VIVE LA VOLATILITÉ

VIVE LA VOLATILITÉ

May 5, 2017

French Election: Landslide Macron victory prompts muted initial reaction from euro

In reaction to our recent Q1 Commentary, there understandably continues to be questions surrounding the confounding lack of volatility and complacency that has pervaded global markets, despite the widespread distress gripping the global geopolitical arena. Many market participants and those watching from the sidelines have been left dumbfounded watching the VIX (Volatility Index) meander around 90-year lows, while at the same time, the number of Google searches for World War III (WW3) is at its highest level ever.

How can this juxtaposition be explained? Perhaps, rather easily.

For example, let’s take a moment to picture in our minds a white-collar worker sitting at his office cubicle, surrounded by a bustling workplace around him. This gentleman appears more than relaxed sitting at his desk while staring at his computer screen. Essentially motionless with only some gentle typing on the keyboard, any outside observer would note that this employee appears calm, quiet, and reserved while going about his work. Needless to say, this man is not in a volatile or explosive state.

Milton is not in a volatile state.

However, inside this person is a fiery volcano ready to erupt. Blind to the outside eye, this man’s internal stress hormones are through the roof and only rising. Unbeknownst to all of his coworkers and others around him, the gentleman’s cortisol levels are spiking higher than ever following a terrible performance review with his boss just moments before, sudden fear of missing another mortgage payment with the increased threat of being fired, and to top things off, recent revelations that his wife has been cheating on him.

Mr. Christopher Cole, a market volatility expert and founder of Artemis Capital Management, likens this gentleman’s state to the current dynamic afflicting the entire global market construct. As he astutely identifies it, the market is currently in a state of projecting extremely low volatility while at the same time experiencing tremendously high uncertainty, not too dissimilar to the man described above.

In completely crediting Cole to the analogy above and for pinpointing a rather accurate portrayal of the state of global markets, this entire post is dedicated to answering the perplexing volatility question above by summarizing a recent interview Cole gave with aceloewgold.com friend Demetri Kofinas, on his recently launched and brilliant podcast series, Hidden Forces.

Demetri Kofinas' Hidden Forces Podcast at: www.hiddenforcespod.com

Financial Volatility at the Edge of Crisis with Christopher Cole / Ep. 5 with Demetri Kofinas (Hidden Forces)

SUMMARY

Market Period Leading Up to 2008

The period leading up to the financial crisis in 2008 is often identified as a time of massive monetary and fiscal expansion. On the heels of the 9/11 terrorist attacks and the collapse of the NASDAQ dot.com bubble, relatively low interest rates were expectedly moved even lower to stimulate an otherwise robust U.S. economy. In maintaining this lengthy low interest rate environment, former Fed Chairs Alan Greenspan and Ben Bernanke were touted as successfully being able to contain and manage inflation, in a period known to many as the “great moderation.” Helping matters, of course, was (and continues to be) the expansion of the global economy further into developing markets, particularly in Asia. As countries like China and other “Asian Tigers” opened up and began exporting more to the developed world, export proceeds generated needed secure places to go and be recycled. With the U.S. Treasury market essentially still the only game in town for excess reserves to flow into, the U.S. has benefited from a continuous bid for dollars to buy U.S. treasury bonds. Mixed with the power it retains as the global reserve, the dollar has naturally remained relatively strong over the years due to this “artificial” demand, while interest rates have been kept suppressed, as the only liquid/large enough bond market in the world perpetually grows even larger.

This dynamic, of course, has had many unintended consequences, particularly with the devastating effects felt in both national and private debt levels. With the cost of borrowing so low, debt levels have soared to unprecedented levels, whereas the savings rate dwindled down to historic lows (as savers continue to be penalized with unappealing rates of return). Unending increases in debt, however, can only last as long as the supporting economy can continue growing to service ballooning balance sheets. During periods of economic contraction, an environment like the “great moderation” can change on a dime.

And, change on a dime it did. Enter 2008.

