US September Durable Goods Orders Preview: Business spending continues to restrain durable goods

- Durable goods orders forecast to fall after modest rise in August.

- Business investment to drop for the second straight month.

- Non-defense orders to climb sharply for the third month out of four.

The US Census Bureau will issue its Manufacturers New Orders for Durable Goods for September on Thursday October 24th at 12:30 GMT, 8:30 EDT.

Forecast

Durable goods orders are expected to decrease 0.8% in September following August’s 0.2% gain. Orders ex transport are projected to decline 0.2% after rising 0.5% in August. Non-defense capital goods ex aircraft and parts, a proxy for business investment, are forecast to fall 0.2% after August's revised 0.4% loss, initially -0.2%. Orders outside of defense appropriation will increase 1.9% in September after the prior month’s 0.6% decrease.

Durable goods

Durable goods are the long-lived denizens of the retail world. Its products are intended to last three years or more in normal use. They vary from consumer purchases like lawn chairs, circular saws and espresso machines to business investments like earth-moving machinery and commercial aircraft and government procurement like tanks and helicopter gunships. The longer longevity implies a somewhat different economic analysis especially for business which wants to be sure that the purchase cost will be justified by use.

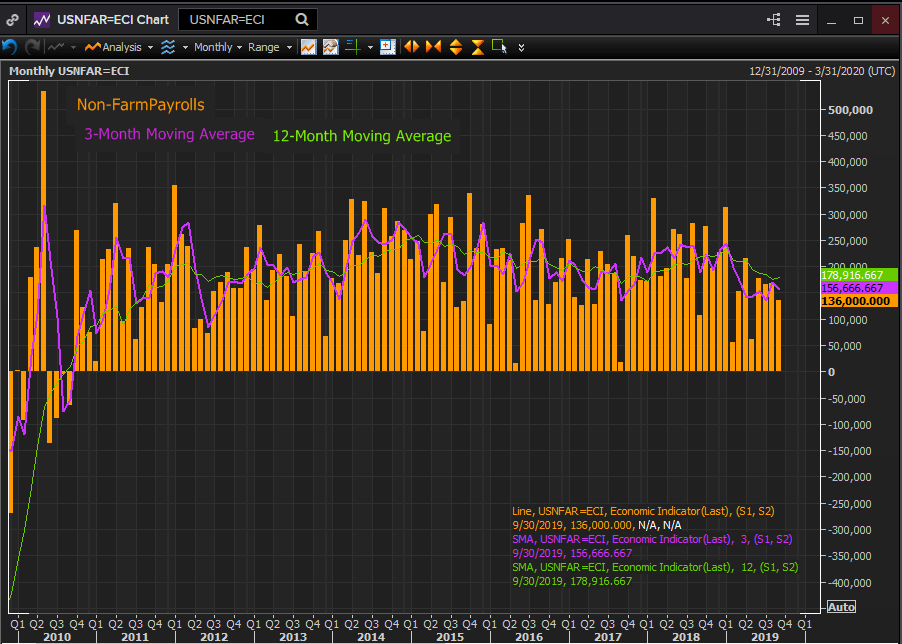

Retail Sales and the labor market

Consumer spending slowed in September after six strong months, though the unexpected drop was mitigated by positive revisions to some of the August results.

Overall sales slipped 0.3%, missing the 0.3% forecast, while the August totals were adjusted up to 0.6% from 0.4%. Retails sales ex-automobiles fell 0.1%, below the 0.2% expectation though August’s final figure was revised to 0.2% from flat. The control group, the business spending analog, was flat on a 0.3% prediction and unchanged for August at 0.3%.

The half-year to July was the best for overall retail sales in 16 years. Household spending has been buoyed by robust rates of job creation and rising wages.

Payrolls averaged 157,000 in the three months through September and 179,000 for the year. The 3.5% general unemployment rate was the best in five decades and the rates for African-Americans and Hispanics were at all-time lows. Though the annual wage gain slipped to 2.9%, that was the first month below 3% in more than a year, the best stretch in a decade. Rising rates of consumption are the natural corollary to economic success.

