USD rally accelerating with key moves on forex as gold breaks lower [Video]

![USD rally accelerating with key moves on forex as gold breaks lower [Video]](https://editorial.fxstreet.com/images/Markets/Currencies/Crosses/AUDJPY/forex-australia-and-japanese-currency-pair-with-calculator-4780678_XtraLarge.jpg)

Market Overview

A recovery on the US dollar is gathering momentum. With traders increasingly concerned about second wave COVID infection rates rising across Europe and trends also turning higher for the US, there is a shift into the dollar. Throughout the summer months the perception was that the US was in for economic underperformance. However, this perception is now being re-set as France, Spain and increasingly the UK are struggling with rising infection rates which are forcing the reinstatement of social containment measures. Congress may have been able to pass a stopgap funding bill to keep government open, but a fiscal support package remains some way off. Fed chair Powell may have towed the dovish line, but there has also been surprisingly hawkish comments from the FOMC’s Charles Evans over limiting QE and raising rates sooner than expected. The dollar has seen the benefit of all this, driving higher through 94.00 resistance on Dollar Index. This equates to two month lows on EUR/USD whilst gold has also broken decisively below $1900. The Reserve Bank of New Zealand maintained a fairly steady ship on monetary policy (rates at +0.25%, asset purchases steady at NZD 100bn) and kept the door open to negative rates. This has not helped the Kiwi too much though this morning.

Wall Street closed with good recovery gains, with the S&P 500 +1.1% at 3315, whilst US futures are steady this morning (E-mini S&Ps +0.1%). Asian markets were all but flat overnight, with the Nikkei just -0.1% lower after two days of public holiday and the Shanghai Composite basically flat. European markets look set for a decent rebound with FTSE futures +0.9% and DAX futures +0.5%. In forex, we see USD strengthening continuing across the major pairs, with AUD and NZD underperforming, whilst EUR and JPY are only slightly weaker. In commodities, the big declines continue in the precious metals, with silver -5% and gold -1% lower again today. Oil is also around -1% lower.

The economic calendar is awash with flash PMIs for September today. Eurozone data is at 0900BST and is expected to show Eurozone flash Manufacturing PMI improving to 51.9 (from 51.7 final August) and Eurozone flash Services PMI to remain at 50.5 (50.5 final August). This would see the Eurozone flash Composite PMI slipping slightly to 51.7 (from a final 51.9 in August). The UK flash Manufacturing PMI is at 0930BST and is expected to drop back to 54.1 (from 55.2 final August) whilst UK flash Services PMI is expected to fall to 56.0 (from 58.8 final August). This would leave the UK flash Composite PMI at 56.3 (down from 59.1 in August). The US flash Manufacturing PMI is at 1445BST and is expected to remain at 53.1 (53.1 final August) with the US flash Services PMI to slip slightly to 54.7 (from a final 55.0 in August). Aside from that, the EIA Crude Oil Inventories are at 1530BST and are expected to show an inventory drawdown of -2.3m barrels (after a drawdown of -4.4m barrels last week).

Once more there will be focus on Fed chair Jerome Powell who testifies before the House Select Committee at 1530BST about impact of COVID-19. Again, any clarity on Fed monetary policy could drive volatility. There are two other Fed speakers today too, with Loretta Mester (tends to lean hawkish) at 1400BST and Randall Quarles (centrist) at 1900BST.

