US Retail Sales February Preview: Will the real consumer please stand up?

- Did January Retail Sales soar 5.3% on stimulus payments?

- Control Group jumped 6%, the most since the lockdown reverse in May and June.

- Nonfarm Payrolls more than doubled from January to February.

- Dollar and interest rates trading higher on good US data.

Did Americans sense the job market was heating up in January despite the dismal initial figures from the government of just 49,000 new hires? Is that a better explanation of the huge 5.3% jump in Retail Sales and 6% gain in the Control Group than the $600 pandemic stipend awarded in December?

The sales performance was not a minor anomaly. Except for the lockdown recovery months of May (18.3%) and June (8.6%), the January burst of spending was the second highest one month gain in a generation. Only the 6.7% increase in October 2001, as the US was emerging from a short recession, was greater.

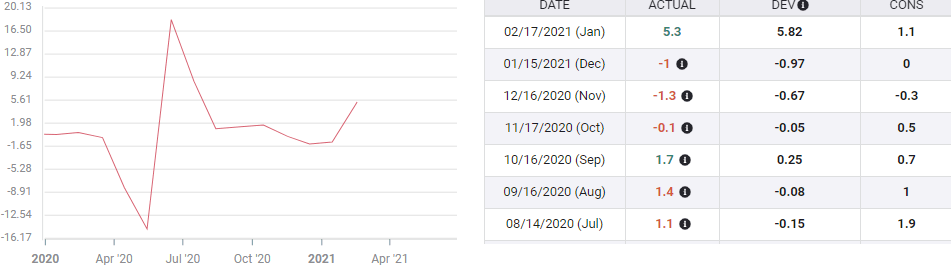

Retail Sales are forecast to fall 0.5% in February from 5.3%. Control Group Sales are expected to drop 1.1% from 6% and Sales ex Autos are predicted to slip 0.1% from 5.9%. These declines are predicated on the supposition that it was the relatively minor stimulus payment that arrived for people in December that funded the January sales rocket. With no stimulus payments in February analysts think US consumers will stay home.

Nonfarm Payrolls

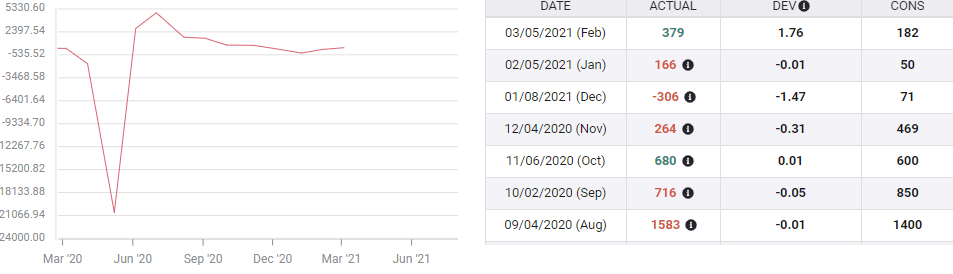

The loss of 306,000 positions in December was a direct result of the re-instituted strict lockdown in California, the nation's largest economy, and applied restrictions in several other states.

Even though California rescinded its closure in late January national payrolls were expected to add only 50,000 workers when the month's figures were released on February 5. The initial issue from the Bureau of Labor Statistics (BLS) was right on target at 49,000.

For the February payrolls, reported on March 5, only 182,000 new hires were forecast. Job creation was actually twice as strong at 379,000 and the revision to January more than tripled the original at 166,000.

Over the two months the forecast for 232,000 new employees did not even replace the December loss of 306,000. In reality, 545,000 people returned to work. American firms produced more than twice as many jobs (240%) in January and February as analysts expected.

Retail Sales

Expectations for consumer spending in January were also woefully under charted. Overall Sales were forecast to rise 1.1%, they soared 5.3%; Sales ex autos were expected to gain 1%, they jumped 5.9% and the Control Group which mimics the consumption component of GDP, climbed 6% on an 0.8% estimate.

Retail Sales

Conclusion

It is a reasonable assumption, given the size of the sales gains and the relatively small stimulus check, that the consumer confidence exhibited in January was prompted by something more than a one-time payment.

By the end of the month it was clear that the pandemic was ending, that the job market as experienced by consumers was far stronger than predicted and that both would continue to improve in February. Add another $1400 in free money and the psychological relief at the retreat of the pandemic and there is a good chance that the spending effusion of January will continue into February.

The dollar and US interest rates have been attentive to the improving US economy. If analysts have again underestimated the US consumer, we can be sure traders will not.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.