US monetary policy outlook: More questions than answers

In his press conference last week, Fed chairman Jerome Powell was very clear. Based on the FOMC’s two objectives – inflation and maximum employment – the data warrant to start hiking interest rates in March and, probably, to move swiftly thereafter. In doing so, it will be “led by the incoming data and the evolving outlook”. This data-dependency reflects a concern of tightening too much and makes monetary policy harder to predict. The faster the Fed tightens, the higher the likelihood of having it take a pause to see how the economy reacts.

14.3% versus 0.25%. More than any other metric, the gap between these numbers shows that US monetary policy is due for a fundamental change. The former refers to the increase, at an annual rate, of US nominal GDP in the fourth quarter of 2021. The latter is the upper limit of the current target range for the federal funds rate.

Admittedly, nominal GDP growth is a poor basis for assessing the stance of monetary policy. However, the number and its decomposition – real growth at 6.9% at an annual rate and inflation, based on the GDP deflator, at 6.9% – reflects the cyclical strength of the US economy but also the fact that inflation has become unacceptably high.

The pace of price increases not only weighs on household confidence because it erodes their purchasing power but it has also become a political topic and may influence the midterm elections on 8 November this year. In his press conference after the FOMC meeting last week, Jerome Powell was extremely clear. “In light of the remarkable progress we have seen in the labor market and inflation that is well above our 2 percent longer-run goal, the economy no longer needs sustained high levels of monetary policy support.”1 In plain English, this means that the federal funds rate will be increased, starting with the March meeting of the FOMC.

Moreover, to reinforce the hawkish message, the Fed chairman insisted that the economy and the labour market are much stronger and inflation much higher than at the start of the previous rate hike cycle in 2015. “These differences are likely to have important implications for the appropriate pace of policy adjustments.” This means a faster pace of rate increases and/or increases of 50bp3. In scaling back the degree of accommodation of monetary policy, the run-off of the balance sheet (quantitative tightening, QT) will only play a secondary role.

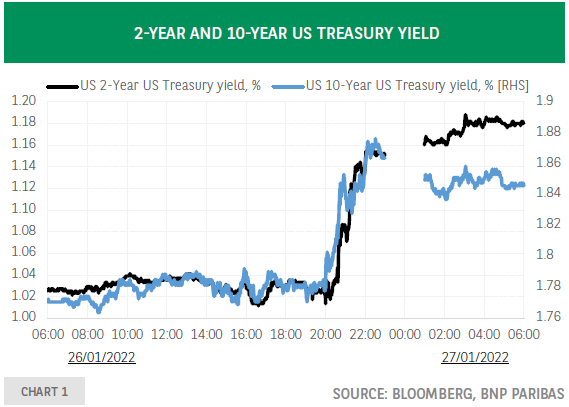

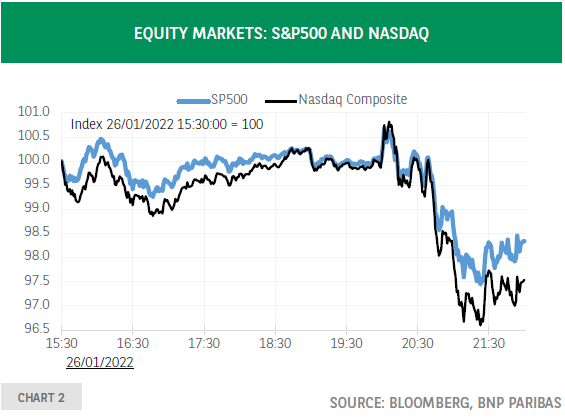

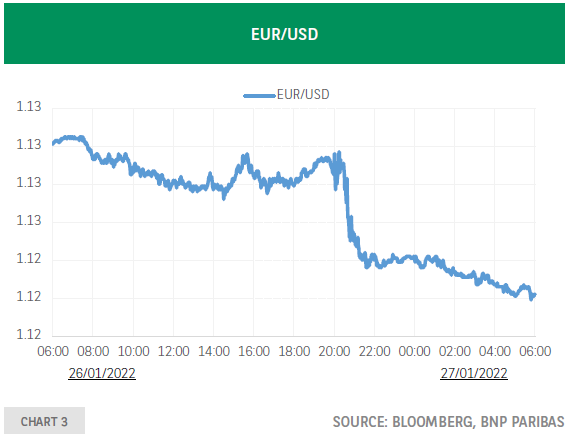

The FOMC sees “the target rate for the federal funds rate as its primary means of adjusting the stance of monetary policy”, whereby the balance sheet would decline in a predictable manner. This reflects the view that the consequences of rate hikes are easier to estimate compared to those of QT. Unsurprisingly, bond yields jumped (chart 1) with the 2-year yield rising slightly more than the 10-year yield, equity markets declined – the more rate-sensitive Nasdaq more than the S&P500 (chart 2) – and the dollar strengthened (chart 3).

Yet, despite the clear message that rates will be increased and that in all likelihood hikes will follow each other in swift succession, the monetary policy outlook is surrounded by a high degree of uncertainty, about the pace of rate hikes and the cyclical peak of the federal funds rate. This is nothing new. At the start of a tightening cycle, the same questions are asked time and again.

However, today’s inflation is partly caused by supply disruption and this complicates the analysis. Supply bottlenecks should be temporary as production picks up and the logistical problems in supply chains ease. This should reduce inflationary pressures. Moreover, high inflation originating in the supply side of the economy should weigh on demand thereby reducing the imbalance between demand and supply.

In addition and as emphasized by J. Powell, demand growth should also be influenced by a significantly smaller impulse coming from fiscal policy. On the other hand, elevated inflation has become broad-based5 and wage growth is accelerating due to persistent labor shortages. This should push prices higher: faced with strong demand, companies will find it easier to charge higher prices when wage and non-wage costs increase. This justifies the need for policy tightening, something that the labor market should be able to cope with, at least initially. “I think there’s quite a bit of room to raise interest rates without threatening the labor market. This is, by so many measures, a historically tight labor market, record levels”.

To conclude, the FOMC is of the view that, based on its two objectives – inflation and maximum employment – the data warrant to start hiking interest rates in March and to move swiftly thereafter. In doing so, it will be “led by the incoming data and the evolving outlook”. This data-dependency reflects a concern of tightening too much and makes monetary policy harder to predict. The faster the Fed tightens, the higher the likelihood of taking a pause to see how the economy reacts.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.