US Michigan Consumer Sentiment February Preview: Looking in the labor market mirror

- Sentiment to moderate slightly from eight month high.

- Current conditions index to edge higher, expectations to slip.

- Labor market performance is the key metric.

The University of Michigan will release its preliminary Survey of Consumers for February on Friday February 14th at 15:00 GMT 10:00 EST

The survey consists of three indexes--the Index of Consumer Sentiment, the Index of Current Economic Conditions and the Index of Consumer Expectations. Each is revised once. The survey began in 1978.

Forecast

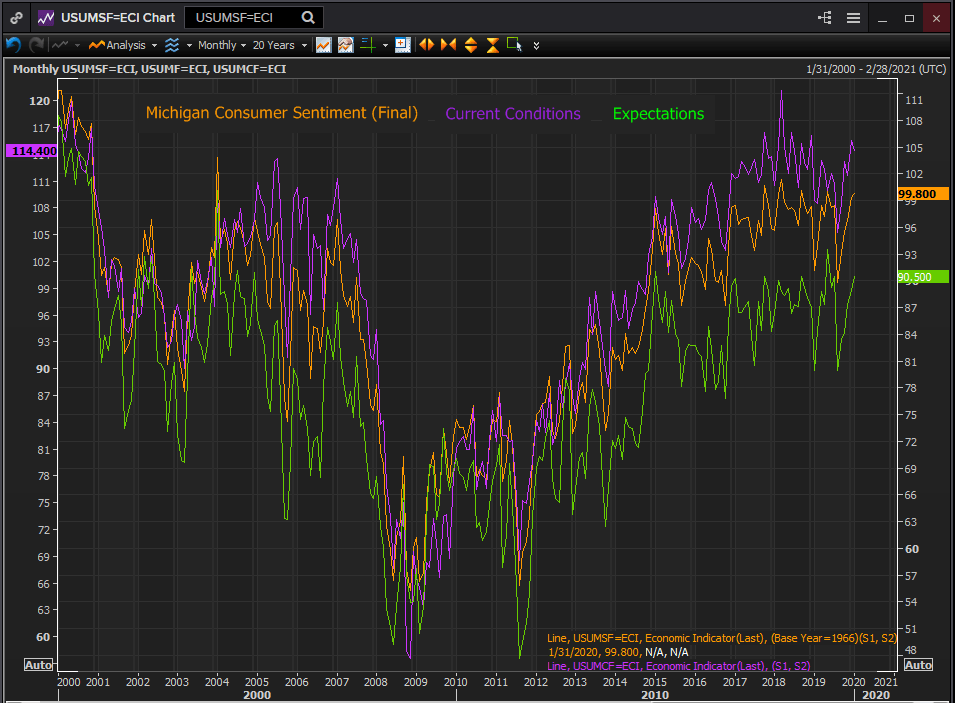

The Consumer Sentiment Index is expected to slip to 99.5 in February from 99.8 in January. The Current Conditions Index will rise to 115 from 114.4. The expectations Index will fall to 90.3 in January from 90.5 the prior month.

Michigan Consumer Sentiment

The sentiment index has made a very spry recovery from its August 2019 three year low of 89.8, a plunge largely caused by the negative trade rhetoric between the US and China at the time.

At 99.8 in the overall index in January, 90.5 in the expectations index and 114.4 in current conditions, the confidence of the US consumer in the present and the future is among the best of the past three years which themselves are the in the highest range of the past two decades.

Despite the endless political bitterness in Washington, China’s health crisis and economic malaise in much of the rest of the world, close to home America has remained cheerful.

