USD/JPY Forecast: The dollar sickens

- USD/JPY advance on trade completion partially reversed by China virus.

- Yen benefits from the risk aversion as illness spreads.

- Japanese statistics remain weak despite the US-China agreement.

The long rise in the USD/JPY from its late summer low of just below 105.00 and lately boosted to its highest level in seven months on the US-China trade pact reversed this week on risk aversion as the spread of the Corona virus in China and elsewhere became a major news story.

From its close on January 7th at 107.99 to finish at 110.18 on the 16th and 20th of this month the dollar yen gained 2% in seven trading sessions. This was a tribute to the unwinding of the trade war risk premium as much as a positive judgement on the US China pact. About half that rise was returned this week with the pair going to ground at 109.25 in afternoon action on Friday, a loss of 0.8%.

It is too soon for any judgement on the trade agreement to show up in US statistics. The very limited information from the economy in housing and jobless claims this week affirmed the continued American expansion and excellent labor market. Considerations for the status and impact of phase two negotiations, despite President Trump’s comment that he would be traveling to China, are not likely to be a topic until after the US election in November, all the more so while China is beset with a public health emergency.

The Bank of Canada’s mildly downbeat or perhaps wary is a better description, forecast for its economy undermined the loonie but as a general comment on the global outlook it is several months out-of-date as rate cuts from the Reserve Banks of Australia and New Zealand and the Federal Reserve can attest.

Middle Eastern tensions in Iran and the Persian Gulf largely dropped from the news and West Texas Intermediate reflected the lack of excitement losing 8.2% on the week and 17.4% from its January 8th high of $65.45 to $54.25.

In the US Senate the impeachment trial of President Trump continued with the Democrats presenting their case for removal to extensive media coverage and little public or market interest.

US statistics January 20-24

The US housing market continued its strong recent showing. Annualized existing home sales, about 90% of the total, climbed to 5.54 million units in December, its best rate since March 2018.

Initial jobless claims registered 211,000 in the January 17 week bringing the four-week moving average down to 213,250 which remains near a five decade low.

Purchasing managers’ indexes from Markit Economics of the UK for January were mixed. Services came better than anticipated at 53.2 on a 52.9 forecast and December's 52.8 score. Manufacturing continued to drag at 51.7, missing the 52.5 prediction and December’s 52.4 result. The composite index rose to 53.1 from 52.7, 52.5 had been projected.

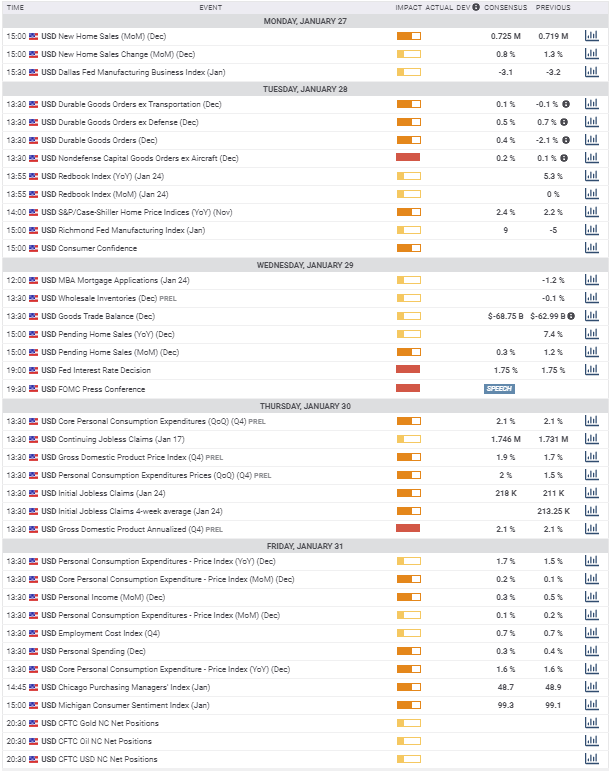

US statistics January 27-31

Next week is busy in the US with information on housing, durable goods, GDP and an FOMC meeting.

Monday sees new home sales for December with 725,000 annually forecast up from 719,000 in November. Purchases were 604,000 last May and their rise reflects a healthy housing market underpinned by employment. New home construction provides most of the jobs in the sector.

On Tuesday durable goods orders for December are released by the Census Bureau with a 0.4% gain expected. The 2.1% decline in November was largely due to a sharp drop in Defense Department procurement. A 0.5% gain is predicted in the ex-Defense category following November’s 0.7% increase and 0.1% is predicted in the ex-transport group.

The often cited proxy category for business investment, non-defense capital goods orders ex-aircraft, is forecast to rise 0.2% in December after November’s 0.1% increase and October’s 1.1% jump. Any improvement for this group will be taken as a preliminary indication that business investment is returning.

