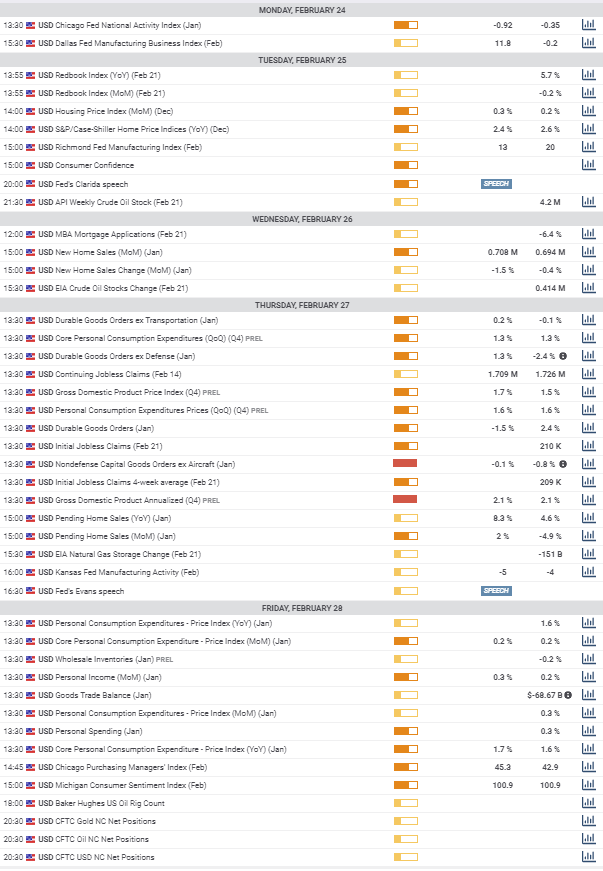

USD/CAD Forecast: The US economy in focus and under question

- Weak Markit PMIs for the US in February hit USD/CAD.

- Core Canadian inflation unchanged in January, headline higher.

- Retail sales flat in January, December revised up.

The USD/CAD meandered down from its breach of 1.3300 for the first four days but the unexpectedly weak Market PMI numbers for the US on Friday brought the USD/CAD to its low for the week at 1.3202 though1.3200 remained intact. As per the last seven sessions ranges were limited averaging 42 point a day through Wednesday, 57 points on Thursday and 66 on Friday. Trading opened at 1.3250 on Monday and closed at 1.3218.

The USD/CAD restraint was uncommon as the euro and the yen fell to fresh lows, of 34 and nine months respectively, on weak data from Germany and Japan and then reversed modestly on Friday’s surprise US manufacturing information.

American statistics initially showed promise, especially in manufacturing, which was later countered, while Canada’s figures depicted an economy marking time. Neither set provided a rationale for movement in the pair.

Canadian and US statistics February 17-21

Canadian manufacturing sales for December were disappointing at -0.7% far below the 0.5% forecast and November’s result was revised to -1% from -0.6%. Sales have dropped for four straight months in the longest run since 2012 though the -0.525% average is less than -0.97% average for October, November and December 2018.

Consumer prices were as expected with the annual core rate up 0.1% in January to 1.8%, 0.4% on the month. The overall inflation pace rose to 2.4% from 2.2% and the January rate was 0.3% from flat in December.

Private sector employment in the ADP report was weaker in January than anticipated, 25,900 against 71,800 and down from Decembers 46,200. The ADP results have been much stronger for the last six months averaging 40,000 per than the national employment figures form Statistics Canada which have been 16,000.

Retails sales in December were slower in the headline, flat against a forecast gain of 0.1% but with an upward revision to November 1.1% from 0.9%. The ex-auto figure was 0.5% on a 0.4% prediction and the prior month was adjusted to 0.5% from 0.2%.

American statistics were good this week until Friday though providing little support for the USD/CAD.

The New York Fed’s Empire State Manufacturing Survey jumped to 12.9 in February from 4.8 in January, nearly doubling the 7.9 forecast. It was the best reading for this index since May. New orders surged to 22.1, the best since September 2017 and shipments climbed to 18.9, the highest since November 2018.

