USD/JPY Forecast: Don’t look back, risk-aversion might be gaining

- US China tensions rise over trade, pandemic and Hong Kong.

- USD/JPY technical reversal on May 11 confirmed.

- Why did the Bank of Japan meet on Friday?

The USD/JPY consolidated its breakout this week as tensions between the US and China over a variety of topic bolstered the dollar against the yen in a mild return to risk-aversion pricing.

Washington and Beijing engaged in a war of words over the origin and responsibilities for the coronavirus, while the US Senate passed a bill that could restrict mainland companies from listing on American exchanges and China proposed a strict new security law for Hong Kong that would permit its agents to operate freely in the former British colony.

Countering the political disputes were generally positive developments in the pandemic as many US states and European countries continued to loosen restrictions with no adverse effects and several vaccines have shown promising results.

The emergency or at least unscheduled Bank of Japan meeting on Friday produced no results other than a headline. The governors held the cash rate at -0.1% and offered no new stimulus measures.

USD/JPY outlook

Currencies have not shaken the lingering effects of the great March and April pandemic panic but risk-aversion is being driven more by secondary effects like the US-China rhetoric on virus responsibility-the origin is not in dispute-and its spillover into trade and politics. In Hong Kong Beijing is using the pandemic distraction to tighten control on the city and end the one country, two systems policy of the last two decades.

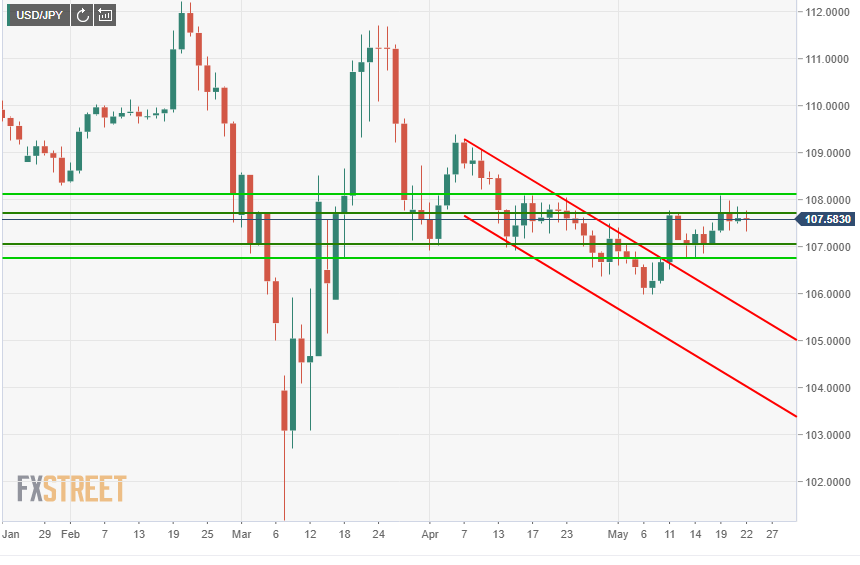

Since the break of the four-week old channel on May 11 the USD/JPY has kept a tight limit of 107.00-107.75 on the daily open and close and 106.80 to 108.85 on the overall range. The USD/JPY opened at 107.04 on Monday and finished the week at 107.59.

The pandemic risk-premium is being replaced by more conventional worries over US-China trade and Pacific Basin politics but the impact on currencies is similar with risk driving toward the US dollar.

The relative balance between risk and optimism of the past two weeks will not hold and the next move will be determined by whether the burgeoning conflict with China or the global economic recovery becomes the dominant motif.

Japanese and US statistics summary May 18-May 22

Japanese and US statistics summary May 18-May 22

Japanese statistics confirmed that the economy entered its fourth recession in the past decade as annualized GDP contracted 3.4% in the first quarter following the revised 7.3% decline in the final three months of 2019.. April exports plunged on the year as expected though imports dropped less than forecast.

In the United States jobless claims continued to shrink with 2.4 million filed in the latest week but with a total of almost 39 million in the past nine weeks and over 25 million continuing claims improvement would be the wrong description. There is as yet no sign of returning employment reducing the jobless rolls. The IHS Markit preliminary PMI surveys for May were better than expected though still deep in contraction, suggesting that a bottom for the economy may have been reached.

There is little to choose between the pandemic economic collapse in the two countries, and though the Markit PMI may hold promise for the US other statistics likely will not. The Atlanta Fed GDPNow model for the second quarter is -41.9%.