2008 proved to be a significant bump in the road for the global economy – the entire system, all of the sudden, went from a harmonious balance of “great moderation” to the brink of collapse with the threat of a massive deflationary implosion. To combat a complete systemic failure, the Fed and the rest of the world’s central banks intervened during the chaos, and pulled out all of the stops – throwing the kitchen sink and more at the imminent demise of entire global financial system. Slashing rates, QE’s, Operation Twists, reducing reserve requirements, massive bailouts, liquidity facilities, restructurings (ESM, ESFS, OMT in Europe), massive fiscal stimulus in China, and more – the collapse of the global economy, for the time being, was thwarted by enormous stimulus measures the world had never seen before.

Market Period Between 2008 - 2012

For about four years or so between the beginning of the financial crisis in 2008 through 2012, the markets and the global economy were in a precarious state. With so much uncertainty around the effectiveness of the unprecedented efforts from the central banks, volatility in the markets see-sawed regularly between heightened fears of systemic collapse (i.e. Flash Crash, European Sovereign Debt Crisis, etc.) to periods of momentary relief in temporarily being able to extinguish a seemingly endless amount of fires in “whack-a-mole” fashion.

2012

In 2012, everything changed. In what was shaping up to be the “end of the world,” even popularized by films like “2012,” it appeared to many that the systemic dam would inevitably break again. In an abnormal attempt to get ahead of the curve, however, the Fed and other global central banks strategically changed their tune in 2012. In order to help pacify the growing angst in the markets, central banks tactically moved from a position of being reactive to proactive. No longer were central bankers in the business of fighting crises and putting out endless fires. Led in particular by one central banker and one extraordinary remark, global central bank policy moved swiftly from incessantly responding to the 2008 crisis and its aftermath, to preemptively quelling volatility at all costs and stomping out all fires before they appeared.

ECB President Mario Draghi

In July 2012, ECB President Mario Draghi stunned markets with his “whatever it takes” speech, ultimately fortifying the survival of the euro and Eurozone. That statement, in combination with the Fed’s launch of QE3 (an unending iteration of $85B of bond purchase per month) changed everything.

Taking the cue, market participants have essentially shifted investment/volatility strategies to auto-pilot with the understanding that under any and all circumstances, global financial markets will be both protected and propped up by regular and extraordinary stimulus measures. With the Fed, ECB, and other powerful central banks unequivocally telling the markets that they are now in the business of preventing asset price declines to stave off the risk of systemic collapse, “left tail” risk, or extreme volatility to the downside (deflation) has naturally shifted to the “right tail,” with more surreptitious volatility steadily building to the upside (inflation).

Last 5 Years

During this quiet shift from “left tail” to “right tail,” volatility has appeared to fade away completely. Over the last five years or so, the markets have experienced little to no volatility as investors, traders, and computer algorithms alike have embraced the mantra that even bad news is good news for asset prices. Whether it’s been a bad jobs report/economic data, lackluster earnings, or even a terrorist attack, all market dips continue to be bid up with the continued expectation that central banks will forever administer more stimulus into the system, if need be.

In another appropriate analogy, Cole (and even Fed officials like Dick Fisher) have likened this dynamic and response mechanism to a doctor treating a cancer patient. Rather than treat the underlying illness, the doctor irresponsibly only gives the patient amphetamines during each visit. Naturally, the patient feels great leaving the doctor’s office, but of course, is increasingly only getting sicker. Like a patient with cancer, our financial system has a cancer of exorbitant debt, ill-fated demographics, and crushing deflationary pressures, with Dr. Yellen, Dr. Draghi, and others prescribing nothing but amphetamines of QE and other forms of extraordinary stimulus measures to treat the waning markets.

