US Non-Farm Payrolls Preview: Against all odds

- August payrolls predicted to be at trend

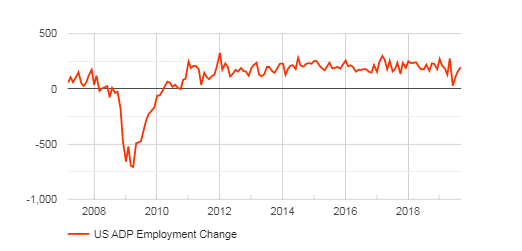

- ADP hires were better than expected at 195,000,

- Unemployment rate should continue near historic lows, wages steady

The Bureau of Labor Statistics (BLS) a division of the US Department of Labor will issue its Employment Situation Report for August on Friday September 6th at 12:30 GMT, 8:30 EDT.

Forecast

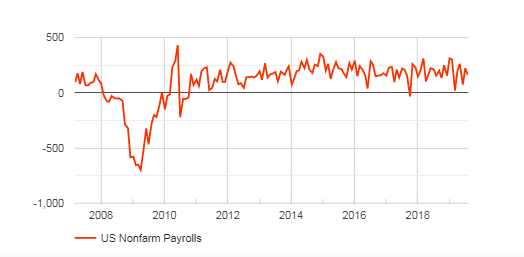

Non-farm payrolls are expected add 158,000 new workers in August after May’s gain of 164,000. The unemployment rate is predicted to be unchanged at 3.7%. Average hourly earnings will rise 0.3% on the month as in July and the annual increase will fall 0.1% to 3.1%. Average weekly hours are projected to climb to 34.4 from 34.3.

The Employment Situation Report background

Commonly called non-farm payrolls, payrolls or just NFP, the US Labor Department’s monthly assessment of employment is the most widely noted and actively traded set of American economic statistics.

The report is formulated on two surveys. The establishment poll queries non-farm businesses and compiles the payrolls numbers, wages, weekly hours, labor force participation rate and other measures.

The household survey contacts a representative segment of the working age non-military population and asks if each person is employed or unemployed and if and when they last looked for a job. The answers are used to calculate the unemployment rates.

The U-3 unemployment rate is the measure normally quoted in analysis. Unemployment here is restricted to non-working individuals who have looked for a job in the month prior to the survey. A person who is not employed or unemployed under the U-3 definition is not part of the official workforce.

FXStreet

The U-6 or under-employment rate is a wider gauge and includes anyone who has searched for work in the prior year. Many analysts consider it a better measure of actual unemployment.

The non-farm payrolls figure includes a BLS estimate for the number of jobs created at start-up firms, generated by the so called birth-death model, that have not yet been reported to the government. The number of these jobs is revised at a later date against company and government information.

The NFP report is one of the most current of the government’s statistical efforts as its data is about one month old.

Non-Farm Payrolls, unemployment and wages

The job figures of June and July, 164,000 and 224,000, have quieted fears that the labor market was beginning to sag from the combined weight of the China trade dispute, Brexit and the global economic slowdown. Two months in the past six, February at 20,000 and May at 75,000, were far below average and though volatility is common, two oddities in a short space is unusual and could have signaled a change in trend.

In fact job creation has retreated this year. The three-month moving average has dropped from 257,000 in January to 154,000 in July. If the August consensus estimate of 158,000 is accurate the average will only rise to 182,000, still a good number but 75,000 less than January.

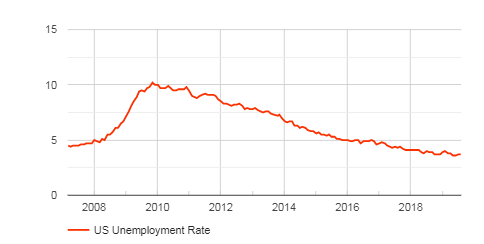

In past economic eras an unemployment rate below 4% for six months and for 12 of the last 13 would be considered full employment and a herald for incipient wage inflation. The unemployment rate has not been this low for this long since the late1960s, over 50 years ago.

