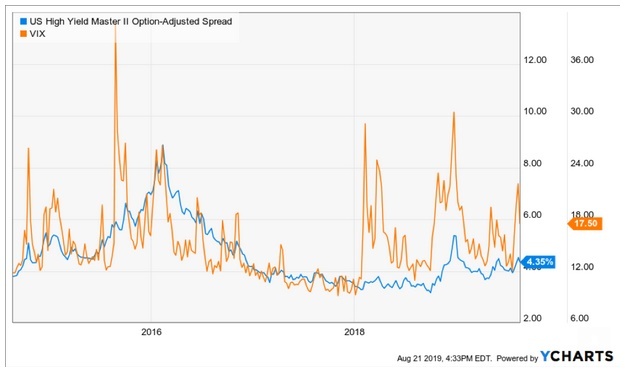

Volatility (VIX) dropped back to 15.91, falling over 9%

Highlights:

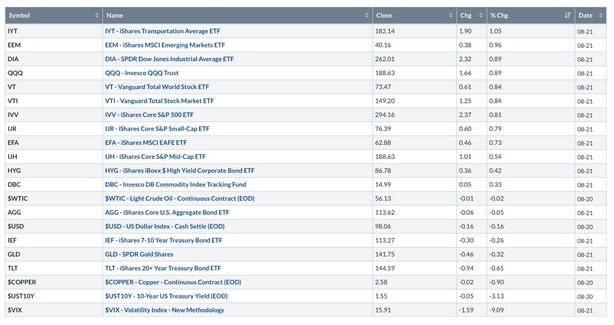

Market Update: Stocks bounced yesterday. Transports were the top performing segment, gaining over 1.05% on the day. Volatility (VIX) dropped back to 15.91, falling over 9%. U.S. 10-year yields dropped as well, pushing bonds up. The S&P 500 (IVV) finished higher by 0.81%.

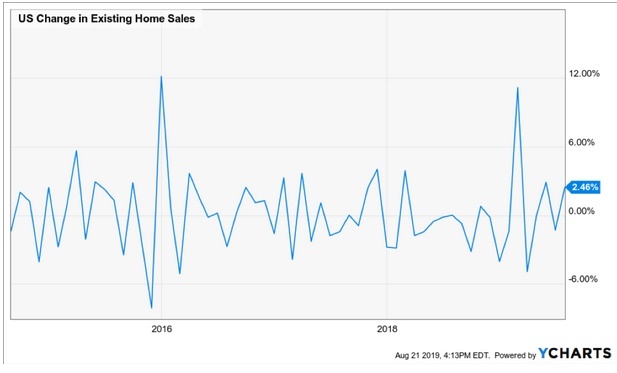

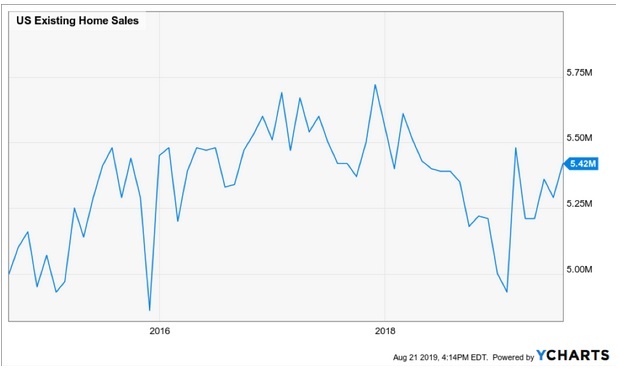

Economic Data: Existing home sales moved higher 2.46% month over month. Home sales are still down from the peak reached in late 2017. However, they have rebounded significantly from the lows set earlier this year. A rebound in the housing market would demonstrate a strong consumer and that could bode well from an otherwise faltering economy.

The Consumer: There was a lot of talk about the consumer yesterday on financial media. Those pundits that don’t want to admit that the economy is slowing, and has been slowing for some time now, are holding on to the consumer as their last hope for avoiding a potential recession. We wanted to take a look at the consumer through the lens of the market to see if the market agrees with the pundits. The top three sectors yesterday were consumer discretionary (XLY), retail (XRT), and homebuilders (XHB). Currently, only consumer discretionary and homebuilders are in positive trends relative to the broad market (SPY).