As one can imagine though, volatility and risk have not been destroyed – they have simply been transmuted. While a “right tail” blow-off inflationary top may eventually be in the cards as this shift intensifies, the truth is that this transmutation of risk/volatility has potentially created the most ominous of “unknown unknowns.” Because we have set off into unchartered monetary waters, transmuted volatility/risk is not being properly priced or reflected in the financial markets through traditional mediums like the VIX, and yet, most would argue it is being felt elsewhere. Like water running down a mountain stream, true volatility and risk will find a way. Right now, it is being felt geopolitically with the rise of nationalism and social unrest sweeping through the U.S., Europe, and the rest of the world (with current attention on the French and South Korean elections).

In the financial markets, new risks and vulnerabilities have undoubtedly been created and will emerge, but for the time being, the embedded moral hazard that’s been injected into the patient persists. With the drugs pumping in and the markets melting up, the economy (like the patient) continues deteriorating. In an economy that is barely growing with an anemic Q1 GDP print of only 0.7%, publicly traded companies are having an increasingly more difficult time keeping quarterly earnings in-line with record high stock prices and valuations.

The result, of course, is that companies are continuing to buy back their own shares at increasingly elevated levels to reduce shares outstanding, and financially engineer higher Earnings-Per-Share (EPS) figures each quarter. Unbeknownst to the general public as they watch record market prices and corporate earnings beats, we are currently witnessing the highest level of share buybacks ever. Buybacks are not inherently bad, provided the company doesn’t have a better use of its cash and is buying below intrinsic value, but we’re seeing the complete opposite take place.

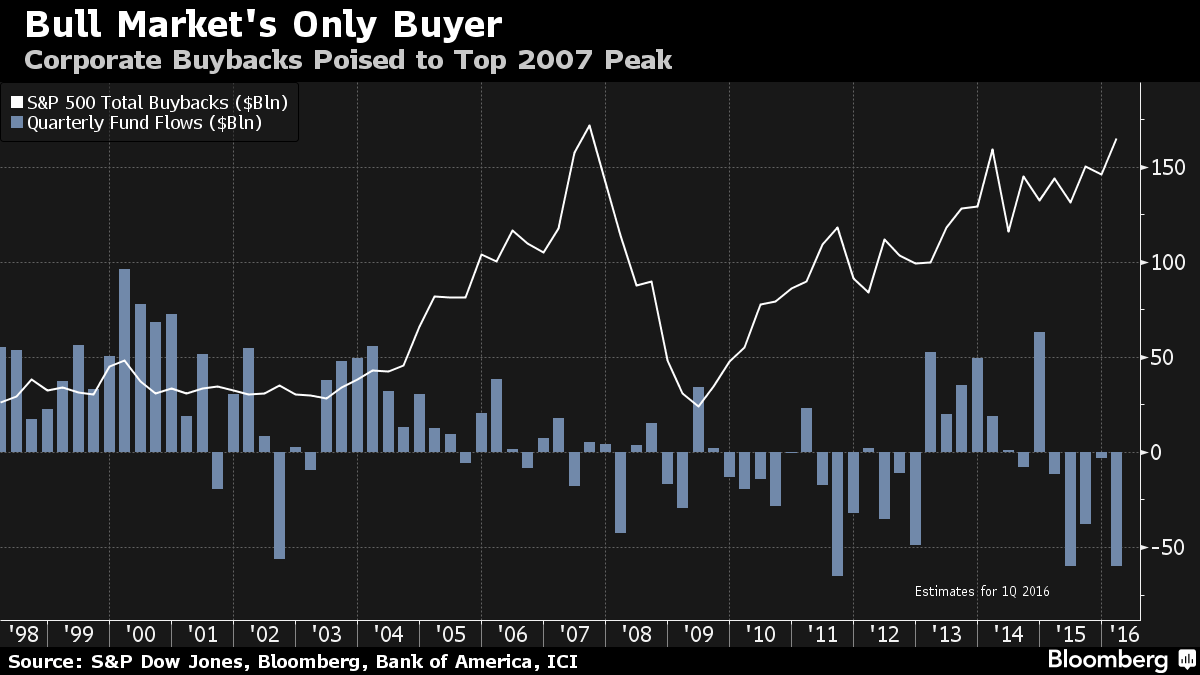

"Bull Market's Only Buyer" - Bloomberg

Interestingly, the late Steve Jobs was adamant that share buybacks were a sign of organic weakness and an indication to the market that a company had run out of ideas. Insinuating at the time that his innovative company would never stoop as low as buying back its own stock, Apple, of course, has since become one of the market leaders of share buybacks, purchasing roughly $150B of shares just in the last few years alone.