The FOMC minutes of the January 28-29 meeting on Wednesday reinforced the governors' optimistic view for the US economy while noting the unknown impact of China’s corona virus on global growth. Housing starts and building permits for January reflected the strong housing market with the boom in permits, up 9.2%, and the far smaller than expected decline in housing starts likely a reflection Januarys warm weather in much of the country.

The Philadelphia Manufacturing Survey for February on Thursday, like the New York version, was far better than projected soaring to 36.7, well above both the consensus prediction of 12 and the January score of 17. It was the highest for this gauge since February 2017 and the second best level in 27 years. The new orders index soared from 18.2 in January to 33.6 in February, its highest since May 2018. This measure has more than tripled in three months from December’s 11.1 reading.

Market Economics of the UK provided a surprise on Friday with both their PMI’s for February dropping, manufacturing to 50.8 from 51.9 and services to 49.4 from 53.4, in the first dip below 50 since February 2016.

The striking difference between this survey and the two Fed indexes mentioned above may be due to the more export oriented manufacturing outside of the Northeast home of the Philadelphia and New York Federal Reserve Districts. We will know more on March 2 and 4 when the nationwide Institute for Supply Management PMI Surveys are released.

Statistics conclusion

Competing statistics from Canada and the United States did not alter the overall disposition of the nations’ currencies. +

Of the week’s three US surprises, two, the better than forecast Fed manufacturing surveys had little impact on the USD/CAD. The weaker than predicted Markit indexes drove the USD/CAD to the week’s low at 1.3202 and back below the start line of the technical higher run of February 3. .

Like the effect on the EUR/USD and USD/JPY which saw dollar losses on the release, the Markit PMI numbers tempered some of the optimism from recent US statistics. If the London firm is seeing the first effect of China’s economic slowdown the sense of US immunity will fade and this should draw some of the dollar’s recent strength.

Canada statistics February 24-28

Wholesale sales are expected to rise 0.8% in December after falling for 1.2% each in October and November. As the retails sales figures for December are already in, this number will give no new information.

Fourth quarter GDP on Friday is forecast to drop to 0.2% from 1.3% in the third and 3.5% in the second. If accurate it will confirm the sharp slowdown in the Canadian economy at the end of the year and could undermine the loonie.

FXStreet

US statistics February 24-28

Durable goods for January on Thursday are expected to fall in the headline to -1.5% from 2.4% in December but to rise 1.3% from -2.4% in the ex-defense category as recent Defense Department procurement fades. The ex-transportation number is predicted to gain 0.2% after December's 0.1% drop. Finally the non-defense capital goods ex aircraft group, the analog for business investment, is forecast to decline 0.1% after the revised 0.8% fall in December. Fourth quarter annualized GDP should be unchanged at 2.1% in its first revision.

Friday's PCE price index and its core version for January are the Federal Reserve's chosen inflation measures. With the core rate forecast to rise 0.1% to 1.7% price status quo is maintained and the Fed will again be able to assert when asked that inflation will rise over time to its 2% target. Consumer confidence in the Michigan Survey is predicted to be unchanged at 100.9 upon revision.

Statistics Conclusion

The Markit PMIs will bring this week’s information into acute focus. Any indication that the anticipated slowdown in China’s economy is crossing the Pacific will likely drain strength form the US dollar. Its February ascent has been based on the anticipated performance of the US economy being substantially better than its rivals. The durable goods non-defense business category will be of particular interest as the drop in business investment in the second half of last year and its anticipated revival with the completion of the US-China and USMCA accords is one of the keys to the success of the economy this year.

