US October Manufacturing PMI Preview: Waiting for the China deal

- Modest rebound in sentiment forecast but index will remain in contraction.

- The unsigned phase one trade deal with China has had little positive effect as yet.

- Export orders in September were the weakest since the recession.

The Institute for Supply Management (ISM) will issue its purchasing managers’ index (PMI) for the manufacturing sector in October on Friday November 1st at 14:00 GMT, 10:00 EDT.

Forecast

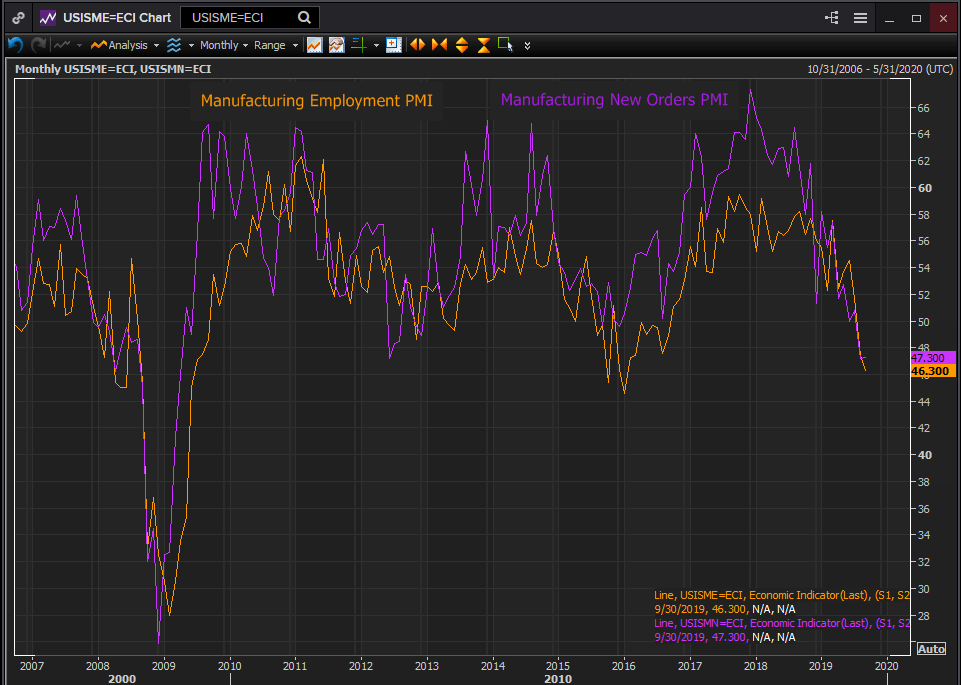

The purchasing managers’ index is expected to rise to 48.9 in October from 47.8 in September and 49.1 in August. The prices paid index is projected to increase to 49.9 from 49.7. The new orders index was 47.3 in September and 47.2 in August. The employment index registered 46.3 in September and 47.4 in August.

ISM Manufacturing Report on Business

The ISM survey is based on the responses of “a group made up of more than 300 purchasing and supply executives from across the country.” These professionals respond anonymously to a “monthly questionnaire about changes in production, new orders, new export orders, imports, employment, inventories, prices, lead times, and the timeliness of supplier deliveries in their companies comparing the current month to the previous month.” The answers are tabulated into an index and rated on a scale that places the division between expansion and contraction at 50 with the first above and the latter below. *Quotations from the Institute for Supply Management website.

US China trade and manufacturing

The US trade dispute with China turned a buoyant manufacturing recovery in 2017 and 2018 into an incipient recession this year. The initial optimism that the two sides would find a deal has faded into a long drawn acrimonious confrontation. After two years of argument and escalating tariffs the October deal, as yet unsigned, will need many months of performance by both sides before it begins to lift the pessimism in the manufacturing sector.

Over the past year sentiment in manufacturing has had the steepest decline since the recession and financial crisis. From 60.8 in August 2018, a 15 year high, the purchasing managers’ index dropped into economic contraction in August with 49.1 and 47.8 in September.

Indexes for employment and new orders have fallen in line with the sentiment index. Employment has gone from 58.2 last September to 46.3 a year later. New orders have fallen from 61.8 last November to 47.3 in September.

Reuters

The new export orders index registered 41 in September down from 43.3 in August. It was the third month in contraction and the lowest reading since March 2009.