Wage gains took almost a decade to recover from the financial crisis and recession. The huge overhang of unemployment meant that for almost ten years employers did not have to offer incentives to hire. Since breaking above 3.0% last October at 3.1% annual wages increases have remained steady. When combined with low inflation these gains have given consumers the best additions to purchasing power since the recession and helped to keep the US economy expanding.

FXStreet

Coincident labor market statistics

Two secondary US statistics are are often used as precursors to the labor market portrayal in the payrolls report: ADP payrolls and initial jobless claims.

NFP and ADP

The private payroll list from Automatic Data Processing (ADP) has the most direct correlation to NFP but there are two important differences.

The ADP numbers are generated from the 411,000 company clients whose payrolls are processed by the firm. The BLS numbers cover the entire economy including all levels of government employment.

The ADP numbers come from real payrolls that is they are a record of the paychecks of actual employees. The government payroll figures, while they list real payrolls also contain an estimate, based on the so-called birth-death model, of the number of new jobs created in the reporting month. Those jobs may or may not exist, the model was inaccurate in estimating the number of new jobs in the immediate aftermath of the recession. The conjectural jobs also may or may not last six months as most new businesses fail. These estimated jobs are corrected against tax rolls at a later date in the baseline revision to job data.

Reuters

The two averages have moved together this year. The three month moving averge for ADP has declined from 221,000 in January to 151,000 in August. Government numbers have fallen from 257,000 at the beginning of the year to 154,000 in July.

FXStreet

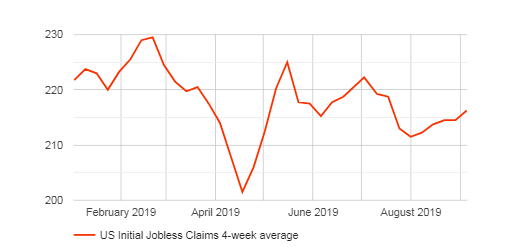

Initial jobless claims

Initial claims have been at or near 50 year lows for more than a year. The achievement is more impressive when one remembers that claims are straight numbers not percentages. In the past five decades the US population has grown 60% yet claims are on a par with 1969 when the country held just 203 million people, there are now 328 million citizens.

Claims are a late cycle indicator. People do not file until they have lost their jobs and this will not happen to large numbers in an economy wide basis until hiring has fallen substantially of halted.

The 4-week moving average was 216,500 in the week of August 30th.

FXStreet

Conclusion

Job creation has retreated somewhat from last year’s strong levels matching the relative decline in US GDP. However at an average of 178,000 monthly this year the market is providing more than enough employment to fill the needs of new entrants to the labor force. Combined with the backlog of unfilled positions over the past two years the upward pressure on wages should remain.

That surplus of work over workers has pushed employment into parts of American society that had long suffered from weaker employment. The current unemployment rates for Hispanics and African-Americans are the lowest on record.

Federal Reserve Chairman Powell has stressed the bank’s role in keeping this achievement, a product of the long-running expansion, intact. It is likely that this is now the chief rationale for the FOMC’s July 0.25% rate cut and the pending September reduction.

The almost two year old US-China trade dispute, by now a trade war, may yet be settled by the negotiations slated to resume again in October but markets have lost much of their original optimism. It and Brexit have had a large negative effect on the outlook and hiring plans of business executives particularly in the manufacturing sector. Though there was a revival in factory employment in June and July which averaged 14,000 new positions, after declining for a year, the drag on the manufacturing sector will continue until a new trade arrangement emerges.

The US economy expanded at a 2.55% rate in the first half and the current pace of consumption is probably sufficient to keep activity running at around 2% annually or a bit more. This rate of growth has proved capable, so far, of sustaining the expansion of the labor market. Coincident indicators show no sign that US firms are becoming reluctant to hire.

The stresses on the US and global economies are, despite their late cycle position, largely event driven. Whether the economy and labor market can weather another year or two of the current unease and indecision on trade is open to much question but for the moment the US labor market is taking its reference from the domestic economy and not the globe. The payroll risk for August remains, as it was in, July on the upside.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.