Apple and others have had no choice but to financially engineer growth in what has been the weakest economic recovery since the Great Depression. 50% of the EPS growth over the last year and a half, in fact, has come as a direct result of share buybacks, and 25% of that growth was from repurchases before that. Rather than use cash for reinvestment, R&D, hiring, and expansion, companies are even looking to the perpetually cheap debt market to fund more buybacks at the risk of completely blowing up otherwise sound balance sheets.

Market participants are currently watching what is turning out to be one massive “leveraged buyout of the entire stock market.” Off the lows in March 2009, this continues to be the only bull market in history that has experienced lower and lower trading volume (as a direct result of the ever-decreasing amount of shares outstanding). With a record amount of share buybacks, corporate debt loads, and an increasingly more difficult time meeting/exceeding quarterly earnings expectations under current valuations, it is no wonder that C-suite executive insiders are the ones on the front lines selling at every chance they get.

Present Market Conditions

Due to distorted market conditions and response mechanisms largely created by the world’s central banks, the foundation for growth has almost entirely been built on financial engineering rather than genuine economic or fundamental reasons. Present growth lives in a system inflated by the largest debt levels ever recorded, untenable corporate and central bank balances sheets, unprecedently low interest rates, and the most expensive equity market ever as seen through Enterprise Value/EBITDA, Price/Sales, Price/Book, and Case Shiller P/E.

As it turns out, with artificial growth comes artificially dampened market volatility. As alluded to above many times, we have an incredibly strange dynamic embedded in the market with little to no volatility to report of, as measured by the VIX (1-month implied volatility). Like the white collar worker example, however, uncertainty and internal stress hormones in the market are actually as high as ever. Looking outside of the traditional volatility price discovery vehicle (VIX), “forward volatility" (uncertainty/internal stress hormones), as measured through forward volatility term structure, VIX futures, skew, and variance swaps are at their highest levels ever. With the VIX seemingly sitting at some of its cheapest levels ever, in reality, future volatility (where the underlying uncertainty and stress hormones are being priced in) is actually quite expensive. This signals that vigilant markets participants are very much aware that at some point, the volcano will erupt.

For now, however, the volcano lies dormant and professional money managers essentially have no choice but to be “short convexity”. In Cole’s equation, Short Convexity = Long Consensus = Long Status Quo = Long Mean Reversion = Long Value Investing = Short Volatility (VIX). On the flip side, the contrarian/minority trade Cole is building a firm and reputation on is: Long Convexity = Short Status Quo = Long Positive Exposure to Change (upside and downside) = Long Volatility (near-term and long-term).

For the time being, the masses in the markets are willing to stay “short convexity” and risk continuing to pick up pennies in front of a moving steamroller.

Spoiler Alert – The Steamroller Always Wins

As mentioned briefly above, there are “three-D’s” currently driving the steamroller. The drivers of debt, demographics, and deflation are stepping down on the gas pedal, and the steamroller is only picking up speed. Record debt levels and crushing deflationary pressures are glaring problems certain to eventually ignite volatility, but even the lesser-talked about demographic headwinds are just as precarious. Volatility could, in fact, be moved forward in a hurry as baby boomers retire at an ever-increasing rate.

