USD GBP and CIT

USD

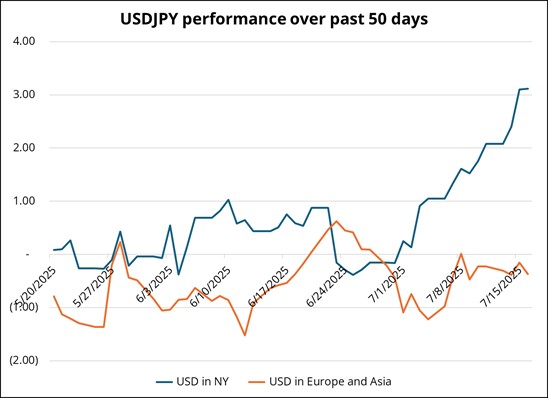

The NY time zone continues to buy USD as CTAs unwind USD shorts and the US data fails to offer any sort of cyclical reasoning for bearish USA views. Inflation data have been mixed with mildly worrisome CPI components and PPI weak with stonking upside revisions. USDJPY has been spicy, time-zone wise, as it has rallied in a straight line since July 1 and all this rallying has been in the NY time zone.

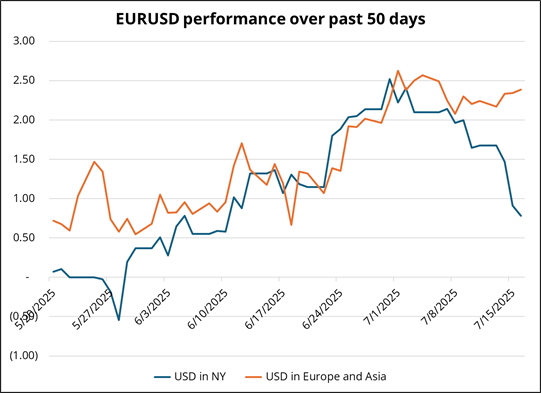

Perhaps the CFTC is getting bored of its massive long JPY position and the prohibitive carry involved. While interest rate differentials have gone substantially lower in USDJPY as Japanese yields continue to rip, the price of sitting there short USDJPY remains high. EURUSD tells the same time zone story. NY is buying USD.

UK

UK CPI data was a disappointment for GBP bears, but overall the pound has not reacted much. UK jobs data tomorrow are now in focus and will be the key to determining the P&L of my 1.3410 GBPUSD put. The jobs market signal from the

KPMG UK Jobs Report for June was unequivocally soft, but the official UK employment data we get tomorrow is for May. A weak jobs result should more than offset the strong CPI data as it will send a picture of stagflation looming over one of the three countries that markets have labeled as deficit sinners. Japan and the USA are the other two.

Here’s a summary of the June KPMG report. You can read the whole thing here.

-

Hiring Activity Drops Sharply: Permanent placements fell at the fastest rate in nearly two years, while temp billings also declined, driven by business uncertainty and tighter budgets.

-

Candidate Supply Surges: Staff availability rose at the steepest pace since November 2020 due to redundancies and reduced hiring demand.

-

Pay Growth Weakens: Starting salaries and temporary wages grew only modestly, reflecting lower demand for workers and improved labor supply.

-

Vacancies Continue to Decline: Demand for permanent roles dropped significantly; only Construction and Engineering showed slight increases in job postings.

Again, this report was for June, while the May KPMG report was softish, but not dramatic. If we get a weak jobs report tomorrow, the targets for the move are the minor support on the chart in light blue at 1.3335, and the bigger support in red at 1.3250. In the dream scenario of a move down that way, I will scale out of shorts as 1.3250 nears and be flat if it trades there.

Tariffs

I get the impression that one of the reasons the US government cannot achieve its impossible goal of signing trade deals with a zillion trading partners in a short time is that some countries are slow-playing the process in the hopes that the tariffs will be ruled illegal. The most recent 50% tariff on Brazil adds a new level of whim to the story as those tariffs clearly have nothing to do with any economic or national security emergency. Why sign a trade deal under the threat of tariffs when those tariffs are potentially illegal and could be vetoed by the courts?

In May, the U.S. Court of International Trade (CIT) ruled that President Trump exceeded his authority under the International Emergency Economic Powers Act (IEEPA) by imposing broad "reciprocal" and “fentanyl” tariffs. The court

permanently blocked these tariffs. Shortly after, the Court of Appeals for the Federal Circuit granted a temporary stay of that ruling and allowed the tariffs to remain in effect during ongoing litigation. Oral arguments in the Federal Circuit are scheduled for July 31, 2025. This will cover both the broader collective challenge (CIT) and a related case from the DC District Court involving small toy companies.