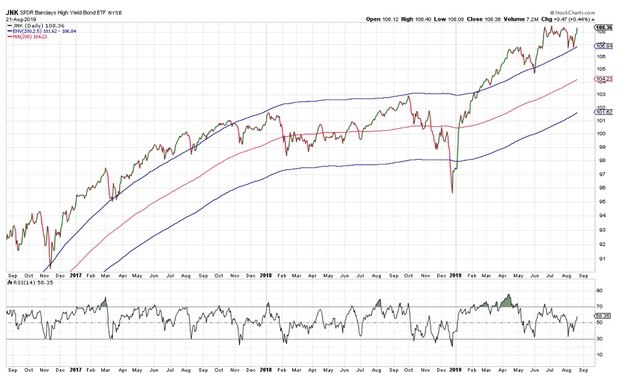

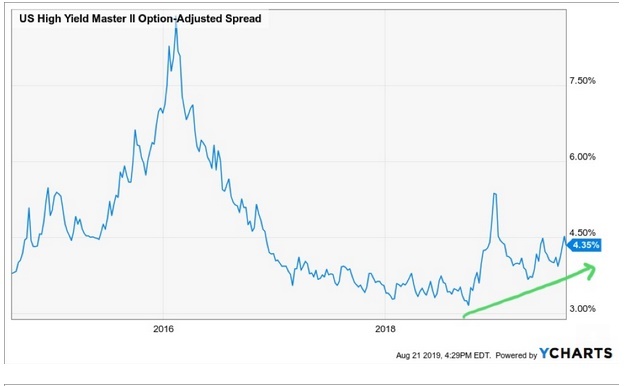

High Yield: The one area of the market that has been incredibly resilient to the slowing economy, growing trade war tensions, and geopolitical risks has been the high yield bond market. High yield bonds are close to moving to all-time highs and remain in a positive trend based on price alone. A breakout to new highs would be an encouraging sign for risk assets in general.

Spreads: Despite the strength in the high yield market from a price perspective, spreads have continued to widen since bottoming last year. They are still below the highs made in December of 2018, but they are making a series of higher highs and higher lows. Spreads widening can be leading indicator to future equity market volatility.

Futures Summary:

News from Bloomberg:

Stocks and Treasury yields fell as traders parsed European economic data and awaited Fed chief Jerome Powell's address tomorrow. Ten-year Treasury yields slipped to around 1.57% and U.S. equity-index futures tracked losses in Europe and Asia on below-average volume. The dollar nudged up. Gold dropped and oil advanced.

The euro-area economy unexpectedly perked up in August, though a meaningful rebound remains out of sight. The regional composite Purchasing Managers' Index rose to 51.8, indicating a slightly stronger expansion than in July. Manufacturing returned to growth in France, but the outlook for Germany remained bleak, with orders falling the most in more than six years.

The ECB will release minutes from its last meeting that may give clues on the size and shape of the stimulus package it's lining up for September. The central bank is expected to cut interest rates next month, but it's unclear by how much, Bloomberg Economics said. Mario Draghi has signaled asset buying will start again, but hasn't given details on the amount that will be spent or whether the ECB will alter the composition of the purchases.

Nordstrom jumped pre-market after second-quarter profit beat estimates, offering hope the department-store business model can survive. But the company said net sales will probably drop 2% this year and it narrowed its earnings guidance range. L Brands gave mixed news: Net income topped estimates and sales at Bath & Body Works rose more than expected, while Victoria's Secret missed.

Salesforce reports after the close and may show trade war resilience. With low exposure to China, it may not echo SAP with a negative view, Bloomberg Intelligence said. Demand from Europe will be in focus. HP Inc.'s results may be dented by tariffs and a mixed print supplies segment. VMware and Intuit are also up.

Author

Clint Sorenson, CFA, CMT

WealthShield