US Retail Sales Preview: The question of December

- January sales expected to return to trend

- December revisions key market focus

- Private sector records show good holiday sales

The US Census Bureau will issue its retail sales report for January on Monday March 11th at 8:30 am EST, 13:30 GMT.

Forecast

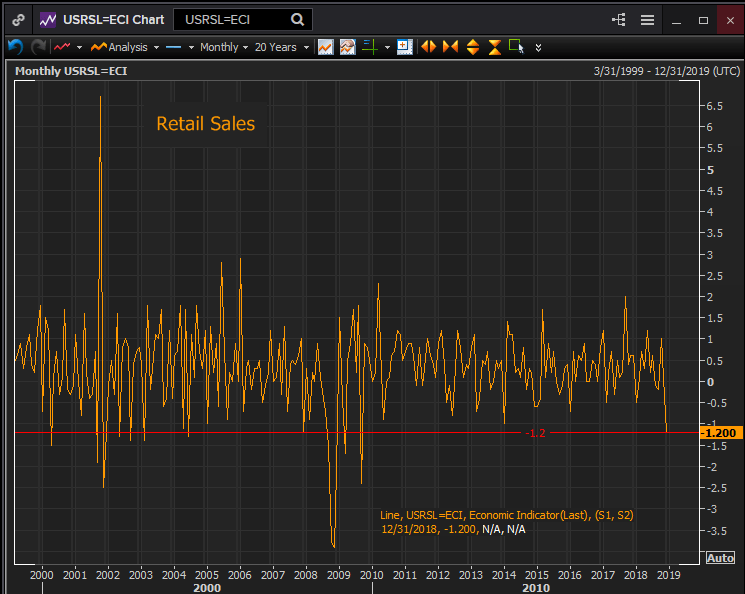

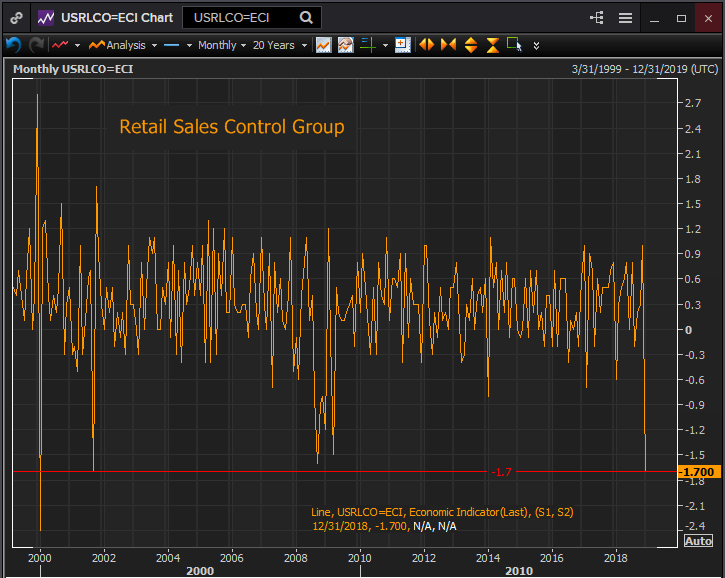

Retail sales are predicted to increase to 0.1% in January following December’s large but likely incomplete drop of 1.2%. Sales without automobiles are expected to rise 0.3% after the 1.8% plunge in December. The control group which is used by the Bureau of Economic Analysis to calculate GDP and excludes building material, motor vehicles gasoline station and foods service receipts, is expected to gain 0.6%. It fell 1.7% in December.

December Revisions: Revived optimism

Revisions to prior months’ statistics are normally a minor affair. This release is different. December is biggest month of the year for American retailers, many depend on holiday sales for much of their annual profit. As we noted in our preview for US fourth quarter GDP on February 27th .

“The month long partial government shutdown in late December and January may have had an uncertain effect on the US economic activity but it had a decided effect on the reporting of that growth. The most important impact seems to have been on the retail sales numbers from the US Census Bureau a division of the Commerce Department.”

Expectations before the delayed December retail sales release on February 14th were for a continuation of the healthy expansion rates from October and November. Overall sales were expected to rise 0.2% in December following the prior gains of 1.0% and 0.1%. Sales excluding autos were forecast to rise 0.1% after October’s 0.8% increase and November’s flat result. The control group, the Bureau of Economic Analysis’ category for consumer spending, that is sales excluding building materials, motor vehicles and parts, and gasoline station and food service receipts, was predicted to increase 0.4% after October’s 0.3% and November's 1.0% gains.

There were good indications from the private sector that the December holiday shopping season had been a success.

Amazon the world’s largest on-line retail business had reported record sales for the season. The Redbook Index which tracks weekly proceeds from stores representing 80% of the Commerce Department’s retail base tabulated a 6% rise each week in December in same store sales. The 9.3% increase of annual sales in the last week of the month was the largest in its history. MasterCard said it had a 5.1% increase in card purchases over 2017.

In the statement accompanying the release the Commerce Department included the anodyne note, "data collection and processing were delayed" leaving the interpretation as to how this might have affected the numbers entirely to the reader.

The retail sales numbers as issued were far below expectations and in complete contradiction to the figures from private sources.

Headline sales came in at -1.2%, 0.2% forecast. Sales ex-autos were -1.8%, forecast 0.1%. The control group was -1.7% with a predictions of 0.4%.

Reuters

To give a sense of how far out of line the Census numbers were the headline drop of 1.2% was the worst single month since sales fell 2.4% in September 2009. Sales-ex autos at -1.8% saw their worst month since December 2008, -2.6% at the height of the financial crisis. The control group number -1.7% was the largest one month fall since September 2001, worse even than September 2008, -1.6%, and March 2009 -1.5%.

Reuters

The disconnect between the private sector accounts of the Christmas season and the Census figures was noted by many commentators. One final note, Amazon’s report of record sales directly denys the government statistic that non-store sales fell nearly 3.9% in the month.

If the December figures from Census are accurate then it will be surprising if the January numbers return to trend. We will have to formulate a new theory as to why retail sales would collapse in the midst of a jobs boom. If the numbers are incorrect the view ahead for the US economy is considerably brighter.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)