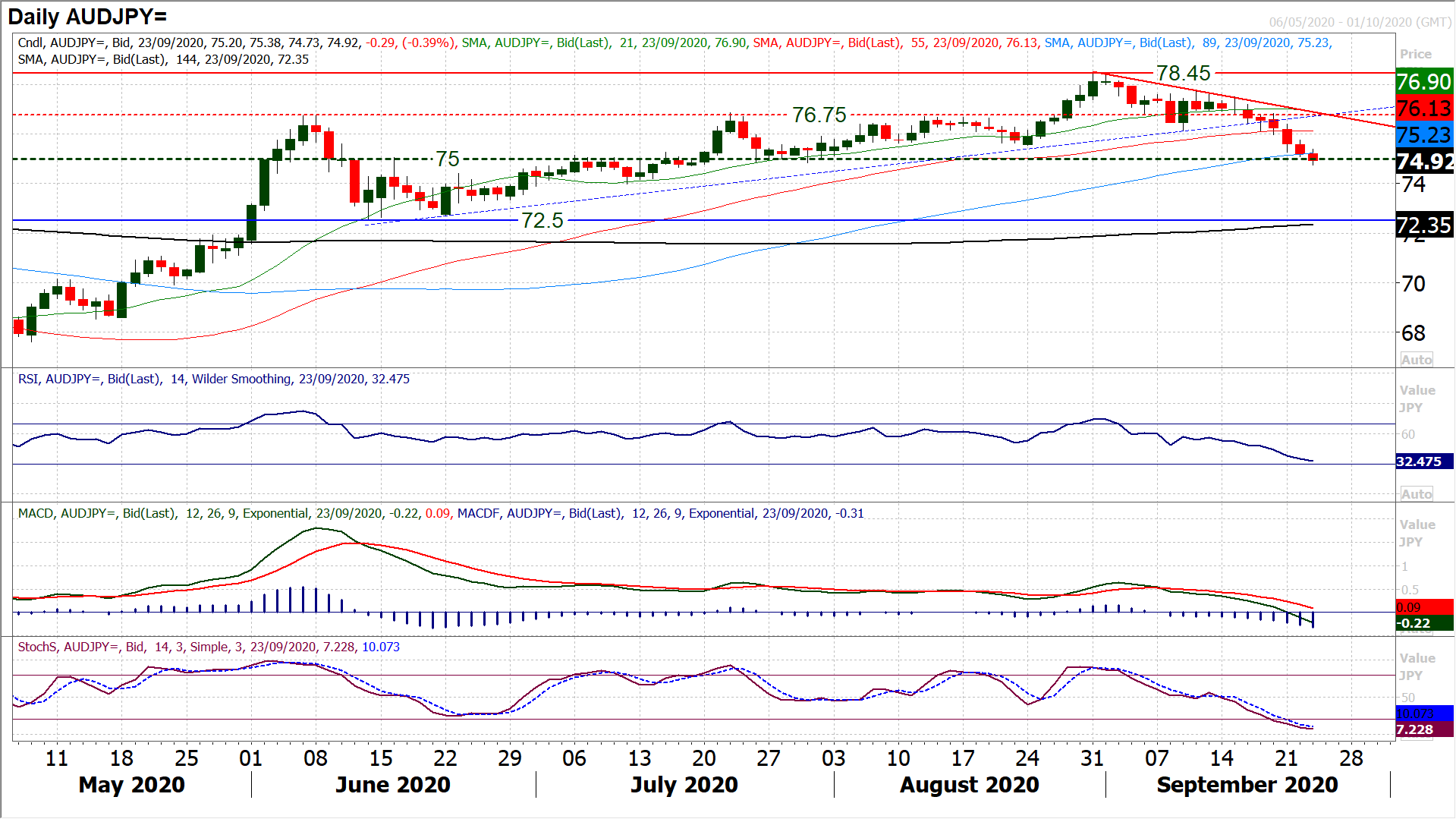

Chart of the Day – AUD/JPY

Aussie/Yen remains a classic signal for risk sentiment. So as risk appetite heads south in the early part of this week we have seen an acceleration lower on AUD/JPY. This move has dragged the cross back to the old June/July pivot at 75.00 again, a level coming under significant scrutiny early today. This seems to be a sharply deteriorating market right now, but a closing breach of 75.00 would effectively open the way towards 72.50 again. The concern for the bulls is that having broken the final (shallowest) uptrend (since mid-June) of the recovery late last week, the market is now building a new downtrend of lower highs and lower lows. The move below 75.55 in the last couple of days confirms the retreat now underway. A three week downtrend is in play, whilst momentum indicators are increasingly correctively configured. It suggests now selling into near term strength, with a band of resistance 75.55/76.10 being a band of overhead supply. On a close below 75.00 the initial support is 74.00.