The appeals will determine:

-

Whether IEEPA grants presidents the power to impose tariffs at all, or only under narrow, specific emergency circumstances.

-

If those limitations were violated, whether the preliminary block by CIT stands.

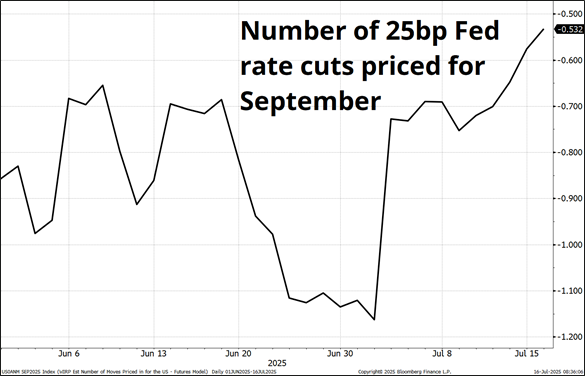

The process could take 2-4 weeks, and a ruling is expected at some point in August. More uncertainty for the Fed to consider as it waits for clarity on the on-again / off-again tariffs. What the Fed does know right now is that unemployment is low, inflation is above target and rising, and deficits are increasing faster now than they were last year, despite four years of soft landing in the United States.

It makes sense that September rate cut odds are falling because Team ZeroDots has all the facts on their side for now while Team TwoDots wants to be proactive based on a sketchy belief that the Fed is restrictive.

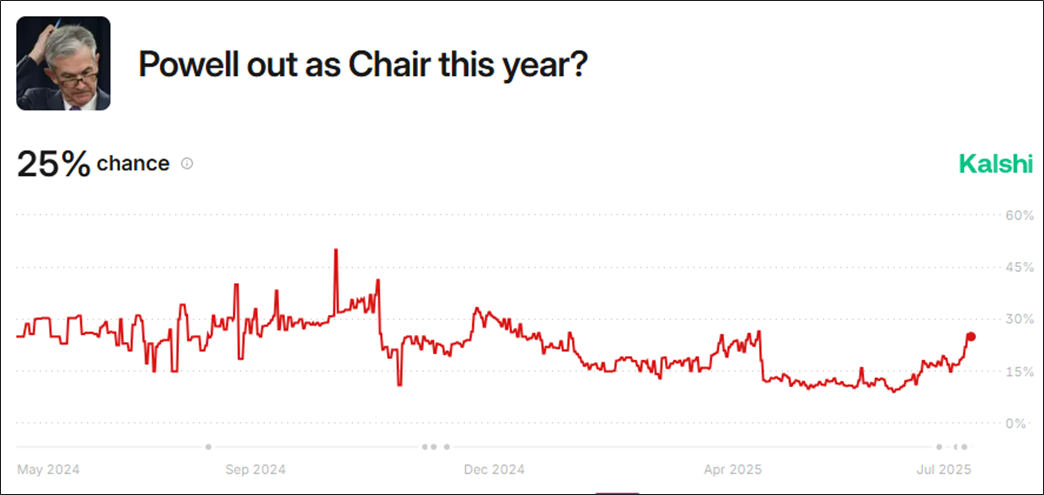

Powell

Trump’s MO is to find esoteric legal reasons to take actions that might otherwise be prohibited by normal precedent. The investigation into the Fed’s HQ cost overruns (and related perjury accusations against Powell) are the latest incarnation of this strategy.

If Powell resigns or is fired, expect a massive fall in the back end of the bond market as the market shoots first and asks questions later on the embrace of a more Turkish style of monetary policy. This would be a move towards more central planning in the USA (on top of industrial policy, sectoral strategies, partial nationalization of rare earths, outright choosing of winners and losers in tech, etc.). It would trigger capital flight and would be negative for the dollar. 25% feels about right to me, though it feels like it’s too random of a variable for markets to price in right now.

If you can find a market maker who will sell (USD down 5% / US 30-year yields up 50bp) dual digitals, they’re probably cheap!

Author

Brent Donnelly

Spectra Markets

Brent Donnelly is the President of Spectra Markets. He has been trading currencies since 1995 and writing about macro since 2004. Brent is the author of “Alpha Trader” (2021) and “The Art of Currency Trading” (Wiley, 2019).