US September Nonfarm Payrolls: Taper expectations intact despite dismal job numbers

- US Payrolls add 194,000, less than half the 500,000 forecast.

- Unemployment rate falls to 4.8% as 200,000 leave labor force.

- Treasury yields rise, dollar is mixed, stocks flat.

The US economy created less than half the number of expected jobs in September. Firms seem unwilling or unable to hire workers despite a huge backlog of unfilled positions.

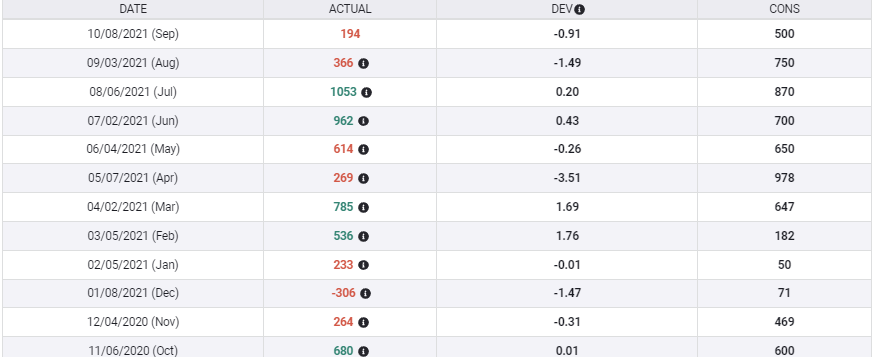

Nonfarm Payrolls added 194,000 jobs in September, less than half the 500,000 consensus forecast. The unemployment rate dropped to 4.8% from 5.2% in August, as almost 200,000 people stopped looking for work. August’s payrolls were revised to 366,000 from 235,000 and July’s numbers rose to 1.091 million from 1.053 million.

Nonfarm Payrolls

FXStreet

Job creation has slowed dramatically in the last two months. In June and July the economy hired or returned 2.053 million employees. In August and September that plummeted to barely one quarter at 560,000.

Private payrolls rose 317,000 in September and government employment at all levels shed 123,000 workers.

The second anemic NFP report in a row came as the participation rate slipped to 61.6%, its first drop in five months.

Weak hiring is an economic conundrum and may stem from lingering pandemic reluctance, indulgent jobless benefits and a lack of necessary skills, especially in the manufacturing sector. Almost 11 million unfilled jobs were listed in July by the Job Offerings and Labor Survey (JOLTS) and that number is unlikely to have fallen in August or September.

JOLTS

A more encompassing measure of unemployment that includes so-called discouraged workers, fell to 8.5% in September from 8.8%.

Wage increases continued to accelerate as employers used salaries to attract scarce and necessary workers. Average Hourly Earnings jumped 0.6% on the month and 4.6% on the year.

The leisure and hospitality sector added the most workers at 74,000, lowering its unemployment rate to 7.7% from 9.1%.

As these workers are among the lowest paid and wages still rose sharply, it underlines the inflationary pressure generated by the worker shortage.

Federal Reserve

The Federal Reserve has been preparing the markets for a reduction and end to its bond purchase program for several months. A good NFP report would have made a taper announcement at the November 3 Federal Open Market Committee (FOMC) a distinct possibility.

Fed Chair Jerome Powell noted after the September 22 meeting that a majority of members thought the “substantial further progress” criteria for a taper had been met.

September’s clear evidence that the labor market is slowing may have postponed the taper announcement until the December 22 meeting.

Market reaction

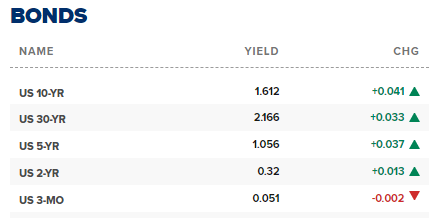

Initial reaction to the September NFP report was negative. Treasury yields and the dollar fell and equity futures rose. Those assessments were short-lived. Treasuries quickly reversed with the 2-year, 5-year 10-year and 30-year Treasuries all gaining in yield.

US Treasury yields

CNBC

The benchmark 10-year bond rose to 1.612%, its best finish since June 3.

US 10-year Treasury yield

CNBC

The dollar ended mixed against the majors.

The USD/JPY rose sharply closing above 112.00 for the first time since late April 2019.

The USD/CAD fell almost a figure to 1.2473, finishing below 1.2500 for the first time since July 29.

The loonie was aided by West Texas Intermediate (WTI) which finished at $79.08, its highest in seven years.

In the rest of the major pairs, the dollar lost negligible amounts.

Equites finished largely unchanged with the Dow shedding 869 points, 0.03% to 34,746.25 and the S&P 500 losing 8.42 points, 0.195 to 4, 391.34.

Conclusion

Despite the second consecutive dismal payroll report, markets still expect the Fed to announce and begin a bond taper this year.

Evidence that wage increases will be a stronger and more durable contributor to inflation may have added to that conviction. The Fed’s own recent admission that inflation will be higher and longer-lasting than originally anticipated, likely helped markets to keep the taper faith intact.

Treasury yields will set the pace for the dollar. If they continue to rise the greenback will follow.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.