Vehicle Detailing: Record Auto Debt and the Consumer

Executive Summary

Household debt is at a record high, but as a share of GDP it is way down from its 2008 peak. The lower debt share today suggests that households are in better shape. But when we look at the composition of household debt we find that nearly all the growth in household debt in this cycle has come from just two categories: student loans and auto loans. This report focuses on auto loans, an upcoming report will build on work we have already done on the student loan situation.

Consumers today are buying bigger, more expensive cars and they are financing them for much longer periods of time than even a few years ago. While the median credit score of borrowers is higher and banks are already tightening lending standards, the cost of ownership is proving to be onerous given elevated levels of auto loan delinquencies.

We are not overly worried at present, but the run-up in auto loans is a potential risk not only to auto sales but to consumer spending more broadly. An exogenous shock, like a surge in gasoline prices or sudden deterioration in consumer confidence, could slow the pace of auto sales or lead to even higher delinquency rates or both. For now though, consumer confidence is at a 6-month high and gas prices remain relatively low. On that basis, we expect the pace of auto sales to remain steady or perhaps slow slightly and delinquencies to remain in check.

Putting Auto Loans in Perspective

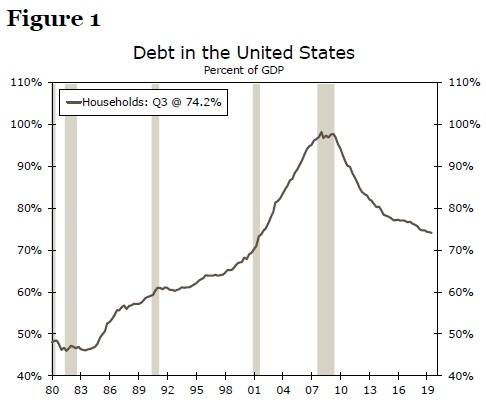

One of the major imbalances in the lead-up to the financial crisis and recession was sky-high levels of household debt. As a share of GDP, household debt peaked at 98.3% in the first quarter of 2008. In level terms, the amount of household debt outstanding today is more than $1 trillion larger than its peak in 2008, but since the economy has grown much faster than household liabilities, the share of household debt relative to GDP has come down to just 74.2% (Figure 1).

Source: Federal Reserve Board, Federal Reserve Bank of New York and Wells Fargo Securities

The lower debt share today suggests that in aggregate at least, households are in better shape. But when we look at the composition of household debt, we find nearly all of the growth this cycle has come from just two categories: student loans and auto loans.

To put the category in perspective, the $1.3 trillion in auto loans represents the third largest category of household debt (after mortgages and student loans). As a share of the total, auto loans comprise 9.4%. While the growth in student loans has grabbed most of the attention this cycle, it bears noting that the 64.5% growth in auto loans towers over the growth in the next fastest-growing category, credit cards, which is up only 8.0%.

Author

Wells Fargo Research Team

Wells Fargo