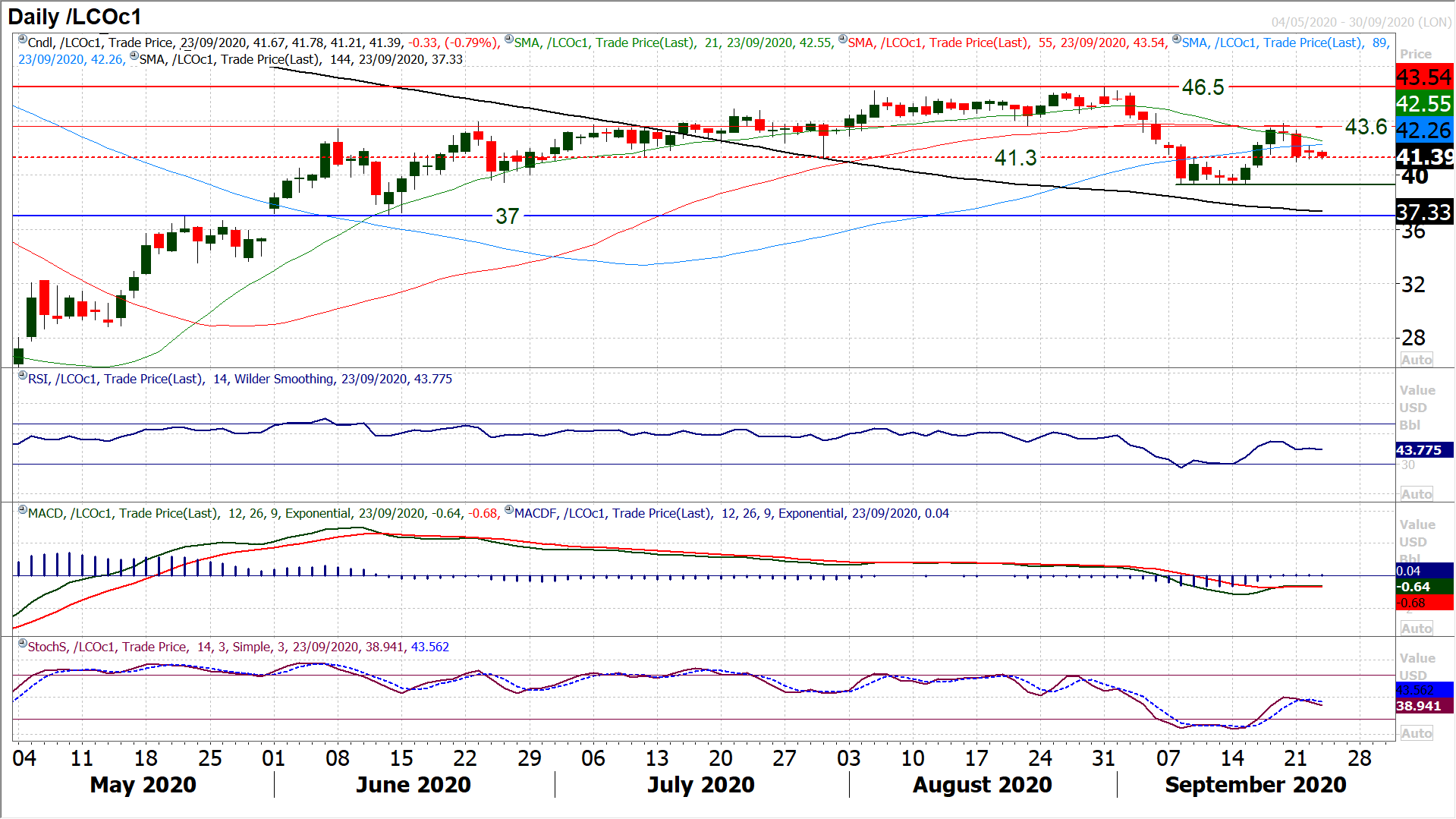

Brent Crude Oil

After the near term recovery fell over on Monday, a less certain outlook has begun to develop. An inside day (neutral candle) formed yesterday as support around $41.30 appeared to be holding. This support is under threat once more today as the market ticks back lower again. The mild negative bias to momentum suggests the ongoing pressure on this support, whilst if there is a closing breach, it would open the key $39.30 support again. Given the recent configuration of candlesticks, this is our preferred near term outlook now. The market needs to move back above $43.60/$44.25 resistance to enable a more positive outlook now.