The original quote for the title is from Satchel Paige, the American baseball player, “Don’t look back. Something might be gaining on you.”

Japan statistics May 18-May 22

Monday

First quarter annualized GDP dropped 3.4%, less than the -4.6% expected but following on the fourth quarter’s 7.3% decline, Japan entered its fourth recession since the financial crisis. On the quarter the economy contracted 0.9% on a 1.2% forecast after dropping 1.9% in the final three months of last year.

The Tertiary Index that tracks the service sector dropped 4.2% in March, much worse than the expected 0.2% gain and February’s 0.5% loss.

Tuesday

Industrial production for March was unrevised at -5.2% for the year and -3.7% for the month as predicted after dropping 5.7% and -0.3% respectively in February.

Machinery orders dropped 0.4% in March, far better than the -7.1% projection and 0.7% for the year also much less than its -9.5% estimate. Monthly orders were 2.3% higher in February and 2.4% lower on the year.

Wednesday

April imports declined 7.2%, improving on the 12.9% forecast but making 12 negative months in a row. Exports plunged 21.9%, close to the -22.7 forecast but the largest drop since the financial crisis and one month shy of a-year-and-a half of declines.

Thursday

National CPI (ex-fresh food) fell 0.2% in April y/y missing the -0.1% forecast after rising 0.4% in March. National COI (ex food and energy) rose 0.2% on the year following a 0.6% gain in March.

The Bank of Japan kept the overnight cash rate at -0.1%, at its emergency meeting where it has been since January 2016. The bank announced a new lending program worth 30 trillion yen ($279 billon) to support small businesses but did not add any general economic stimulus.

US statistics May 18-May 22

Monday

The National Association of Home Builders Index for May, an indicator of future growth in housing, came in at 37, better than the 33 forecast and the April reading of 30 which had been the lowest since June 2012.

Thursday

Initial jobless claims were 2.438 million in the May 15 week, 2.4 million were forecast. Continuing claims were 25.073 million slightly above the 24.765 million and a 2.525 million increase. In the past nine weeks 38.615 million people have claimed unemployment insurance.

Existing home sales plummeted 17.8% in April, not quite as much as the 18.9% prediction and the 4.33 million annualized selling rate retreated to just above the post-crash low of 3.83 million of July 2010.

HIS Markit’s preliminary PMI surveys for May were 36.4 for the composite, up from 27 in April, 39.8 in manufacturing from 36.1 and 36.9 in services from 26.7. All the April reading were the lowest for the approximately 10-year old survey.

