US Retail Sales Preview: Let the spending begin

- Retail sales set to resume expansion in March

- Consumer spending was unexpectedly weak in February

- Recent sales volatility may be result of reporting issues around the government shutdown in January

The US Census Bureau will release its retail sales report for March on Thursday April 18th at 8:30 am EDT, 12:30 pm GMT

Forecast

Overall retail sales are predicted to rise 0.9% in March following February's 0.2% decline. Sales excluding automobiles are expected to climb 0.7% after falling 0.4% the prior month. The 'control group' sales minus building materials, motor vehicles and parts, and gasoline stations and food service receipts, is predicted to rise 0.4% in March after February's 0.2% decrease.

Retail Sales: Volatility and then some

The recent gyrations in the retail sales figures were a product of reporting lapses around the now forgotten government shutdown. The closure lasted most of January when the December retail numbers were to be forwarded to the Census Bureau statisticians. The 1.6% plunge in December’s overall retail sales and the three month 4.9% round trip from 1.0% in October 2018 to -1.6% in December and back to 0.7% in January were the largest variations in the sales statistics since the financial crisis and recession of 2008-2009.

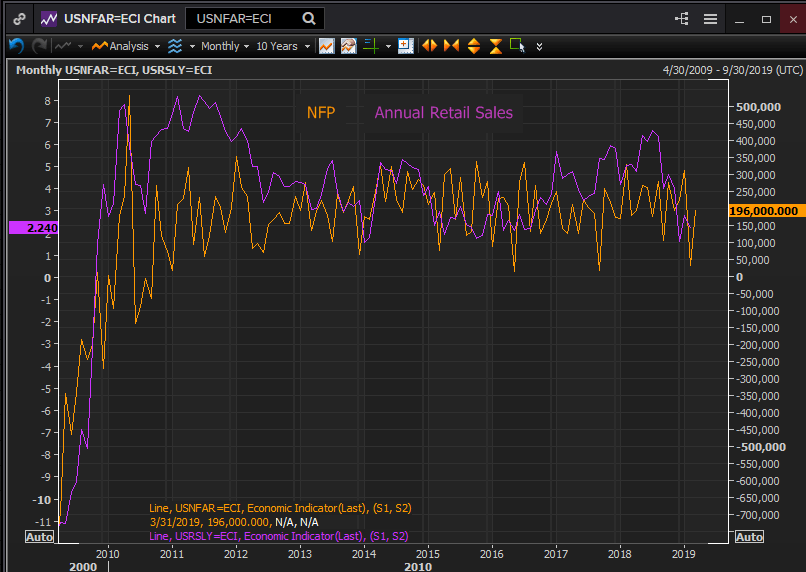

Retail Sales and the Labor Market

The steady production of new employment and the gains in average hourly earnings over the past two years have given households more confidence in their economic future and helped bring the annual change in retail sales from 2.2% in August 2016 to 6.62% in July 2018. The decline to 4.03% by last November brought sales to the low side of its two year range but the subsequent plunge to 1.64% in December 2018 and the minimal recovery to 2.24% by March is most likely a residue from the accounting problems surrounding the January government shutdown.

Reuters

Reuters

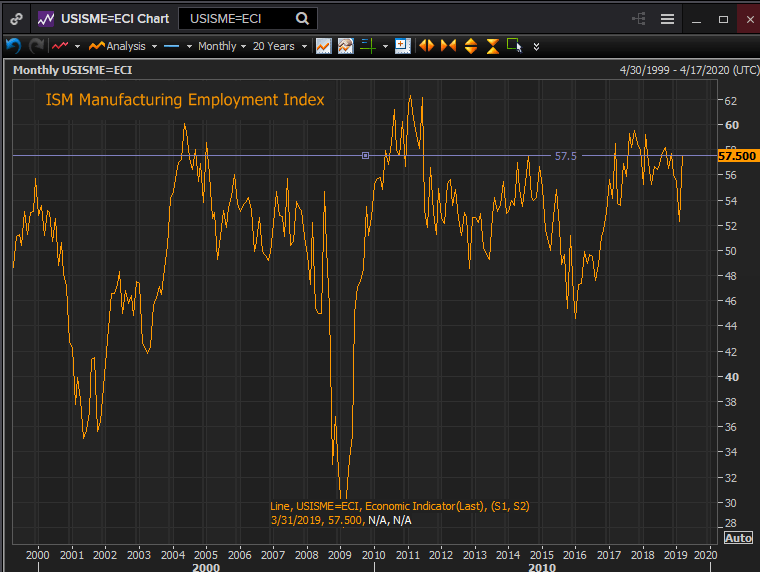

Employment indexes from the Institute for Supply Management show moderated levels of new hiring but the moderation is in relation to the very high levels of optimism evinced by businesses in 2017 and 2018. The ISM manufacturing employment index last month was 57.5, in the upper range of the last two years but above every score for the six years prior to March 2017.

Reuters

The ISM services employment index for March at 55.9 is in the lower reaches of its two year range but it is securely on the expansion map.