All durable goods categories will be watched for signs that the China trade agreement is starting to impact the economy.

Wednesday sees wholesale inventories for December. An inventory build after the November drop of 0.1% would suggest that businesses are preparing for improving sales.

The first Federal Reserve rate decision of this year is announced at 2:00 pm EST on Wednesday. Fed funds futures showed an 87.3% chance that the current target range of 1.50%-1.75% would be continued. Interestingly the balance was 12.7% for a 25 basis point increase. The main market focus will be on Chairman’s Powell’s press conference and his characterization of the US economy.

Annualized gross domestic product for the 4th quarter will be released on Thursday. The preliminary estimate is expected to be 2.1%.

Inflation resurfaces on Friday with the personal consumption expenditures price indexes (PCE) for December from the Bureau of Economic Analysis, a division of the Commerce Department. Core prices are projected to increase 0.2% on the month in December and 1.6% on the year. As the core PCE index is the Federal Reserve’s preferred inflation measure it has a higher market impact than the older CPI. Overall price gains will be 0.1% and 1.7%. Core inflation has not been at the bank’s 2% target since August 2018.

Personal income and spending for December are also issued with 0.3% expected for each. Income is a broader measure of household revenue than average hourly earnings as it includes a number of transfer payments.

The Michigan Consumer Sentiment final figure for January is released at 10:00 EST, a slight gain to 99.3 from 99.1 is anticipated.

On a comparative basis with Japan American statistics should provide the dollar with an edge, risk aversion trading excepted.

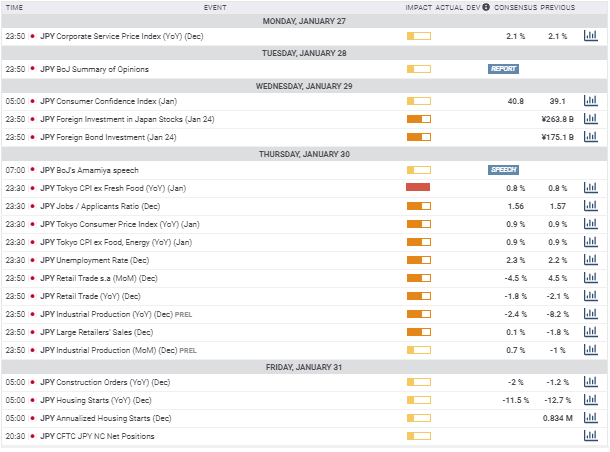

Japan statistics January 20-24

Economic statistics would likely have contributed to a yen decline this week but for the threat from the virus in China.

Industrial production for the year dropped 8.2% and 1% on the month in November. The annual decline was the worst in five years and the month to month slippage followed October's 4.5% plunge which was the worst since 6.8% in January 2018.

Exports and imports were lower on the year in December, 6.3% and 4.9% respectively both worse than their -4.2% and -3.4% forecasts. Imports were down 15.7% in November, 14.8% in October and have fallen for eight straight months. Exports decreased 6.3% in November and 7.9% in October and have fallen for 13 months at an average of 5.5% per month.

The coincident index, a measure of current economic activity fell to 94.7 in November from 95.3 the prior month. Activity has fallen steadily for the last two years from 119.7 in December 2018.

Inflation continued to be weak with core CPI at 0.9% in December and the overall at 0.8%. The core rate has been below 1% since March 2015.

Japan statistics January 27-31

Consumer confidence for January on Monday is expected to be 40.8 up from 39.1 in December. Last September saw an eight year low of 35.6.

The decline in industrial production is forecast to moderate in December with a preliminary figure of -2.4% year on year. Monthly production is projected to climb 0.7%.

The job to applicants’ ratio for December is expected to slip to 1.56 from 1.57 and the unemployment rate to rise to 2.3% from 2.2%.

Sales at large retailers should rise 0.1% in December after a 1.8% gain in November and construction orders will drop 2% after falling 1.2% in November and rising 6.4% in October.

Japanese statistics continue to show that the economy has yet to find a firm footing for expansion despite more than four years of negative interest rates form the Bank of Japan.