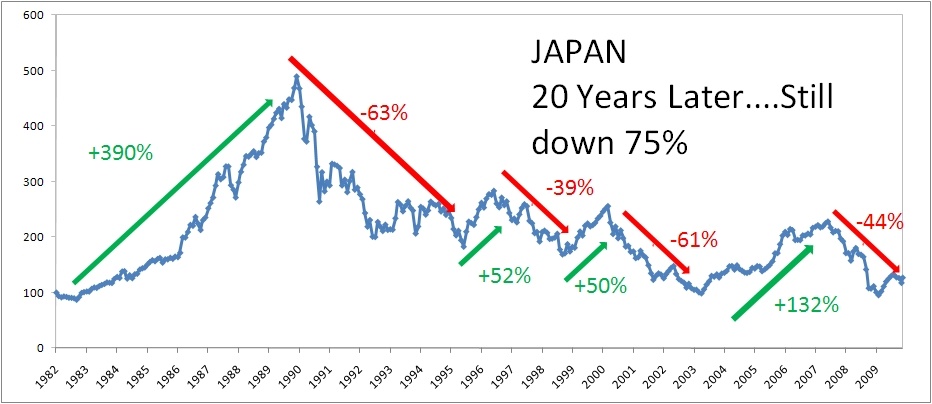

Japan's Nikkei 225 Index

With baby boomer retirement comes the escalating withdrawal of ~75 million retirement and savings accounts, making for what is expected to be a 10-20 year drawdown of money from the global markets akin to the “lost decade” deflationary spiral experienced in Japan.

Central banks, of course, are not the only ones attempting to stand firmly and push against the forces of this “three-D” steamroller. With little to no influence over monetary policy, the public has taken its own fight to the geopolitical world, where there still is a sense of power to enact change. Unsurprisingly, the rise of populism and nationalism has spouted quickly throughout the world.

Rise of populism/nationalism

The intentions of central bankers may very well have been pure in wanting to prevent an all-encompassing systemic collapse, yet the outcome being felt by the general public is one that seems to have only benefited the wealthiest class. As a small percentage of the population, but one that owns the majority of assets (stocks, real estate, etc.), the wealthy have undoubtedly separated/enriched themselves further, while the masses fight over zero-income growth scraps. Donald Trump, therefore, is nothing more than a symptom of Ben Bernanke and Janet Yellen, whereas Marine LePen in France is a direct result of Mario Draghi.

Typically, many look to the markets as a leading indicator, but because of the dormant state of its volatility, we may now be seeing geopolitics taking over that forecasting role. Real volatility is being experienced, but instead of seeing it reflected in the VIX, we’re seeing it in the polls. Under normal circumstances, Brexit and Trump would have unleashed the fury of a market volcano, but similar to other “bad news” events, they too have been swallowed up by the volatility blackhole. All that is happening, though, is that true volatility, risk, and fragility in the system are continuing to be hidden by the same reinforcing feedback dynamics of the market. Because of a potent and self-reflexive mixture of a pervasive central bank reaction function (bad news = good news), more share buybacks (permanent bid for stocks), and a ubiquitous “short convexity” market strategy, volatility continues to have a very difficult time breaking out without getting snapped back to its mean. Over the last five years or so, volatility rises briefly/temporarily, only to be immediately pushed back down by these reflexive pressures.

Simply put, this pattern cannot continue forever. At some point, we will reach a theoretical “air-pocket” that exists, where a catalyst will send volatility past a certain threshold beyond these reflexive barriers, and all of these dynamics will suddenly work in the opposite direction. As soon as the market realizes that the self-reflexive volatility mean reversion is not happening, the volcano can finally erupt bringing both volatility and the market’s internal stress hormones together to one acute blowup point.

According to Cole, here in the U.S., we could very easily experience this acute volatility blowup in either the “left tail” or the “right tail”. For instance, if Trump ignores some of his campaign rhetoric and continues to veer more towards the political status quo, it’s more likely we’ll see a continuation of low interest rates ignite inflation, sending asset prices skyrocketing into a blow-off top. With rates low, inflation ramping up, and prices moving exponentially higher, money managers will be forced to chase performance versus one another. On the other hand, if things go south with Trump (i.e. war break out, a bad trade deal, rates rise, etc.), volatility could swing swiftly back into the “left tail” sending markets into a deflationary collapse. Similarly, outside of the U.S., unexpected geopolitical results/reactions/policy actions in France, South Korea, Italy, Germany, and elsewhere all pose as “left tail” air-pocket risks to the financial markets.