FXStreet

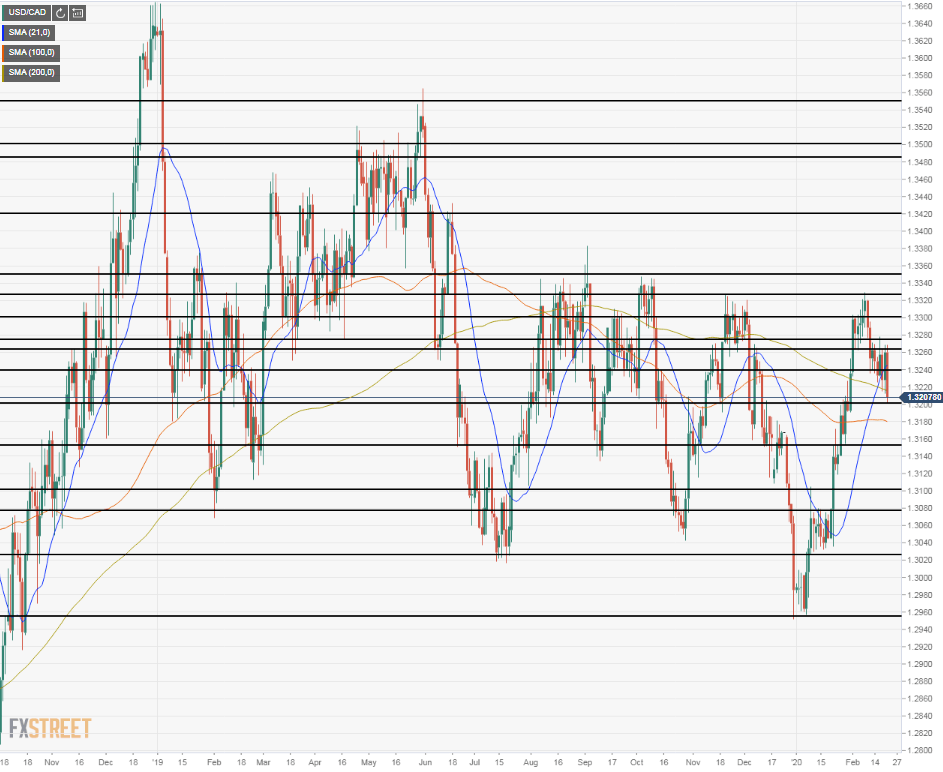

USD/CAD technical outlook

The limited ranges from 1.3202 to 1.3279 this week have preserved most of the technical scheme of recent sessions.

The 21-day moving average remains positive but the decline of the past two week, minor though it was has shifted the 100-day average to slightly negative, mostly due to the Friday fall and reinforced the 200-day downward cast.

Last week's support at 1.3240 is gone, crossed each day this week. The first line is 1.3200 followed by 1.3150 and 1.3100 in quick succession. All relate to levels prior to December and are moderate to strong. The weak line at 1.3080 is from December and unlikely to resist any but mild pressure. The resistance at 1.3025 held in January and again in July of last year and is more substantial. The line at 1.2955 is important mainly as the 16 month low, there was little volume at that level.

First resistance is now 1.3240 followed by 1.3260 both set by this week's trading. Above is 1.3275, 1.3300,1.3330 and 1.3350 all relating to ranges in the second half of the year. The area between 1.3400 and 1.3500 was traded almost continually from late April to early June and will absorb most technical penetration with lines at 1.3425 and 1.3485. Above that is a strong line at 1.3500 and a weak one at 1.3550.

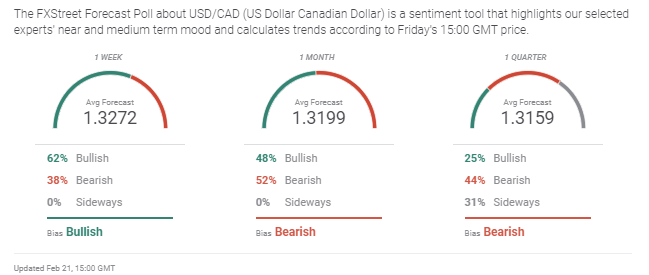

USD/CAD sentiment poll

The lack of upward movement in the USD/CAD is weighing on the outlook.

One week sentiment is heavily bullish at 62% vs 47% with the balance coming from bearish 38% from 47% and neutral 0% from 5%. The forecast is marginally higher at 1.3272 from 1.3253.

The one month outlook is mildly bearish with a higher bullish score, 48% vs 33%, a weaker bearish 52% vs 63% and flat vs 4% in neutral. The forecast is lower at 1.3199 va 1.3218.

Out one month the bearish tendency remains but far weaker: bullish 25% vs 14%, bearish 44% vs 53% and neutral 31% vs 33%. The forecast is 1.3150 against 1.3144.

Improving US economic statistics have been the greenback's main support but the lack of conclusion on the economy and the late week doubt from the Markit PMIs, even though unknown at the time of the survey are reflected in the overall longer term uncertainty about the US dollar.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.