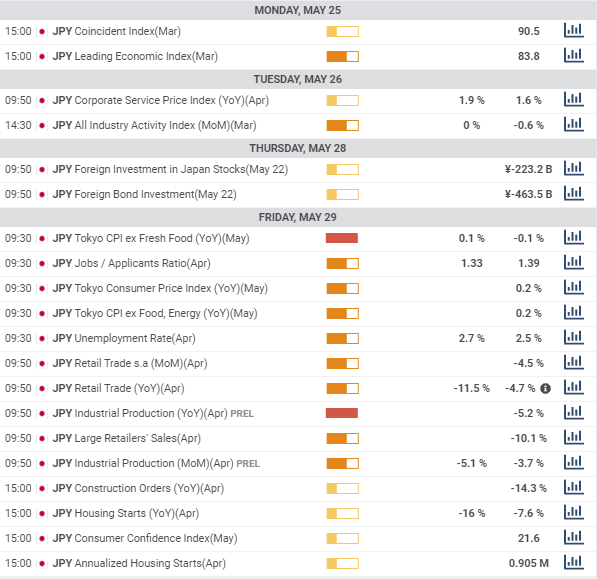

Japan statistics May 25-May 29

Japan statistics May 25-May 29

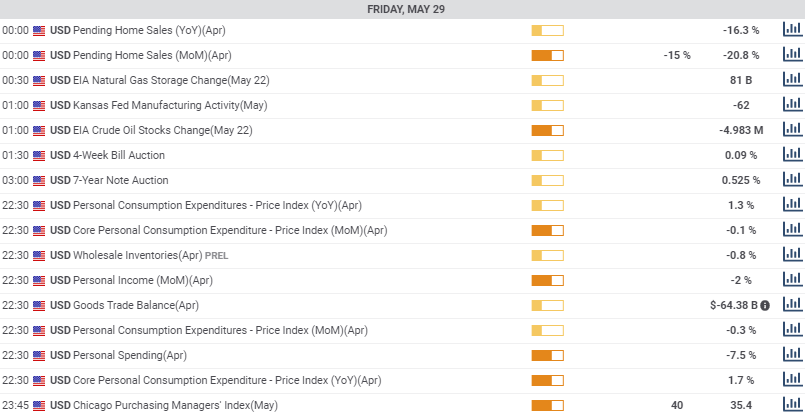

US statistics May 25-May 29

US statistics May 25-May 29

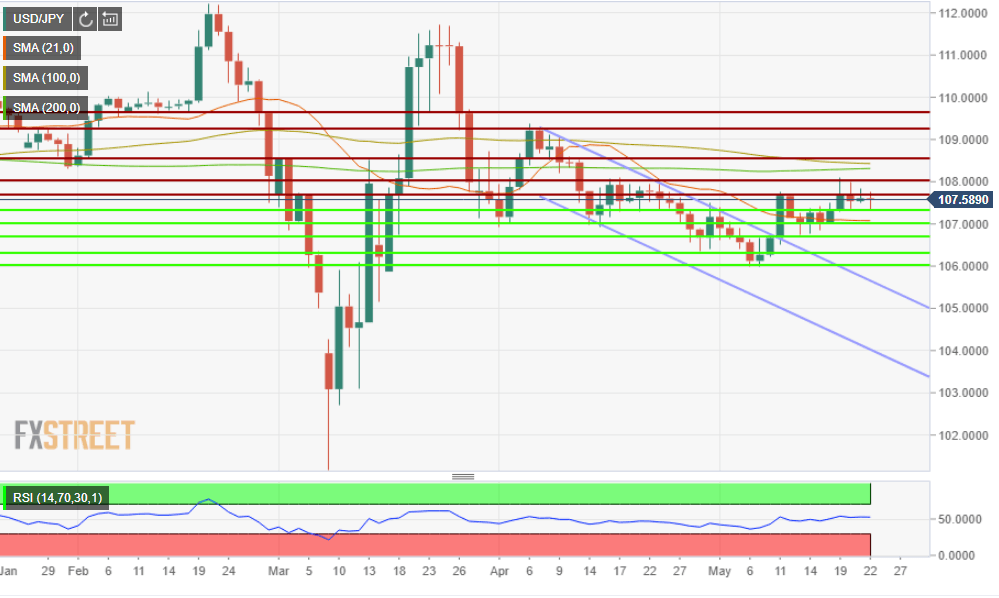

USD/JPY technical outlook

USD/JPY technical outlook

The relative strength index (RSI) is nearly neutral at 50 as would be expected after a week of limited movement, giving little indication of potential. The 21-day moving average is also flat and resting at 107.07 adds to the107.00 support line. The 100-day average at 108.43 is essentially part of the 108.55 resistance line as is the slightly more distance 200-day average at 108.31. The cross of the 21-day average on Monday lends a minor upward cast to the USD/JPY.

Resistance: 107.75; 108.00; 108.55; 109.25: 109.65

Support: 107.35; 107.00; 106.70; 106.30; 106.00

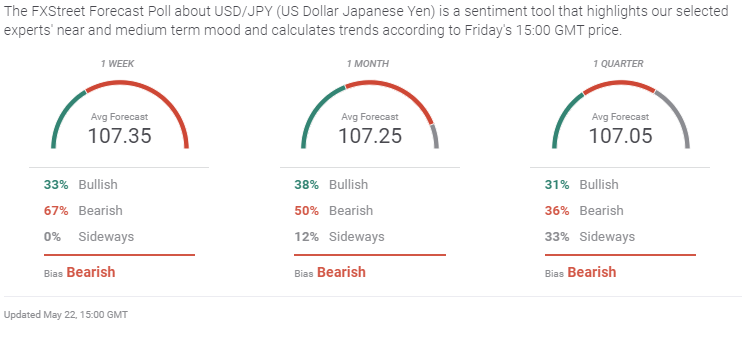

USD/JPY sentiment poll

Despite the strongly bearish cast in the near term the forecast at 107.35, just 25 points under the Friday close is weak. The same could be said for the one month and one quarter views. The clear lack of predictive movement in the forecasts betrays the current lack of direction in the USD/JPY. Or to put it another way, the pair is still subject to developments beyond the ken of charting analysis.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.