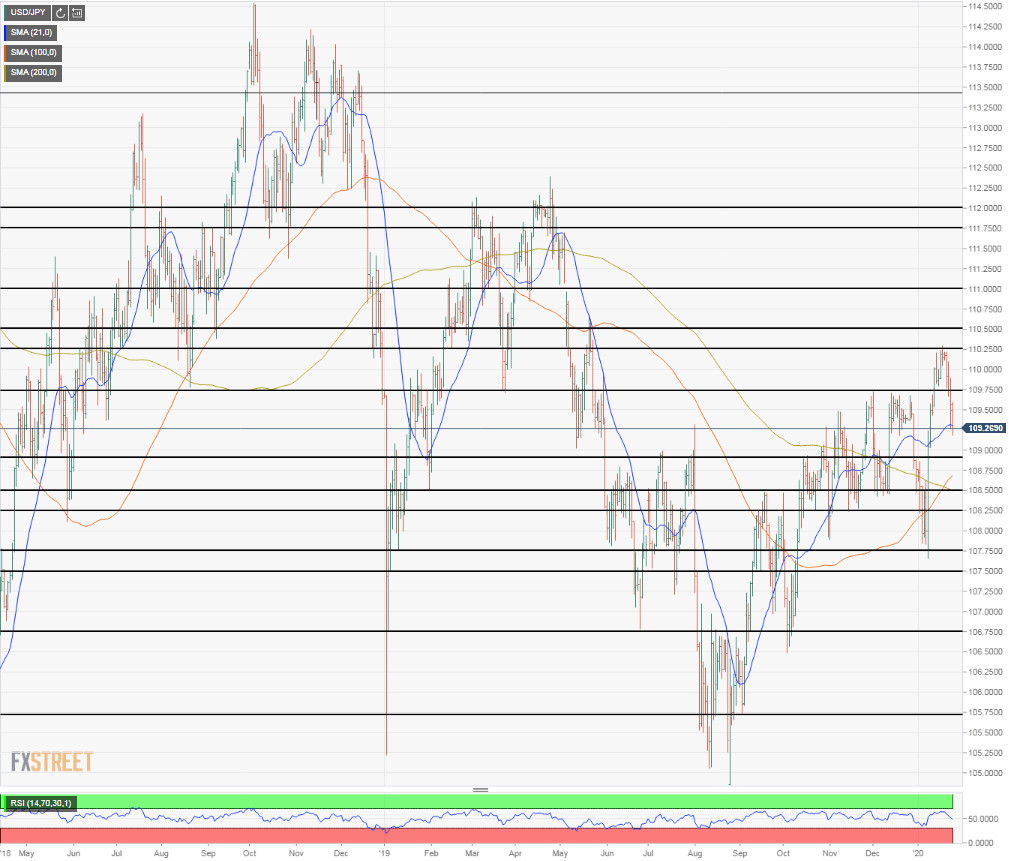

USD/JPY technical outlook

This week's decline in the USD/JPY was without technical input except for the brief pause on the way down at 109.60 the top in late November and most of December.

The 21, 100, and 200 day moving averages are mixed with the 21 and 100 reflecting the fourth quarter rise in the dollar yen while the longer indicator has not lost the influence of the April to August plunge from 112.00 to 105.00. The relative strength index (RSI) is nearly neutral with the climb and partial reversal of the last two weeks.

Initial support is at 108.80 then 108.50 both marked by price action in October and November. Next are three weak lines at 108.25, 107.75 and 107.50. Substantial support is found at 106.75 the top for most of August and early September and the average lows in the first week of October. Long range 105.75 offer solid support.

Immediate resistance is at 109.75 followed by the recent high at 110.25. Beyond that we have to return to the first half of last year for comparison. Last February 110.50 served as a bottom for much of the month but its strength is undermined by subsequent price action in March and again in May. An aggregate collection of tops and bottoms from March to May at 111.00 offers moderate resistance, in addition to the well known USD/JPY penchant for trading at figures. A weak line follows at 11.75 and a stronger one at 112.00.

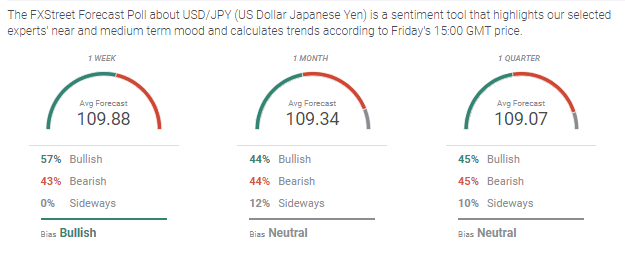

USD/JPY sentiment

Analyst sentiment remains upbeat in the one week view despite the decline over the last trading sessions with bullish attitudes rising to 57% from 50% and bearish outlooks also gaining to 44% from 36%. Neutral sentiment fell from14% to an unusual 0%. The average forecast not surprisingly slipped to 109.88 from 110.33.

In the one month view bullish sentiment rose to 44% from 33% as bearish dropped to 44% from 58% with neutral edging higher to 12% from 9%. The forecast declined to 109.34 from 109.66.

At the 30 day view bullish feelings recovered to 45% from 32%, bearish was 45% this week and 46% last, with the neutral outlook the big loser at 10% from 22%. The forecast continues lower at 109.07.

Views of USD/JPY this week have been conditioned by the risk aversion spreading from China. It is at odds with the general bullish view for the USD/JPY but until the health crisis relents it will likely dominate trading.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.