Reuters

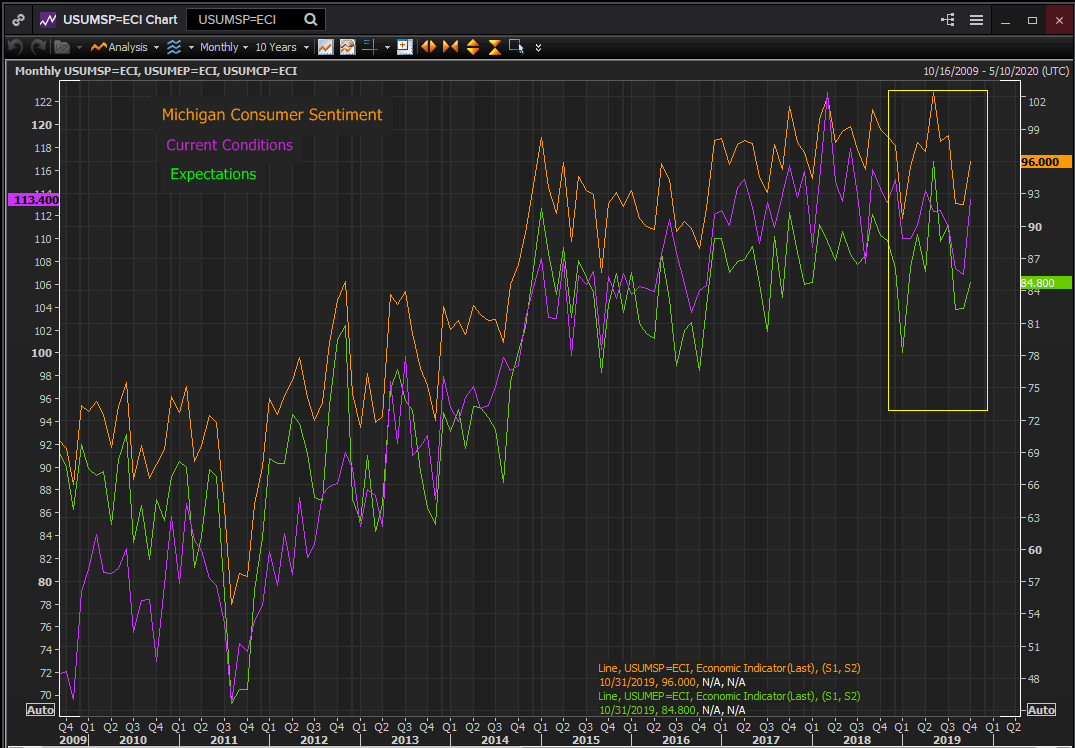

Michigan Consumer Sentiment

After two years of the most positive consumer outlook in decades sentiment declined sharply in January of this year with the partial government shutdown which ended late that month. Americans have a well-documented dislike for political machinations in Washington that affect the delivery of government services. Sentiment had recovered by May to a post-recession high only to fall again in August and September.

Reuters

The drop in September’s overall sentiment was largely driven by a steep fall in the expectations index, which had declined more than twice as much as its twin the current conditions index, this year.

October’s recovery in the Michigan Sentiment Index brought it back to near the mid-point of the last three years and was sponsored by a large climb in the current conditions index.

Americans' concerns appeared to be centered on the sustainability of the current economic good times. The unusual length of the expansion, the bitterness of endless political conflict in Washington, the unsettled China trade war even Brexit and the concerns exemplified by two Federal Reserve rate cuts all likely play a part.

The labor market boom has extended work and prosperity to communities much damaged by the transfer of jobs overseas by the economic policies of the past 20 years. A little disquiet about their good fortune is probably natural.

