US stocks are on course for their best month since 1987

European stocks moved tentatively to the upside after a record-breaking session on Wall Street in the previous session. US stocks are on course for their best month since 1987 with the Dow Jones up over 13% so far. The mood in global markets has been lifted by a combination of three doses of very encouraging vaccine news, the US election finally being ‘settled’, and I think it’s worth noting the appointment of Janet Yellen to the US Treasury. She’s someone who, as Fed chair, repeatedly called on Treasury to do more and is viewed as a dove in relation to the deficit. Her first task won’t be made any easier after incumbent Steve Mnuchin moved to tied up $55bn in unspent Cares Act funding in a pot that will require Congressional approval to spend.

The Dow Jones industrial average smashed through 30,000 for the first time and in a sign of confidence in the move, closed above the level, too. Energy +5% and Financials +4% led the way as the rotation/reopening/reflation trade – whatever you want to call it – carried the day. The S&P 500 rallied 1.62% to 3,635, while small caps led tech. The Russell 2000 is now up 20% in November, its best ever month. President Trump called 30,000 for the Dow a ‘sacred number’.

Tesla shares rose another 6% to $555. I can’t put this down to anything other than a kind of mania akin to Bitcoin ‘HODLers’ who simply love the security too much to ever part with it and are ‘holding on for dear life’. On that front, Bitcoin eased back off the highs after breaking $19,000 yesterday, hitting an intra-day high at $19,495. Bloomberg will call an all-time high if it exceeds $19,511.

In early trade this morning the FTSE 100 rose to 6,466, just breaking above last week’s high at 6,463. Jun 8th highs at 6,511 are the next level up to be taken out for the bullish trend to continue. The FTSE is up over 13% this month alone, on course for its best monthly performance since 1989 but remains down over 14% YTD – if you think we get back to where things were before the pandemic at the end of 2019, there is plenty more upside to get to that level. Over in Europe, the ECB says it may lift the ban on bank dividends next year.

In FX, the dollar is offered with DXY dropping under the big 92 number and now faces key support at 91.70, the September low. Flows are indicating moves out of USD into EM, while the euro is also making progress with EURUSD at 3-month highs above 1.19. GBPUSD was steady around 1.3350, close to its recent highs. Relative silence over Brexit talks in the last couple of days is only raising expectations that there is a deal in the offing. Rishi Sunak to deliver his Spending Review later today. Spoiler alert: the public finances are awful and the Chancellor will prioritise protecting jobs. It’ll be a lot of green stuff, a lot of levelling up not down but he probably doesn’t think it’s time yet to turn the screw on investors with a hike to capital gains tax.

With the US Thanksgiving holiday tomorrow, we get a slew of data today from across the pond. US durable goods seen at +1% vs +1.9% last month, with the core reading expected at 0.5% vs 0.9% previously. Initial jobless claims seen at 732k, vs 742k last week. Continuing claims are see falling to 6m. Preliminary GDP figures for the third quarter (second reading) expected to be unchanged from the first reading at +33.1%. Core PCE index seen flat after +0.2% last time, with the personal spending down to +0.4% from +1.4% last month and personal income down to 0% from +0.9% previously.

Crude oil marched higher as the risk-on sentiment overcame doubts about demand over the winter. Whilst momentum is strong to the upside, near-term inventory builds still need to be watched. There is a risk that also that the recovery in prices is an overshoot when considering near term demand problems. The rally may also dissuade some OPEC members and allies from delaying the tapering of production cuts in the New Year. Technically, the 14-day RSI has reached overbought levels on WTI as it trades above $45, with Brent above $48.

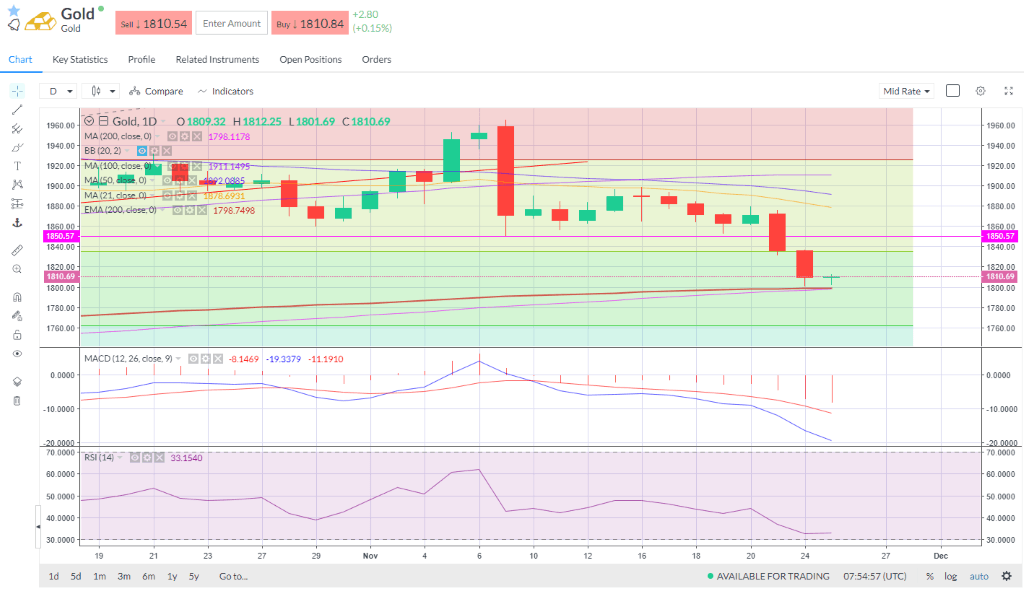

Gold slipped but found support at the 200-day moving average support on $1,800. What’s interesting is that the breakdown in gold has occurred even as real rates declined deeper into negative territory. Turning to Goldman Sachs for explanation: "We believe it is due to a combination of pro-cyclical rotation in equities combined with lack of increase in breakeven inflation expectations, which drove gold higher in late spring/summer. Therefore, gold suffered from strong rotation without reflation.”

Author

Neil Wilson

Markets.com

Neil is the chief market analyst for Markets.com, covering a broad range of topics across FX, equities and commodities. He joined in 2018 after two years working as senior market analyst for ETX Capital.