USD/CAD forecast: For the time being, it's still the US dollar’s game

- Early signs that the risk avoidance trade may be ebbing.

- Record US unemployment filings claims did not boost USD.

- Euro, yen and Canada gain after 3 weeks and 16.76 million US claims.

- WTI pullback on Friday did not weaken Canadian dollar.

The USD/CAD broke back below 1.4000 for the first time in six sessions on Tuesday as the continuing dissolution of the US labor market failed to excite further risk-aversion fears and the Federal Reserve unveiled a $600 billion lending program for medium sized business part of a $2.3 trillion package to support local and state governments and companies with loans and securities purchases.

OPEC and Russia agreed on a tentative production deal which would cut about 10 million barrels a day in May and June. Saudi Arabia and Russia, the largest producers, would reduce their output by 8.5 million a day and all members would cut their supply by 23%, according to news reports.

The deal is conditional on Mexico’s approval. Energy Secretary Rocio Nahle Garcia said on Twitter after the Thursday meeting that her country is willing to reduce output by 100,000 barrels far less than the 400,000 assumed in the agreement.

This attempt to support oil prices with supply restrictions is far larger than previous efforts by the cartel and is backed by US President Trump. North American shale companies are under severe financial pressure from the more than 50% collapse in crude prices this year. Production costs in the shale fields are generally higher than the more traditional extraction in the Middle East and Siberia.

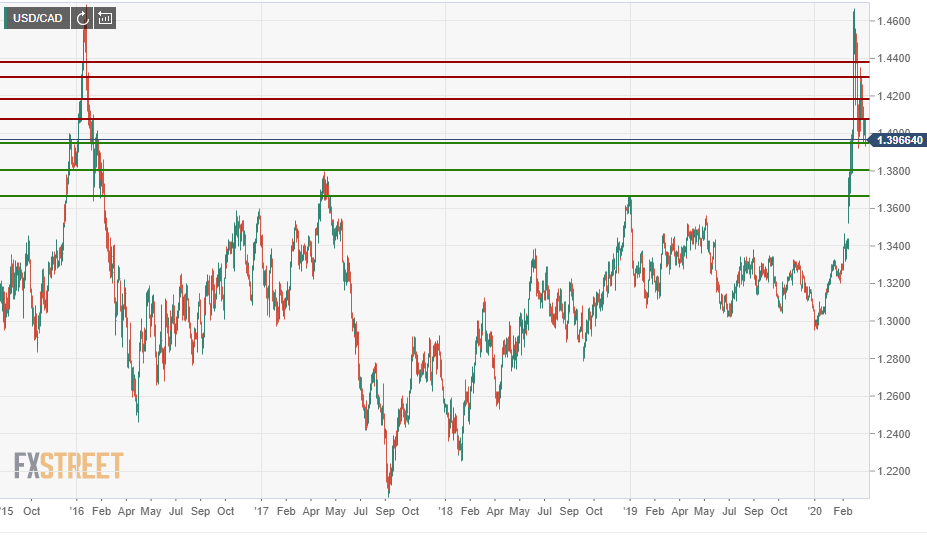

Signs that the pandemic is easing in the US and Europe improved risk sentiment throughout the week. The USD/CAD fell 1.8% and is back to the level of mid-March before the most aggressive Coronavirus inspired fears drove the pair to 1.4668 on March 19, the highest price in four years and the second highest since 2003. The euro gained 1.3% versus the dollar on the week and the USD/JPY was static opening at 108.53 and closing just 10 points lower, though it was down from Monday’s 109.38 high.

USD/CAD outlook

Economic damage around the world from the public health measures instituted to cope with the Coronavirus has taken concrete shape with the astonishing US and Canadian jobs losses.

In the US almost 17 million people, 10% of the workforce, have filed for unemployment insurance in the last three weeks. In Canada one million workers lost their positions in March and the unemployment rate jumped to 7.8% from 5.6%, its highest since February 2011.

