Vulnerable Yields and Fragile Oil

Bond yields were lower Tuesday as the market shrugged off gains on Wall Street, with Treasuries pricing in a very dovish spin following an expected 25 bp rate hike.

The WSJ editorial board joined Trump and recent Op-ed authors to plead with the Fed to remain on hold today. A solid rebound in housing starts and permits broke a data losing streak of late, though global stock market weakness helped quickly cap yields. Crude oil was crushed amid ongoing supply-demand imbalances, flagging risks ahead.

“Time for a Fed Pause” was the title of another op-ed piece in the WSJ after the close attributed to “The Editorial Board,” following hot on the heels of the Druckenmiller/Warsh pause piece the day prior. The WSJ likewise argued that there is no sign of inflation with the PCE deflator “falling for months,” the Dollar strong, growth slowing and commodity prices down. President Trump doubled down and tweeted earlier that he hopes “the Fed will read the WSJ Editorial before they make yet another mistake.”

Set against some 70% expectations of a hike, if nothing else, all this pressure on Powell and Co. increases risk of a more volatile market reaction to the decision, updated projections and presser tomorrow.

The erosion in stocks extended the drop in rates with the 2-year falling over 4 bps to 2.646%, while the 10-year dropped 3.4 bps to 2.8175%.

US Equities initially shrugged off copycat declines in Asia, while Europe closed just in the green.10-year Treasury Yields are down -0.2 bp at 2.816%.

Hence, this sputtering global growth, the external pressure on the Fed to halt rate hikes and ongoing trade/tariff concerns have continued to plague investors into year-end.

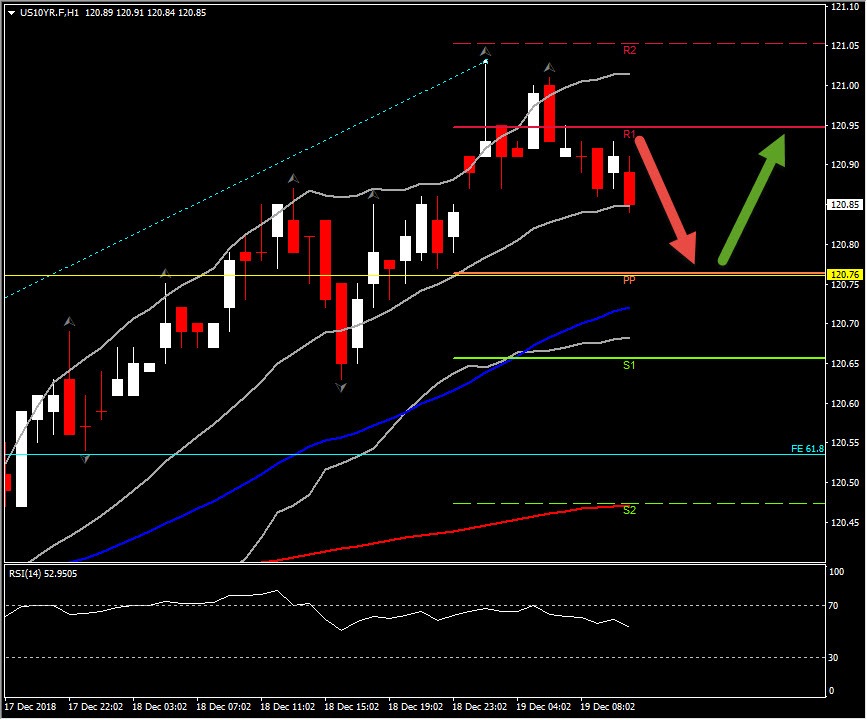

As Treasuries yields are vulnerable to a knee jerk selloff Wednesday, they led a broad rally in peripheral bond markets. The US 10-year bond future closed yesterday at 120.85, while today retested 121 level before reversing slightly lower. Intraday, the asset has 7 bearish hourly sessions and is currently at the 20-period SMA. Hence a closing below this level at the top of the hour could drive price to 120.70-120.76 Support area, which coincides with the PP for the day and also the 50-period EMA which provides good supports for the asset this week. Immediate Resistance is set at 120.95(R1) and next one at 121.05 (R2).

Hourly RSI also supports intraday weakness as it dive to 52 area from 70. The daily picture remains to a positive outlook, however RSI looks overbought at 74, therefore a possible correction could be seen in this 2-month rally.

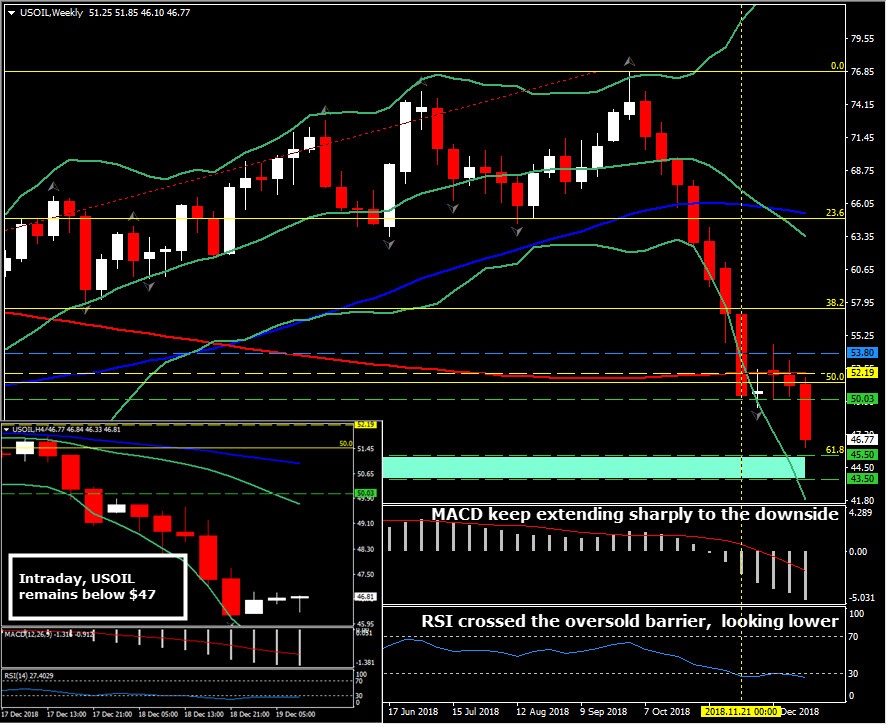

Meanwhile, the latest slide in oil prices, which saw the WTI future dipping briefly below USD 56 per barrel prompted some speculation that the Fed will call off the hike after yield decline. WTI crude futures hit a low of $46.10 yesterday, which is the lowest level seen since August 2017.

WTI crude plunged 7.4% to 15-mth lows near $46.10 amid ongoing supply-demand imbalances, along with China weakness and global growth slowing.

Global production remains at or near records, while expectations for falling demand growth in 2019 have weighed, as markets price in global economic slowing. Technically, as also mentioned in November 26 report,

“With the asset trading just a breath above the psychological $50 level, any intraday or in general any near-term correction, seems incapable of propping up the USOil prices. Hence as the overall picture remains strongly negative, the next medium term Support is around the 3-month lows during 2017 (May-July) and the 61.8% Fib. level, at $43.50-$45.50 area.”

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in