Conclusions

What’s certain is that the success stocks and bonds have had in the U.S. moving higher together over the last 30 years cannot last forever. In order for both asset classes to continue to move higher in tandem would mean that bond yields eventually go negative. With the U.S. and the entire world, though, at or near the zero bound, it is virtually impossible for bond prices to go any higher (yields lower). With that in mind, Cole poses a very interesting question - what would happen if stocks and bonds continue to move together, but this time turn down? Thanks to the “taper tantrum” in 2013, we got a sneak peek of just how chaotic things could get in just a matter of a couple of months. While the volatility blackhole ended up claiming another victim then, what if one or two months of stocks and bonds moving lower together turned into a year or more?

While Cole makes incredibly sound arguments and investors should be prepared, timing, as they say is everything. Cole and Artemis Capital Management work around market volatility timing with sophisticated proprietary trading models, but for the retail investor out there, it is perhaps wise to heed these famous last words from the legendary British economist John Maynard Keynes: “The market can stay irrational longer than you can stay solvent.”

Sources:

2010 Flash Crash. (2017). Wikipedia:

https://en.wikipedia.org/wiki/2010_Flash_Crash

2012 (film). (2017). Wikipedia:

https://en.wikipedia.org/wiki/2012_(film)

2012 Phenomenon. (2017). Wikipedia:

https://en.wikipedia.org/wiki/2012_phenomenon

24/7 Wall St. (2017). Huge Insider Selling Continues as Market Hits Record Highs: MasterCard, Adobe Systems, Charles Schwab, FedEx and More. MarketWatch: http://www.marketwatch.com/story/huge-insider-selling-continues-as-market-hits-record-highs-mastercard-adobe-systems-charles-schwab-fedex-and-more-2017-01-28

Abe, Naoki. (2010). Japan’s Shrinking Economy. Brookings: https://www.brookings.edu/opinions/japans-shrinking-economy/

Bullock, Nicole. (2017). Equity bulls enter 2017 ignoring expensive valuations. The Financial Times:

https://www.ft.com/content/796410cc-c6ff-11e6-8f29-9445cac8966f

Chandra, Sho. (2017). U.S. Economy Grew 0.7% in First Quarter, Slowest in Three Years. Bloomberg:

https://www.bloomberg.com/news/articles/2017-04-28/u-s-economy-expands-at-slowest-pace-in-three-years

Cox, Jeff. (2016). For markets, bad news is still good news. CNBC: http://www.cnbc.com/2016/09/02/for-the-stock-market-bad-jobs-news-is-still-good-news-on-interest-rates.html

DoctoRx. (2013). Apple Exits The Steve Jobs Era, Bets On Engineering Of The Financial Kind. Seeking Alpha: https://seekingalpha.com/article/1375571-apple-exits-the-steve-jobs-era-bets-on-engineering-of-the-financial-kind

Donald Rumsfeld Unknown Unknowns! (2009). YouTube: https://www.youtube.com/watch?v=GiPe1OiKQuk

Dunkley, Jamie. (2012). Debt crisis: Mario Draghi pledges to do 'whatever it takes' to save euro. The Telegraph: http://www.telegraph.co.uk/finance/financialcrisis/9428894/Debt-crisis-Mario-Draghi-pledges-to-do-whatever-it-takes-to-save-euro.html

Durden, Tyler (2017). Dead Market Ramping - Stocks Hit Record Highs As Activity Hits Record Low. Zero Hedge: http://www.zerohedge.com/news/2017-02-10/dead-market-ramping-stocks-hit-record-highs-activity-hits-record-low

Durden, Tyler. (2016). Former Fed President: "We Injected Cocaine And Heroin Into The System To Create A Wealth Effect". ZeroHedge: http://www.zerohedge.com/news/2016-03-09/former-fed-president-we-injected-cocaine-and-heroin-system-create-wealth-effect