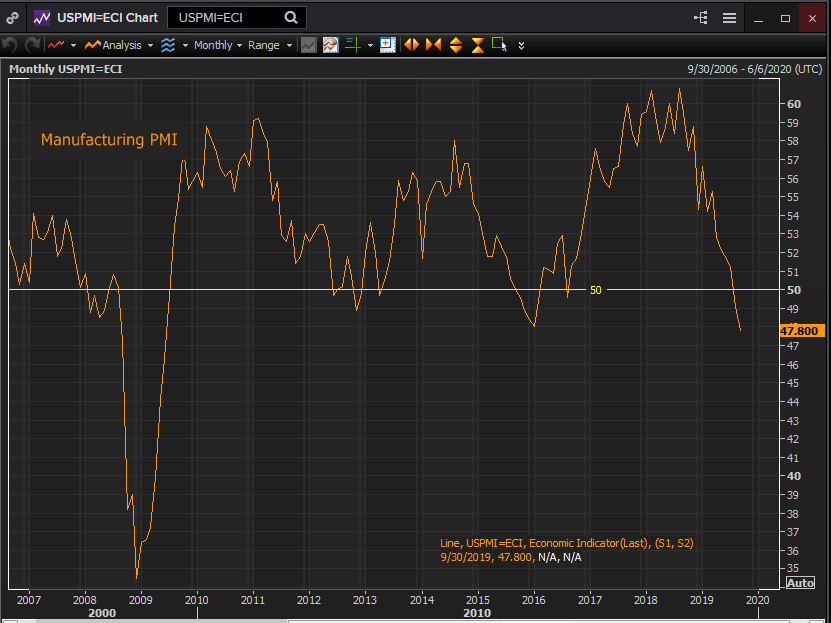

Business spending and sentiment

The trade war with China has been a large and increasing drag on business sentiment and spending for more than a year. That is especially true of the manufacturing sector where the purchasing managers’ index registered contraction in August and September.

Reuters

President Trump and Liu He, the Chinese trade negotiator announced a tentative agreement on October 13th. Mr. Trump said he expected to sign the completed deal with President Xi Jinping next month and talks would continue until extant issues are settled.

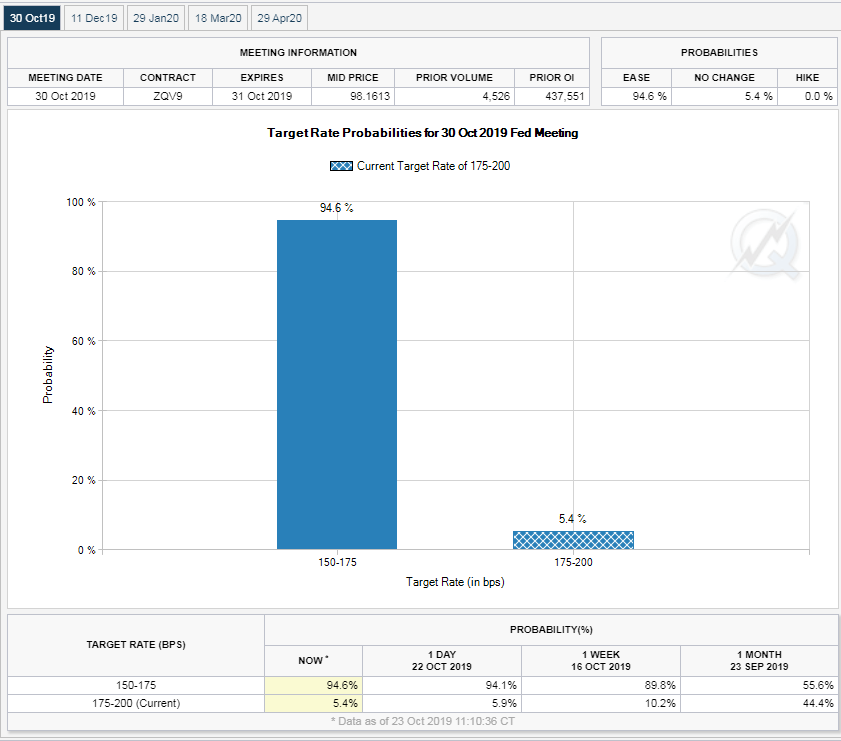

Federal Reserve and the dollar

Durable goods orders will have minimal impact on the pending Fed rate cut on the 30th, currently estimated at 94.6% in the futures market. Even an exceptionally strong number, suggesting a much more robust economy ahead would not on its own sway the FOMC.

CME Group

The dollar’s recent mild weakness has been a function of the decline in global risk aversion as the two chief sources, the China US trade war and the UK exit from the European Union, have made steps toward settlement.

Of more importance to the dollar will be the statements of Chairman Jerome Powell on the future course of policy.

Conclusion

Consumers have been the backbone of the current expansion. The recovery in outlook this month is a sign that the reality of labor and wages will remain the dominant factor in household spending decisions.

Business spending has been largely frozen by the China trade dispute and it is too soon for this month’s initial agreement to have had an impact. Any substantial change in business attitudes will wait until the formal deal is signed and if that takes place in November, new investment will be delayed until the New Year.

The consumer side of durable goods is likely to perform better than expected in September, business not so much.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.