Market risk is a matter of perception. In the ascending phase of the crisis in early March the extent of the pandemic and its economic effects were largely unknown but subject to the worst interpretations. The US dollar and US assets were, as they have always been, the refuge of choice.

The actual job losses in the US and Canada were far higher than expected but they are now known instead of conjecture and if the knowledge is not reassuring is quantifiable.

Five factors began to tilt the risk balance away from the US dollar and toward the loonie this week.

First, the pandemic has started to moderate in several countries in a fashion that may predict its end. Second, infection, hospitalization and fatality rates in the US are proving to have been widely exaggerated when compared to real numbers and the models have been adjusted lower by large multiples. Third, government support programs from Washington and Ottawa and the Federal Reserve and the Bank of Canada have restored market confidence in the functioning of the financial system and, more hopefully, that some of the economic pain from closures can be mitigated. Fourth, talk in DC is slowly shifting to how and when to reopen the economy. Fifth, the OPEC production deal, if approved, should put a floor under crude prices until the reviving global economy increases demand.

None of these developments are assured but if they continue the US dollar’s risk premium, in general and against the Canadian in particular, will slowly drain away and the stage will be set for Dollar Canada to return to pre-crisis levels.

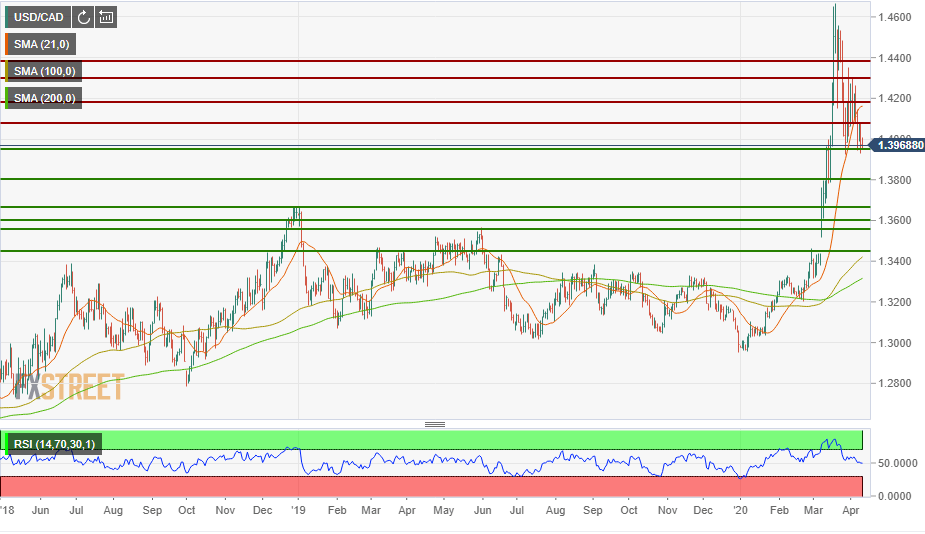

The USD/CAD is supported at 1.3950, 1.3800 and 1.3660 but the rapid nature of the price movement in the last month and the fundamental motivation means that these levels will not endure much pressure. The same stipulations apply to the resistance lines at 1.4075, 1.4180, 1.4300 and 1.4380.

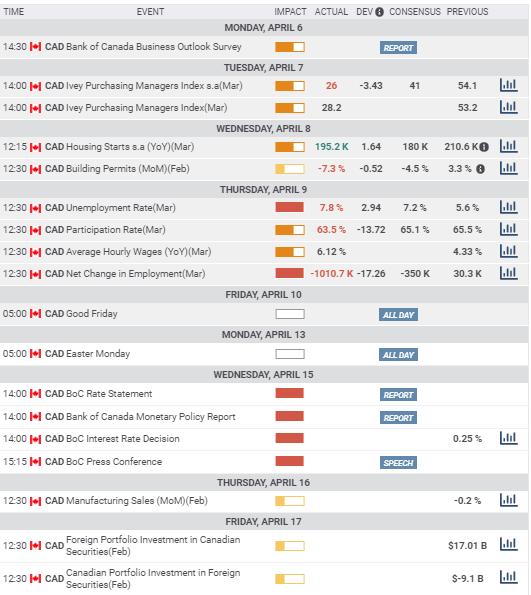

Canadian statistics April 6-10

Monday

The Ivey purchasing managers’ index for March was much worse than forecast, a general refrain this week, coming in at 26 on an estimate of 41 and a February score of 54.1.