Reuters

Sentiment and the labor market

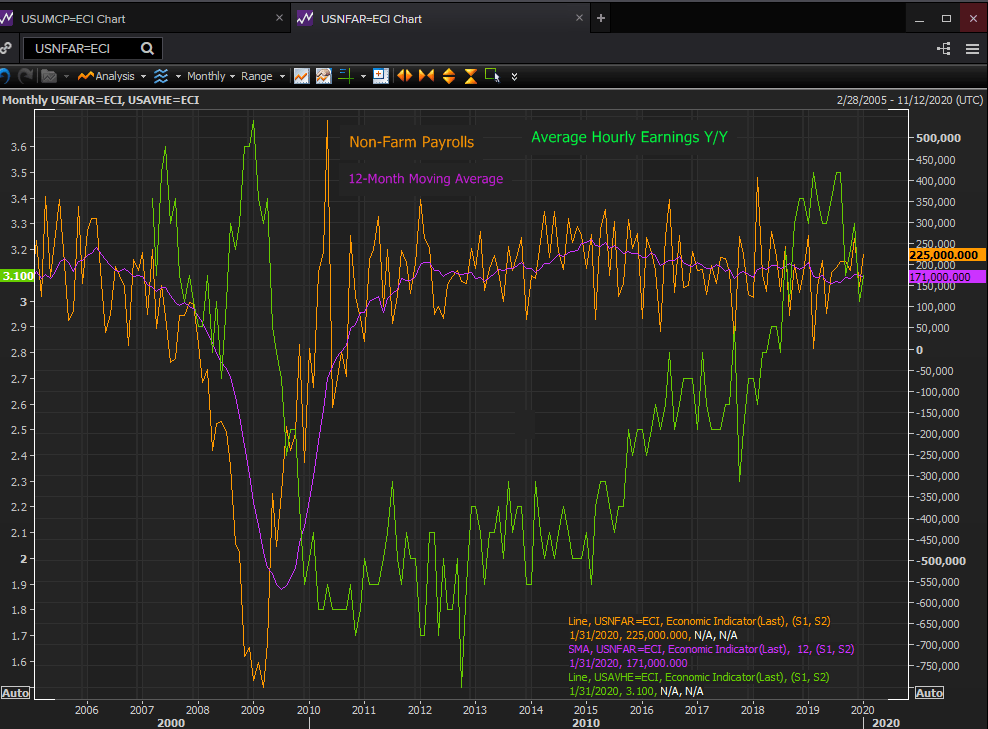

The most powerful ingredient in an individual’s sense of economic well-being is employment. The half-century low in the jobless rate, a surplus of work and wage gains at their highest in a decade provide ample evidence that US economy is performing. It is not surprising this achievement is reflected in the consumer outlook.

Non-farm payrolls averaged 175,000 new jobs in the 12 months to December. Though this was a decrease from the 235,000 average in January 2019 it is greater than the labor force increase of 125,000-150,000 new workers each month.

Reuters

This surplus of employment, which has continued every year since the economy made good the recession job losses in mid-2014, is the main reason that wage gains are close to their best levels of the decade despite the available labor pool represented by the recently improved but historically low 63.4% participation rate.

Annual average wage increases have been at 3% or higher for 18 months through January.

Personal income

This measure of income from the Bureau of Economic Analysis covers many sources of income left out of strict wage and salary accounting, including interest payments, dividends, workmen's compensation, pensions, social security and other transfer payments. It rose 0.2% in December.

The 12-month moving average for personal income has drifted lower this year to 0.317% in December from 0.375% in January and from 2018’s four year high of 0.508% that July and August. The numerous non-wage benefits current in the economy are a not inconsiderable addition to family and individual income.

Retail sales

Consumption remained on an even keel in December at 0.3% as in November. Purchases excluding automobiles rose 0.7% beating the 0.5% forecast and improving on November’s downwardly revised flat reading. The important GDP component ‘control group’ gained 0.5% in December marginally ahead of the 0.4% prediction, though the November result sank to -0.1% from 0.1% under revision.

Sales are expected to stay the course in January increasing 0.3%. Ex-autos should rise 0.3% down from 0.7% and the ‘control group’ will add 0.3% following Decembers 0.5% increase.

The moderate and steady gain in sales over the past year are an accurate reflection of the positive complexion of the consumer market.

Conclusion and the dollar

There is nothing in the domestic economy to upset the US consumer. Jobs and wages are bountiful, inflation and unemployment are low and people are moving from long-term joblessness back into the labor force.

The China health crisis has as yet had little impact in the US even if its economic effects are unknown and potentially substantial.

The dollar will continue to benefit from the US economic performance though the safety trade over the past two weeks has provided a notable boost.

As long as these conditions are intact US consumer confidence will be their mirror.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)