“Global trade remains the most significant issue, as demonstrated by the contraction in new export orders that began in July 2019,” noted Timothy R. Fiore the Chair of the ISM Business Survey Committee in the September release.

Manufacturing and the US consumer

Consumer demand has remained healthy in the United States. The retail sales control group which informs the government’s GDP calculation averaged a 0.4% monthly increase in the year to September.

Reuters

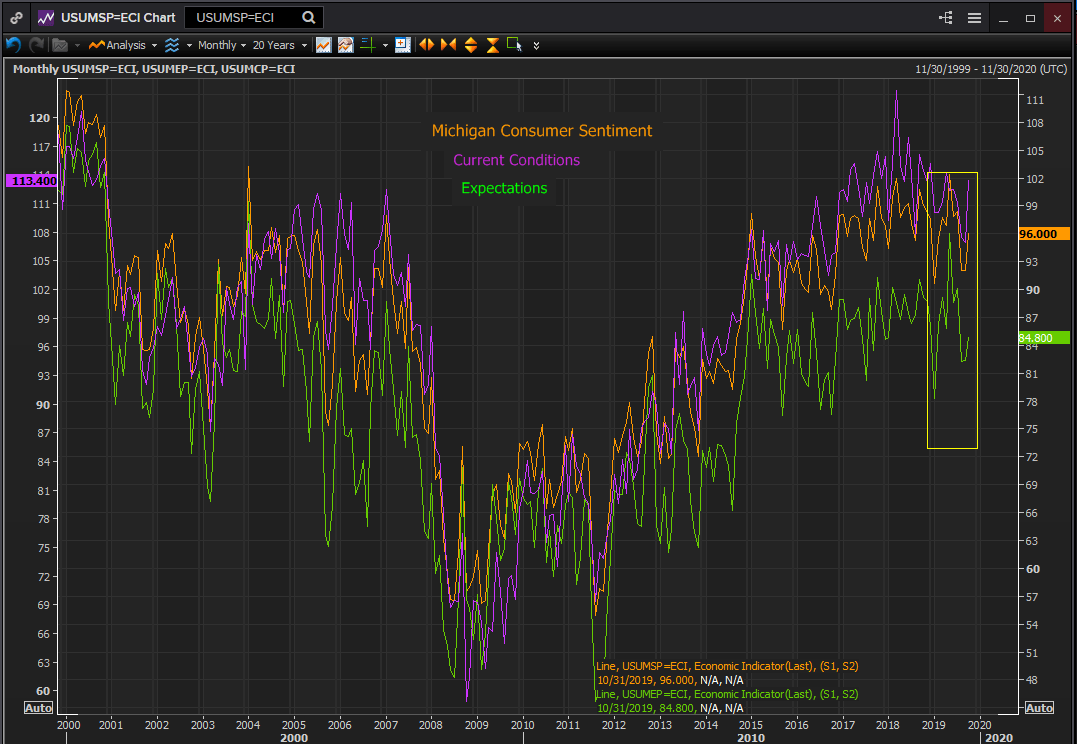

Consumer sentiment has also retained a positive cast though it has lost some of its record elevation of last year.

The Michigan Consumer Sentiment Index recovered to 96 in October from 92 in September. This puts it in the middle of the range of the last two years which have seen the highest sustained reading in two decades.

Reuters

Conclusion

American manufacturers are saddled with a trade war with China that has drastically reduced their own business from overseas and threatened to depress already weak global economic growth.

Domestic orders to US factories have not been the problem as US demand has remained strong. It has been the large reduction in overseas purchases of US manufactured goods, both from China due to tariffs and the balance of the world owing to slowing growth, that has pushed the factory sector into contraction.

The US China trade war has had a two-fold effect. It has directly curtailed US sales to the mainland of manufactured products and agricultural commodities. But its impact on outlook and sentiment and the fear of a generalized global trade contraction has caused a pullback in business investment and spending worldwide.

The October agreement between the US and China may be the first step in improving the global economic picture but it is too early to tell. Even if the agreement is signed as planned in November the trust abrogated over the last two years will take time to restore, and returning to prior levels of trade will take even longer and likely several additional agreements.

If the trade deal can restore optimism to the global scene US manufacturers will recover their own in short order but that will not happen in October or probably this year.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.