Tuesday

Housing starts on the year in March were better than expected at 195,200 for an 180,000 prediction but down from February’s 210,600.

Friday

The unemployment rate in March jumped to 7.8% from 5.6%, 7.2% was forecast. The net change in employment was -1,010,700, almost triple the -350,000 estimate, and like the US unemployment claims and non-farm payrolls to come, by far the highest in Canadian history.

April figures will likely be even higher as Statistics Canada said its survey was completed before the full impact on employment.

Since March 15 more than five million people have applied for all forms of federal unemployment assistance suggesting that the jobless rate may be closer to 25%.

Canadian statistics April 13-17

Wednesday

Bank of Canada rate decision, policy statement and news conference with Governor Stephen Poloz. With Canadian rates at 0.25% and Canada’s first quantitative easing program underway there are unlikely to be any new policy developments though he will be questioned on the bank’s prognosis for the economy.

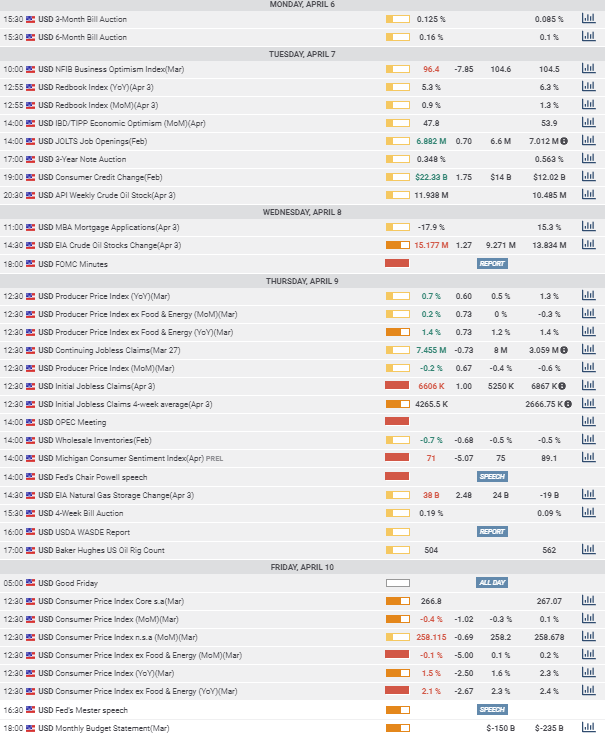

US statistics April 6-10

Tuesday

Redbook Index Y/Y for the week of April 3 dropped to 5.3% from 6.3% and 9.1% the two prior weeks.

JOLTS jobs openings were 6.882 million in February down from 7.012 million in January and a bit of nostalgia for the pre-virus labor market.

Wednesday

The FOMC minutes from the emergency March 15 meeting added little to the Fed’s public explanations for its recent actions with no specific mention of financial market stresses.

Thursday

Initial jobless were worse than expected in the April 3 week, 6.606 million vs 5.256 and followed a revised record in the prior week at 6.867 million from 6.648 million. Continuing claims rose to 7.455 million surpassing the previous financial crisis record of 6.883 million on June 27, 2009.

Friday

Consumer prices fell 0.4% in March after February’s 0.1% increase and annual gains dropped to 1.5% from 2.3%, -0.3% and 1.6% had been forecast. Core rates fell to 2.1% on the year from 2.4% and to -01% from 0.2% on the month.

