US S&P Global PMI Preview: A crucial report in a data-dependent era

- US S&P Global PMIs are expected to continue showing divergence between the Manufacturing and the Services sectors.

- Employment and input prices data will be closely monitored.

- A stronger-than-expected rebound in US PMI could boost the US Dollar.

- Eurozone PMI figures are also due on Friday.

The US economic performance is stronger compared to other economies like the Eurozone, as reflected in the PMIs (Purchasing Managers' Index). On Friday, new preliminary data for September is expected to show a modest improvement in both sectors in the US and the Eurozone. However, manufacturing activity is anticipated to remain in contraction territory on both sides of the Atlantic.

The fresh PMI figures will be closely watched as central banks are in a "data-dependent" mode following the Federal Reserve's decision to pause its interest rate hiking cycle. This dynamic is echoed by the European Central Bank (ECB), which made a dovish rate hike last week. The ECB hinted that interest rates would not be raised further, primarily due to a deterioration in the economic outlook. If the Eurozone PMI data comes in weaker than anticipated, it could strengthen the dovish stance of the ECB and potentially weigh on the Euro, reinforcing the divergence between the Eurozone and the US.

Looking at a modest recovery

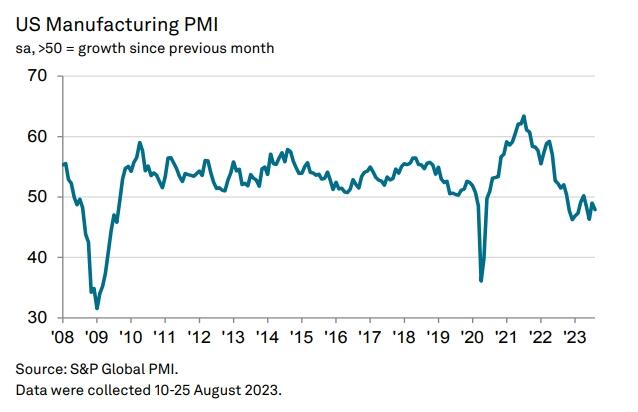

In August, the US S&P Global Manufacturing PMI fell to 47.9 from 49.0 in July, indicating a significant downturn. A marginal uptick to 48.0 is expected in September. The index has been in contraction territory (below 50) every month since November 2022, except for April. If the PMI increases sharply, it would signal that the sector could turn around. However, such a rebound is not expected at this time.

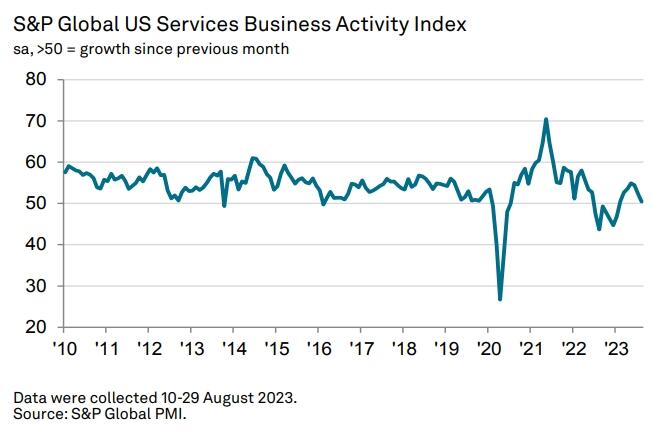

The contraction in the manufacturing sector has come together with a slowdown in the services sector. The Service PMI dropped sharply in August to 50.5 from 52.3, marking the lowest level in seven months. While it remains above 50, indicating expansion, the trend suggests increasing risks of stagflation. A marginal rebound to 50.6 is expected for September. If this reading falls below 50, it would raise comments about a "soft landing" scenario materializing. This could reduce expectations of higher interest rates for longer, potentially leading to lower US yields and putting pressure on the US Dollar.

Price indicators in the PMI survey will be worth monitoring. Signs of persistent price pressures would harm equities and likely be positive for the US Dollar. However, the final impact would depend on a combination of activity indicators, employment, price pressures, and a comparison with Eurozone PMIs.

In Europe, all PMIs are below 50, with Germany's numbers being particularly concerning. The German Services PMI stood at 44.6 in August, while the Manufacturing PMI came in at 39.1. For the broader Eurozone, the Services PMI was at 47.9, and the Manufacturing at 43.5. Market expectations are for a modest rebound, similar to the one anticipated in the US. However, if the readings come in worse than expected, it would further soften the odds of further tightening from the ECB and could weigh on the Euro.

After the Federal Reserve's hawkish pause, economic data will continue to be critical in shaping monetary policy expectations. The PMI data will provide an initial glimpse into activity during September, adding to the debate about the duration of high interest rates or the need for further rate hikes.

The US Dollar Index is on track to post its tenth consecutive weekly gain, marking a record streak. The strength of the US Dollar rally has been fueled by solid US economic data. The PMI data could add more fuel to the rally or slow it down, favoring a correction.

US Dollar Index Technical Outlook

The US Dollar Index (DXY) maintains a strong position above the 20-day Simple Moving Average (SMA), indicating a bullish bias. However, the 105.50 level poses a significant resistance barrier. If the Index remains below this area, a correction appears likely.

In the event of a retracement, as long as the US Dollar Index stays above 104.40, the Greenback will likely retain its strength. A break below 104.40 could trigger an extended correction, exposing the 104.00 level.

Positive data releases could provide the catalyst for the US Dollar Index to break above the 105.50 level firmly. Such a scenario could lead to an acceleration of the uptrend towards 106.00.

DXY daily Chart

-638308465569629865.png)

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Matías Salord

FXStreet

Matías started in financial markets in 2008, after graduating in Economics. He was trained in chart analysis and then became an educator. He also studied Journalism. He started writing analyses for specialized websites before joining FXStreet.