Why the Bank of Japan might wait until the second half of 2026 to tighten again

The Bank of Japan aims to move its real rate closer to zero, but the timing and scale of future adjustments will depend on economic conditions. The market appears dissatisfied with the lack of clarity. With inflation expected to ease and USD/JPY strengthening toward 150, we view October as the most likely time for a rate hike. Recent data supports our outlook.

Tokyo inflation slowdown may prompt the BoJ to be cautious about raising rates

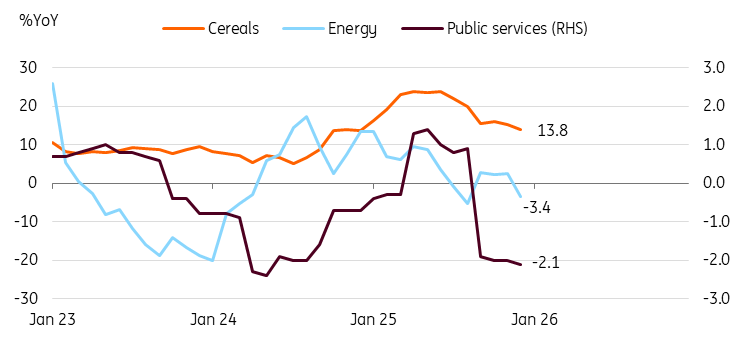

Headline Japanese inflation eased to 2.0% year on year in December, below expectations (vs 2.7% in November, 2.3% market consensus), mainly due to renewed energy subsidies, stable rice prices, and low petroleum costs. These factors are expected to keep inflation low into 2026, as the government increases winter energy subsidies, oil prices remain weak, and rice prices continue to fall. Thus, headline inflation is expected to drop below 2% in the coming months.

Meanwhile, core inflation, excluding fresh food and energy prices, slowed to 2.6% (vs 2.8% in November, market consensus). Goods prices declined while private services and housing prices showed steady gains in December. Going forward, we expect core inflation to decelerate toward 2%, mainly due to base effects.

With headline inflation expected to drop below 2.0%, and core inflation easing toward 2.0%, the BoJ is likely to carefully assess the impact of previous rate hikes before considering any further hikes. Once the BoJ confirms that core inflation will remain above 2% and outpace headline inflation, it will likely take the next step sometime in the second half of 2026. We believe that strong wage growth and government aid will keep core inflation above 2%. Notably, major labour unions have detailed plans to pursue wage growth of over 5%. Strong corporate earnings are likely to allow for solid wage growth. Also, the government's shopping voucher and cash payout programmes are expected to stimulate private consumption.

We expect USD/JPY to appreciate modestly in the first half of 2026 as interest rate differentials between the US and Japan narrow. Yet if market concerns shift toward fiscal health -- unlike our base-case scenario -- and increased direct investment in the US further weakens the JPY, the timing of the BoJ hike could move forward to the second quarter.

Rice, energy, and public services will lower headline inflation in 2026

Manufacturing activity declined in November, but this is likely temporary

Production and shipments fell in November, likely pausing temporarily following previous solid gains. Industrial production declined a more than expected 2.6% month on month, seasonally adjusted, in November (vs 1.5% in October, -2.0% market consensus). This only partially offset the previous two-month gain. The most significant drop was in auto production, which fell 7.2%, the first decline in four months. Meanwhile, retail sales rose 0.6% MoM in December, marking the third consecutive month of growth. Major categories such as general merchandise, apparel, and food and beverages all gained ground. Auto sales were weak, down 2.6%, but we believe this is a temporary decline following a sharp 9.6% gain in October.

We expect GDP to rebound 1.6% quarter-on-quarter, annualised, in the fourth quarter, after a 2.3% contraction in the third quarter, led by private consumption and investment. We are concerned that the sharp decline in Chinese tourists may lead to a deterioration in retail sales in December. So far, the negative impact has been quite limited. Also, winter bonuses are expected to increase sharply, boosting overall consumption. Equipment investment is expected to recover mostly in transportation and semiconductors; construction investment should rebound as safety measures related to one-off factors dissipate.

The BoJ meeting minutes showed the board adopted a more hawkish stance

According to the BoJ’s summary of opinions from its December meeting, some board members noted that the real interest rate remains very low and that the central bank needs to adjust the degree of monetary accommodation. One member even argued that the BoJ should adjust policy with intervals of a few months. We believe the board's overall stance has shifted toward a more hawkish position, but the pace will remain slow. We expect most board members to take a cautious approach to the next hikes. Our expectation remains that a 25bp hike will most likely happen in October; the BoJ may raise the rate as high as 1.50% by the end of 2027.

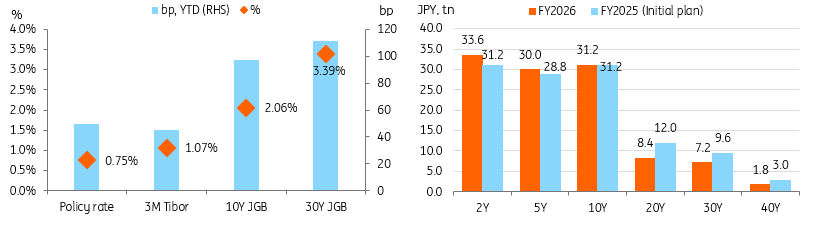

JPY and JGB weakened in December

USD/JPY ended 2025 at 156.63, gaining by 0.4% against the USD. However, the December move declined by 0.7%. Despite the rate hike on 19 December, the JPY fell to a one-month low of 157.77 per dollar, which led FX authorities to issue warnings about potential intervention. The combination of these warnings and the hawkish tone reflected in the BoJ’s meeting minutes helped stem the JPY's softening. We expect JPY to remain range-bound in the near term. Upside is limited by intervention risk, while the USD trend depends on upcoming data. Gradual Federal Reserve rate cuts in the first half of 2026 may strengthen JPY toward 150.

Short-term Japanese government bond (JGB) yields climbed steadily in December, following the policy rate rise. Looking ahead to 2026, we expect JGB yields to continue rising as the BoJ gradually raises rates. There is a greater potential for short-end yields to rise further, especially with increased issuance of short-term JGBs. The government’s plan will decrease sales of super-long JGBs while growing issuance for 2-year and 5-year bonds.

Short-end JGB yields are expected to rise more rapidly in 2026

2026 outlook

Entering 2026, the Japanese economy encounters both challenges and opportunities. Growth is expected to accelerate thanks to expansionary fiscal measures, steady global IT demand, and soft global energy prices. Strong corporate earnings will boost wage growth and investment. Nevertheless, the financial market could remain unstable amid concerns about long-term fiscal health and rising debt-service burdens, which could impact economic performance. Thus, we expect the BoJ's rate hikes to be quite gradual. A further fiscal push could backfire on the economy, but the current government is expected to maintain its expansionary policy stance, posing a significant risk to the economy in 2026.

Read the original analysis: Why the Bank of Japan might wait until the second half of 2026 to tighten again

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.