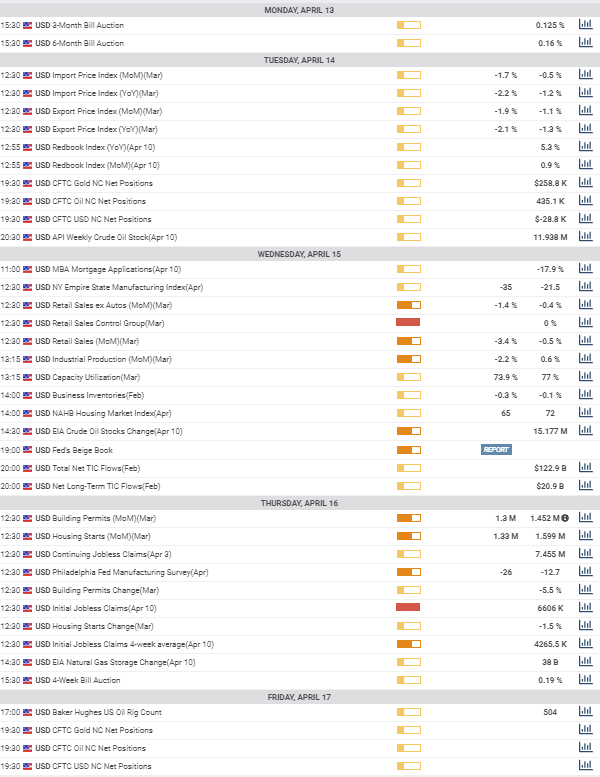

US statistics April 13-17

Wednesday

Retail sales for March will give the first substantive view of the consumer impact of the job losses. Overall sales are expected to fall 3.4% after February’s 0.5% drop. Ex-autos should fall 1.4% from -0.4%. The control group was flat in February.

Industrial production is slated to decrease 2.2% in March; it rose 0.6% in February.

The Fed’s Beige Book assessment of the US economy prepared for the April 28-29 FOMC meeting will deploy the bank’s careful language in its anecdotal description of the catastrophe that has overtaken the US economy.

Thursday

Initial jobless claims. After three weeks of record job losses with almost 17 million new claims market will be looking for any sign that firings are easing.

US statistics conclusion

The detailing of the collapse of the labor market from record performance to debacle in three weeks was the only statistic that mattered this past week. Though as noted above its power to shock markets into risk-aversion positioning has diminished.

Ahead March retail sales will begin to bring the wider economic implications for the consumer driven US economy into focus. A much worse than expected figure will suggest the same for April and US GDP in the first and second quarters. With estimates for economic growth in the first three months having dropped from 3.1% to 1% in the Atlanta Fed model and for April, May and June varying from -5% to -20% and lower, retail sales figures tending to confirm the larger loss projections could bring the risk trade back to prominence and return support to the US dollar.

USD/CAD technical outlook

The relative strength index has returned to neutral on the week's modest decline in USD/CAD. As was true last week all three moving average remain tilted higher.

These four indicators give a somewhat false impression of the prospects for the USD/CAD in the weeks ahead. The almost 10% rise in the pair since early March was predicated on the risk flight to the US dollar. As that fear ebbs and the premium for the US currency erodes the return of Dollar Canad to pre-crisis trading ranges become more likely.

Resistance: 1.4075; 1.4180; 1.4300; 1.4380

Support: 1.3950; 1.3800; 1.3660; 1.3600; 1.3555; 1.3450

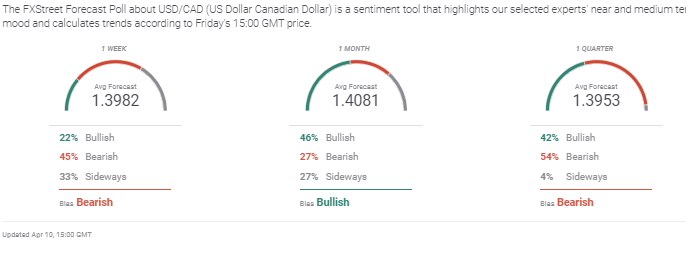

USD/CAD sentiment poll

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.