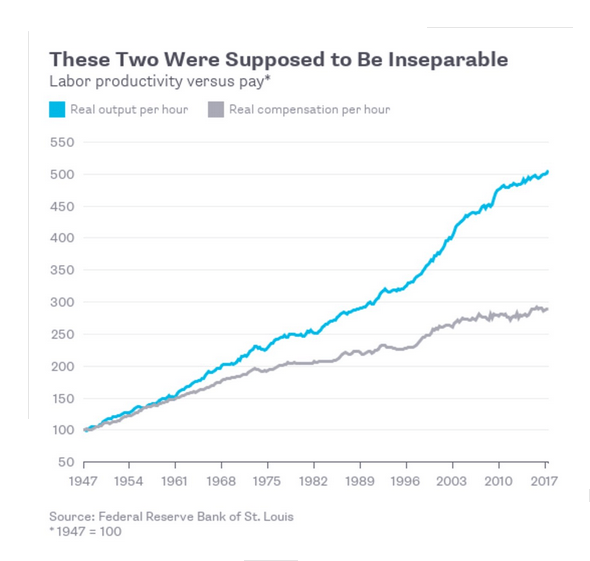

In the broad discussion of economics and politics, the divergence between earnings growth and productivity has been grist for the mill. Since 1980, productivity growth has doubled while some measures of compensation have increased by only 50%. The divergence appears to have begun in the late 1960s.

This Great Graphic, from data by the Federal Reserve of St. Louis was in a recent article by Noah Smith, an assistant professor of finance at Stony Brook University, and a columnist for Bloomberg. It shows the yawning divergence.

Professor Smith says in big bold letters on the top of the chart that "These two were supposed to be inseparable." Really? They did move tightly together after WWII, but what does "supposed to be" mean?

They are not linked by any natural or people-made law. It begs the question of what determines wages. Employers are under no compulsion to distribute the productivity gains to employees. They may do so under certain conditions, such as competition from other employers, or as a concession in negotiations with labor.

Some observers attribute the divergence of compensation and productivity to the integration of China into the world economy. However, the divergence takes place well before China began modernizing in the late 1970s. It did not join the WTO until 2001. The same temporal misalignment seems to rule out the fall of the Soviet Union and the integration of eastern and central Europe, and Russia in to the world economy.

Smith draws on recent work by Summers and Stansbury to argue that short-term changes in productivity are correlated with better pay. He concludes, "It's wrong to say that raising productivity won't raise wages-if history is any guide, it will." Indeed, productivity growth has been abysmal (negative) in some quarters and average hourly earnings have surpassed it.

Smith, however, cannot get away from his teleological argument, and asks, "why didn't wages rise as much as they should have." There is no should have. Still, he recapitulates the usual arguments, like wage inequality (and the difference between average and median). However, claiming that wages did not rise as fast as they "should have" because some wages rose slower than others is not particularly helpful.

He cites technological changes, but that too does not line up with the chart and the beginning of divergence. Consider, for example, that today's smart phone has more computing power than the lunar module that landed on the moon in 1969 as the divergence began. He also notes that the weakening of labor's bargaining power as another possible cause as is the near monopoly power of some employers (monopsony). He is open to the possibility that some combination of factors is at work.

Growth can be thought of as a function of two things. How many hours are being worked and output per hour. Rising living standards have been driven by these two forces. Over the long-term, rising living standards are only possible with rising output per hour, or productivity. Those productivity gains are a function of labor and capital (think equipment and technique). There is no iron law or tinfoil law that speaks to the distribution of productivity gains between wages on one hand and profits on the other hand.

Labor peace during WWII and in its aftermath (when the US remained on war footing, which was reinforced by the Korean War) was purchased through sharing the productivity gains with workers (primarily men). The government helped facilitate this through numerous measures, including encouraging unions. The decoupling of wages from productivity in the US began as American businesses faced stiffer competition from the recent rebuilding of the European and Japanese economies. Facing rising cost of capital and inputs, capital broke what some economists, political scientists and sociologists call the "social contract," and grabbed more of the productivity gains.

However, the social contract was not a contract in any meaningful way. Simply put, it worked in capital's favor to share the productivity gains with male employees until it wasn't and when it wasn't, capital went on an offensive. It sought regulatory relief, including the deregulation of the capital markets and the weakening of organized labor. It enlisted the government's help with this agenda. As the chart illustrates, the divergence between wages and productivity yawned as Reagan announced "Morning in America."

The decoupling of wages with productivity forced American households to adjust. The entry of women in the workforce in large numbers was over-determined (i.e., many causes), but it is not a coincidence that it took place when a men's wages no longer kept pace with productivity. Even women entering the workforce was not sufficient. In many middle-class families, adolescents began working part-time. Still, this did not prove sufficient. The "funding gap" was ultimately filled by credit.

The end of the credit cycle, which is the Great Financial Crisis, has not seen a new convergence between wages and productivity. The disparity in the distribution between the return to labor (wages) and capital (profits) is palpable. It remains one of the key political and economic challenges as next year commemorates the tenth anniversary of the onset of the Great Finance Crisis. For the first time, the Federal Reserve, the European Central Bank, and the Bank of Japan, as well as many other central banks, are advocating higher wage growth.

The skewed distribution of productivity gains is ultimately a reflection of asymmetries of power. It is not that no productivity gains are shared with employees; that is a straw man Professor Smith knocks down with his pen. However, unless compelled by an opposing power, there is no reason for employers to share more of the productivity gains with employees. Employers are no sooner going to give labor a greater share of the productivity gains than they are to unilaterally offer to boost the price they pay the providers of other inputs.

Author

Marc Chandler

Marc to Market

Experience Marc Chandler's first job out of school was with a newswire and he covered currency futures and Eurodollar and Tbill futures.