Consumer Sentiment

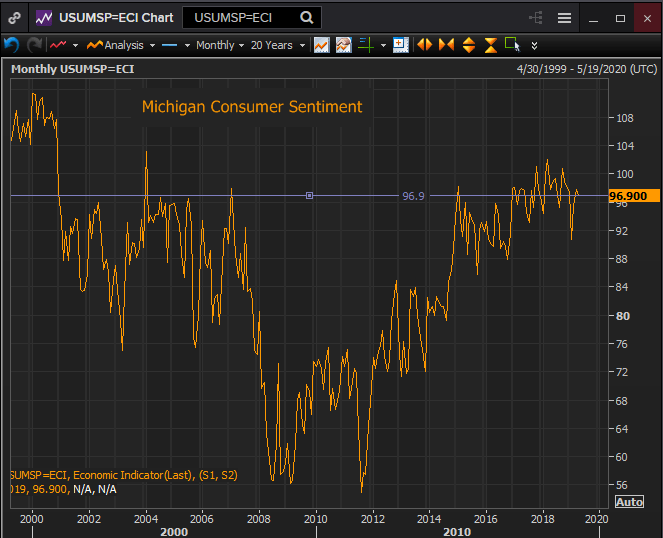

Optimism among American households has also recovered smartly from its drop in December and January. The Michigan Consumer sentiment survey slipped slightly in March to 96.9. That leaves it about mid-way through the excellent scores of the last two years. The current conditions and expectations indexes exhibit a similar return to a sanguine outlook.

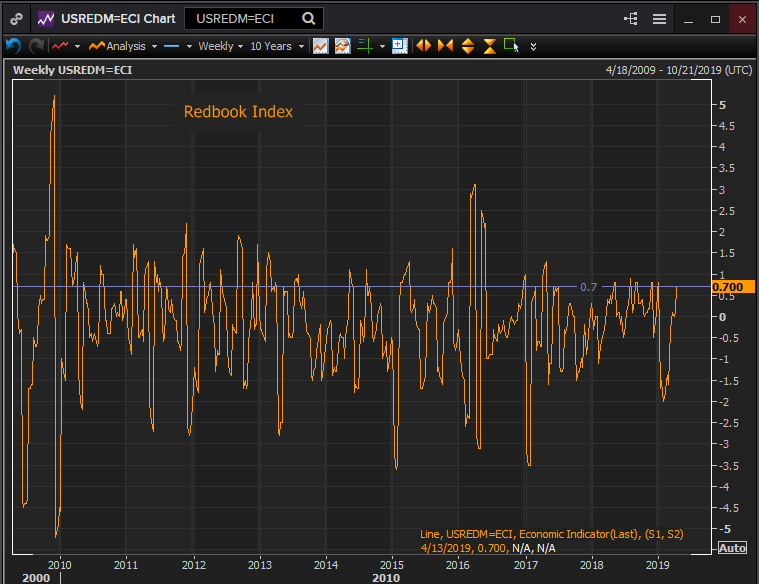

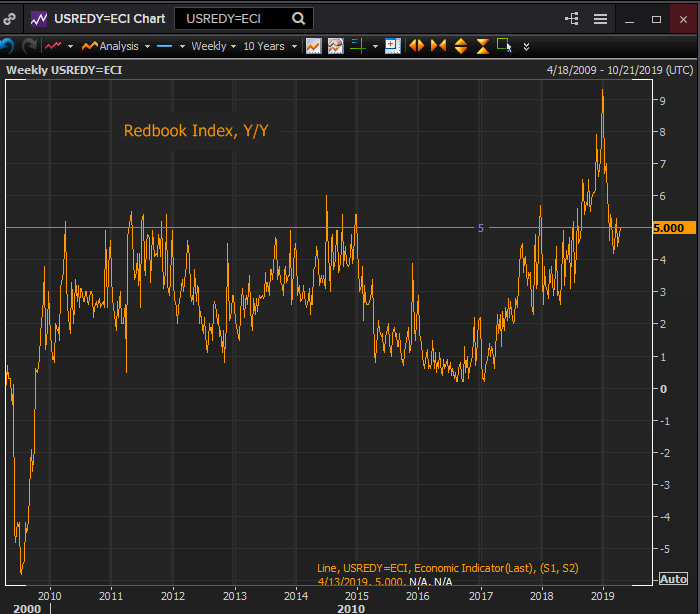

Redbook Index

The Redbook Index which tracks growth in retail sales based on the purchase data of about 9,000 large general merchandise outlets representing over 80% of the government’s retail sales figures, was up 0.7% in the week ending April 8th, a rapid return to normal levels after the steep January fall.

Reuters

Conclusion

All indicators point to a substantial improvement in the March retail sales numbers over February.

The labor market remains strong with non-farm payrolls resuming job creation at 196,000 in March after the February plummet to 33,000. Initial jobless claims are at 50 year lows. Wages continue to improve. Annual average hourly earnings stood at 3.2% in March within 0.2% of its decade high.

Consumer and business optimism are strong if not quite as ebullient as last summer.

Lastly the Redbook Index, a near equivalent to the Census Bureau’s official sales figures, gained an entirely normal amount in March with the annual reading of 5% above almost all of the readings for the past ten years. All in all the US consumer has every reason to be feeling expansive.

Reuters

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.