Durden, Tyler. (2016). How Much Of S&P Earnings Growth Comes From Buybacks. Zero Hedge:

http://www.zerohedge.com/news/2016-04-06/how-much-sp-earnings-growth-comes-buybacks

Durden, Tyler. (2017). Peak Savings: Wall Street Faces 20 Years Of Retirement Withdrawals As Boomers Hit 70 ½. Zero Hedge: http://www.zerohedge.com/news/2017-01-16/peak-savings-us-demographic-time-bomb-ready-explode-boomers-hit-70-12-years

Durden, Tyler. (2017). Obama Oversaw The Weakest Growth In American's Personal Income On Record. Zero Hedge: http://www.zerohedge.com/news/2017-01-30/obama-oversaw-weakest-growth-americans-personal-income-record

Elliott, Larry. (2016). IMF urges governments to tackle record global debt of $152tn. The Guardian: https://www.theguardian.com/business/2016/oct/05/world-debt-has-hit-record-high-of-152tn-says-imf

European Debt Crisis. (2017). Wikipedia:

https://en.wikipedia.org/wiki/European_debt_crisis

Evans, Stephen. (2017). South Korea's 'life or death' presidential election. BBC News:

http://www.bbc.com/news/world-asia-39801447

Fox, Justin. (2017). (Some) Americans Are Saving (Some) Money Again. Bloomberg:

https://www.bloomberg.com/view/articles/2017-05-01/-some-americans-are-saving-some-money-again

Hakkio, Craig. (2017). The Great Moderation. Federal Reserve History: https://www.federalreservehistory.org/essays/great_moderation

Kawa, Luke. (2017). Older Americans Are Retiring in Droves. Bloomberg:

https://www.bloomberg.com/news/articles/2017-01-06/older-americans-are-retiring-in-droves

Mahmudova, Anora. (2016). U.S. companies spent record amount on buybacks over past 12 months. MarketWatch: http://www.marketwatch.com/story/us-companies-spent-record-amount-on-buybacks-over-past-12-months-2016-06-22

Mario Draghi's "Whatever it takes". (2015). YouTube: https://www.youtube.com/watch?v=tB2CM2ngpQg

Matthews, Dylan. (2012). QE3 is on! Fed to buy $85b through December, and then keep going. Washington Post: https://www.washingtonpost.com/news/wonk/wp/2012/09/13/qe3-is-on/?utm_term=.1eb3b984cfb2

Morath, Eric. (2016). Seven Years Later, Recovery Remains the Weakest of the Post-World War II Era. The Wall Street Journal: https://blogs.wsj.com/economics/2016/07/29/seven-years-later-recovery-remains-the-weakest-of-the-post-world-war-ii-era/

Niu, Evan. (2017). How Apple, Inc.'s Share Repurchases Are Driving Record Results. The Motley Fool:

https://www.fool.com/investing/2017/02/06/how-apple-incs-share-repurchases-are-driving-recor.aspx

Sjolin, Sara. (2017). Brace for market mayhem if Le Pen unexpectedly wins French presidency. MarketWatch: http://www.marketwatch.com/story/brace-for-market-mayhem-if-le-pen-unexpectedly-wins-french-presidency-2017-05-04

VARIANCE AND VOLATILITY SWAPS. (2017). FinCad Resources: http://www.fincad.com/resources/resource-library/wiki/variance-and-volatility-swaps

VIX Futures. (2017). CBOE: http://www.cboe.com/products/vix-index-volatility/vix-options-and-futures/vix-futures

Volatility Skew. (2017). Investopedia: http://www.investopedia.com/terms/v/volatility-skew.asp

Xie, Chen. (2015). Understanding volatility term structure. Futures Mag: http://www.futuresmag.com/2015/04/15/understanding-volatility-term-structure

Author

David Loewenthal

ACELOEWGOLD

Current MBA and Wall Street survivor from 2006-2013. Worked as a capital markets analyst in NYC for seven years largely during the financial collapse, specializing in currency markets, global central bank policy actions, and technical analysis.