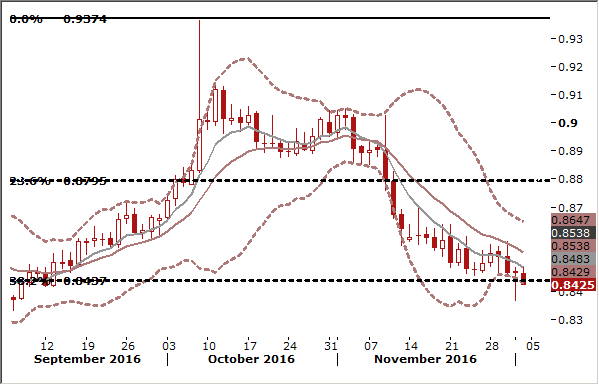

USD/CAD: 1.3320 broken, now eyes on twin jobs report

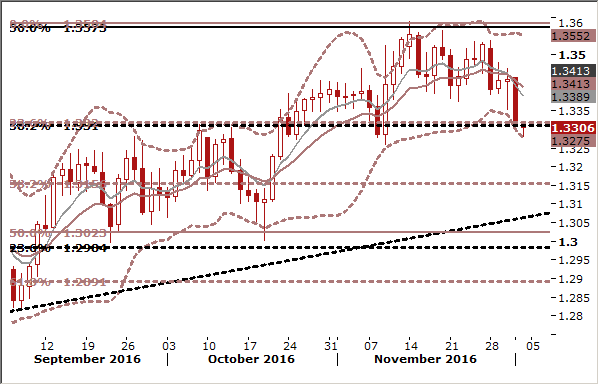

EUR/GBP: Bears are looking for weekly close below 38.2% retrace

-

The GBP struck multi-month highs on Thursday, adding to its biggest monthly gains against the euro since 2009, after Britain's Brexit minister said the government would consider paying into the EU budget for market access.

-

Asked on Thursday by a lawmaker if the government would consider making "any contribution in any shape or form" for access to the EU's single market, David Davis said it would. Davis's comments chimed with hints from British Prime Minister Theresa May earlier this month that she could be open to some form of transitional agreement with the EU, easing fears about the disruptions Brexit may bring.

-

Growth in Britain's construction industry unexpectedly touched an eight-month high in November, but its costs rocketed at the fastest pace since 2011, fuelled by sterling's slump after the June vote to quit the European Union. UK construction PMI edged up to 52.8 from 52.6 last month, helped by improved readings for commercial and civil engineering activity, as well as solid growth in house building. Construction firms quickened their pace of hiring for a fourth month in a row, with jobs growth hitting a six-month high.

-

A hammer formed on Thursday’s candlestick line makes the near-term outlook mixed. While bears managed a breakthrough below 38.2% retrace of the 2015-2016 rise, a weekly close below this level is needed to sustain the weakness into next week. We stay short with the short-term target at 0.8350.

USD/CAD: 1.3320 broken, now eyes on twin jobs report

-

The Canadian dollar hit a three-week high against the USD and bond yields rose on Thursday as oil extended a rally after major petroleum producers agreed to cut output. The USD/CAD dropped despite strong U.S. ISM reading.

-

U.S. ISM Manufacturing PMI beat expectations (52.2) for a more modest rise, climbing 1.3 points to 53.2. That makes it tied with June for the best print since March 2015. Factory survey data have been broadly improving, though keep in mind that this may represent the post-election sentiment bump that we have seen across all sorts of survey data, and which may prove ephemeral. It is in line with our general short-term expectations for the sector, helped in part by a cessation in energy investment's decline, but we continue to warily eye the impact of dollar strengthening. The production index rose 1.4 to 56.0, a clear 22-month high, but the new orders index was a little worrying; it only rose 0.9 to 53.0, still under the average of 54.3 for the year through October. Moreover, backlogs continued shrinking, though at least at a decelerated pace, with that index up 3.5 to 49.0. Employment remained well above trend, down 0.6 to 52.3, still not suggesting a huge wave of hiring. Inventories were said to be contracting for a 17th straight month, that index up 1.5 to 49.0. Trade growth slowed, with the exports index down half a point to 52.0 and imports down 1.5 to 50.5. We would expect the numbers to remain mild in the near future, turning more in favor of import growth.

-

The CAD appreciation was also the result of Wednesday’s Canadian GDP growth data that showed the fastest pace in more than two years in the third quarter. Canadian economy benefited from a rebound in oil exports, cementing expectations that the Bank of Canada will keep interest rates steady next week.

-

USD/CAD traders will be focused on today’s jobs report from the U.S. and Canada (13:30 GMT). The market expect that U.S. employers added 175kjobs in November, although much-better-than-expected ADP reading on Wednesday may have strengthened expectations for an upside surprise. Canadian economy is expected to have shed 20k jobs in November after two months of strong gains.

-

The USD/CAD broke below key support at 1.3320 (23.6% fibo of May-November gains) today. A close below this level will be an important bearish signal. We stay short on this pair.

Author

Growth Aces Research Team

Growth Aces

GrowthAces.com is an independent macroeconomic consultancy. They offer you daily forex analysis with forex signals for traders.