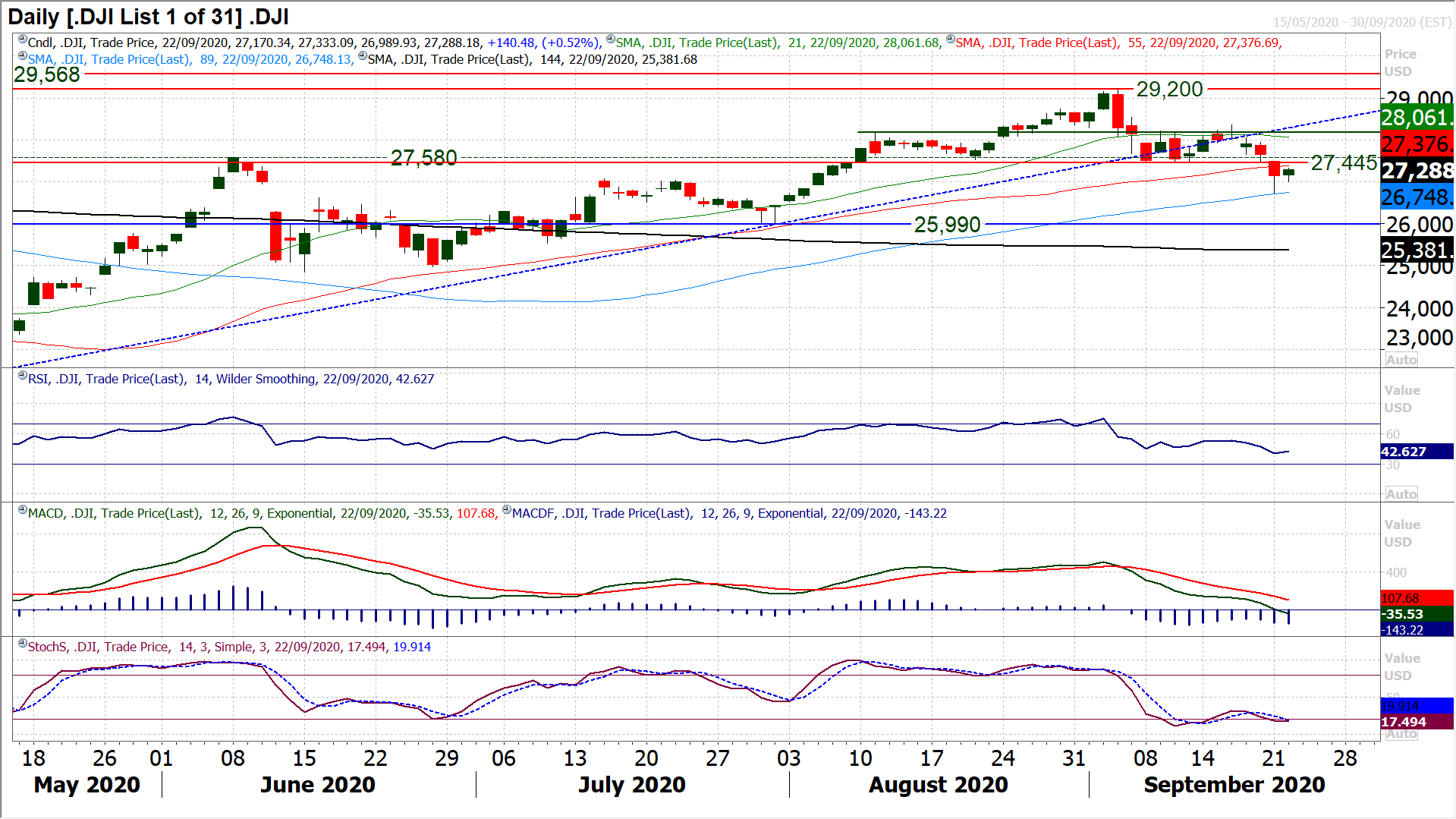

Dow Jones Industrial Average

The selling pressure may have eased slightly yesterday, but as yet there is no decisive recovery underway. Starting with the positives, the reaction since hitting Monday’s low of 26,715 has been positive. Closing above the session mid-point on Monday held a sense of encouragement, whilst yesterday’s positive candle has added to that. However, the key test remains the band of neckline resistance between 27,445/27,580. How the bulls respond around here will be crucial for the medium term outlook now. A failure in this rebound would put pressure back on 26,715 and the downside targets of the six week top pattern (c. 26,000) come into view. Momentum is still corrective and the fear is that rallies are a chance to sell now. A close above 27,580 is needed to begin to generate a more improving outlook.

Other assets insights

EUR/USD Analysis: read now

GBP/USD Analysis: read now

USD/JPY Analysis: read now

GOLD Analysis: read now

Author

Richard Perry

Independent Analyst