USOil dips lower

USOil, Daily

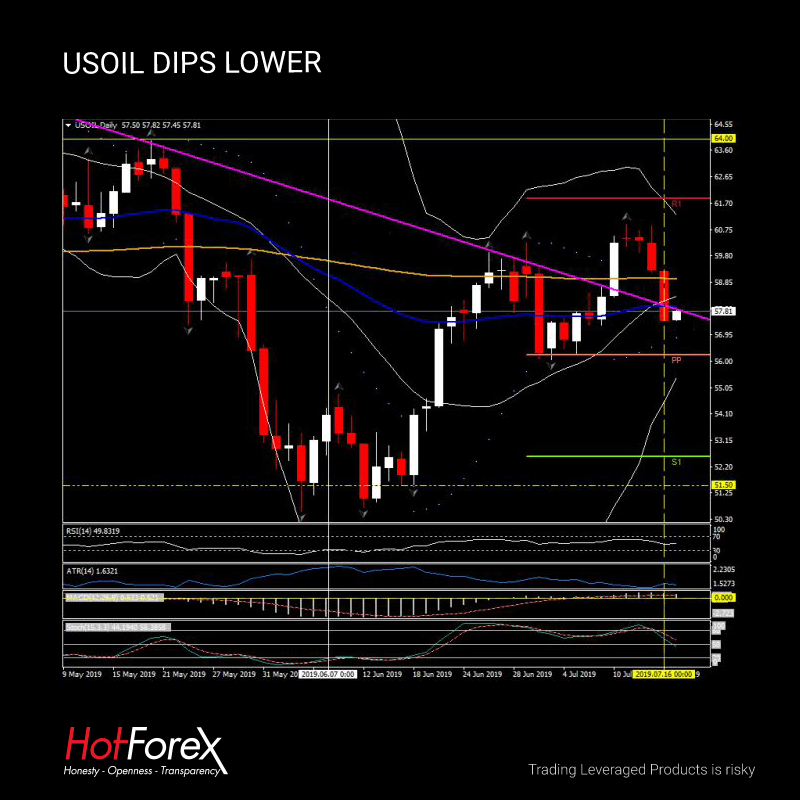

USOil fell 3% yesterday following comments from US Secretary of State Pompeo in a cabinet meeting, who said that for the first time, Iran is prepared to negotiate on its missile programme. Since the downing of the US drone by Iran in the Persian Gulf, US/Iran tensions have been high. This news may signal a shift of policy in Iran, perhaps set to lower geopolitical tensions in the Mideast. However, Iran later denied that they were willing to negotiate over their defence systems.

However, the private industrial group the American Petroleum Institute (API) recorded a decline in inventories of 1.4 million barrels for the week compared to expectations for a decrease of 2.7 million barrels. This stalled the move lower yesterday around $57.25. The official US government data from the Energy Information Administration (EIA) is due later today and expectations are for a reduction in inventories of 3.6 million barrels, which if correct will be the fifth consecutive weekly decline, the longest stretch since the beginning of 2018. The June 26 and last week’s data registered declines of over 10 million barrels as the US driving season is in full swing.

The impact from Hurricane Barry could also bring back supply and limiting gains, however, production from the US Gulf is still under 50% of normal daily volumes following the weekend outages.

Yesterday, the decline moved the USOIL price below the 200, 50 and key 20-day moving averages for the first time in 16 trading days. Support now sits at the Daily pivot point at $56.00 and S1 at 52.50, Resistance to high prices is at $59.00 and $61.80.

Author

With over 25 years experience working for a host of globally recognized organisations in the City of London, Stuart Cowell is a passionate advocate of keeping things simple, doing what is probable and understanding how the news, c