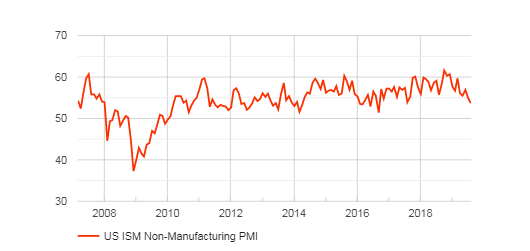

US Services Purchasing Managers’ Index Preview: The recessionary turn approaches

- Service PMI projected to climb slightly in August

- Index has been ebbing since October 2018’s post-recession high

- The US/China trade impact is rising

The Institute for Supply Management will release its non-manufacturing Purchasing Managers’ Index for August on Thursday September 5th at 14:00 GMT, 10:00 EDT.

Forecast

The Purchasing Manager’s Index is expected rise to 54.0 in August from 53.7 in July.

Business Sentiment and the US Economy

The retreat in optimism in the business community from last year’s euphoria, itself a compound of Trump administration policies, tax reduction stimulus spending and the logical if somewhat naive conviction that the trade war with China would find an easy solution, has not bought down the US economy.

FXStreet

Consumer spending backed by a labor market creating more positions than applicants has kept the unemployment rate near record levels and spread rising wages benefits into the far reaches of the job market. This is the economy that the Federal Reserve is keen to preserve with its rate cuts.

While the collapse in manufacturing sentiment and the retreat in the far larger service sector has not derailed GDP the collapse in business investment has shaved about a percentage point from growth.

From 4.1% annualized in the second quarter of 2018 to 3.1% in the third, and 2.1% in the final three months the decline has been steady if restrained. The unexpected jump to 3.1% in the first quarter of this year has not changed the trajectory and was followed by 2.0% in the second quarter and a running estimate for 1.5% in the third.

Consumption, Investment and Exports

The issue is not the overall health of the economy but the degree of spending backing GDP. The rate of domestic consumer expenditure over the past five months, an average 0.74% monthly increase in retail sales and 0.88% in the control group is commensurate with the current pace of economic growth, roughly 2.0%.

Consumers may fuel the bulk of US economic activity but they are not the whole. Business investment and exports are a large part of the balance. Because the US consumer has continued to spend, imports have remained relatively strong while exports, the opposite GDP accounting entry, have dropped sharply.

US Trade Balance

FXStreet

Conclusion

The service sector is the key component of US GDP. A strong labor market and healthy consumption go hand in hand, one reinforcing the expanding tendency of the other. Though the domestic market can provide a stable or growing base for the economy for a long period it cannot maintain itself for ever if the other sectors are in retreat and the global economy heads into decline.

The US economy and its dominant service sector are slowly approaching the crossroad where the global economy may turn toward recession. They will be hard pressed not to follow.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.