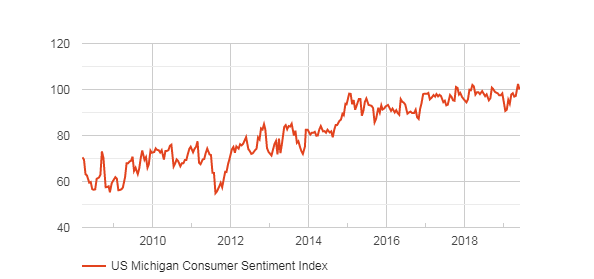

US Michigan Consumer Sentiment Preview: Happiness and caution

- Michigan Consumer Sentiment Index predicted to decline slightly in June

- Confidence may suffer from weak May non-farm payrolls

- Retail sales in April were unexpectedly soft

The University of Michigan will issue its preliminary Survey of Consumers for June on Friday June 14th at 8:30 am EDT, 12:30 pm GMT. The survey consists of three indexes--the Index of Consumer Sentiment, the Index of Current Economic Conditions and the Index of Consumer Expectations. Each result is revised once. The survey began in 1978.

Forecast

The Consumer Sentiment Index is expected to slip to 98 in June from April's revised score of 100.

Consumer sentiment and the economy

American consumer sentiment has consolidated at its best levels of the post-recession era after the volatility around the partial government shutdown in December and January.

Since the presidential election in November 2016 the Michigan Index has varied between 93.4 in July 2017 and 101.4 in March 2018 with the single negative exception of the January 2019 shutdown reading of 91.2. Post-closure the index has averaged 97.4.

FXStreet

The return to optimism by the US consumer is logical. Americans tend to disapprove of political machinations in Washington that impinge on the economic life and business of the country. Once the artificial conflict is removed consumer attitudes are based on the economic realities of jobs, wages and household stability.

The recent volatility in non-farm payrolls has introduced a note of caution in the job picture but it is neither extensive nor prolonged enough to have evinced a serious change in consumer outlook.

Payrolls have declined into the second quarter with the 3-month moving average falling from 245,000 in January to 173,700 in March and then 150,700 in May. The slippage was the result of two very slow months for hiring, February’s 56,000 and May’s 75,000.

Other labor market statistics remain at or near historical performance levels. The unemployment rate of 3.6% in May was the lowest in five decades and the 4-week moving averge of 215,000 exhibits no indication of impending layoffs. Average hourly earnings maintained their near 10-year high of a 3.1% annual increase.

One caveat on the labor market is that employers tend to restrict hiring before they begin layoffs.

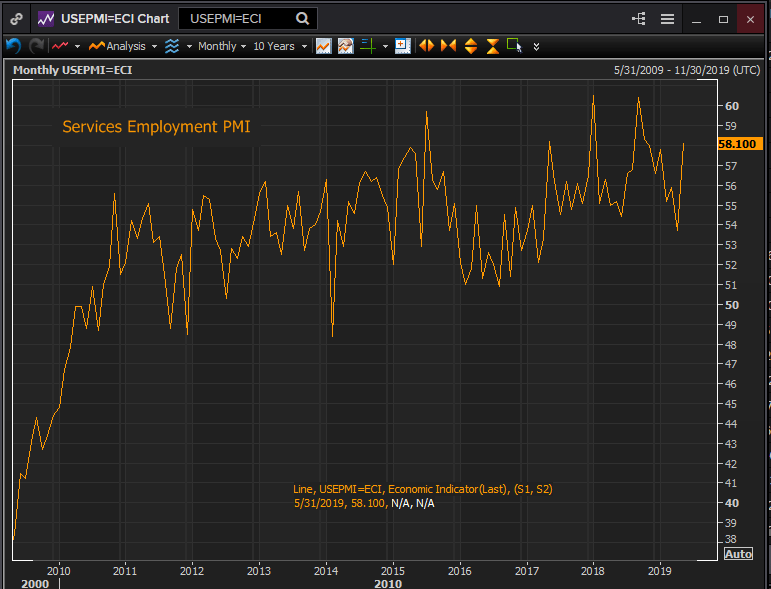

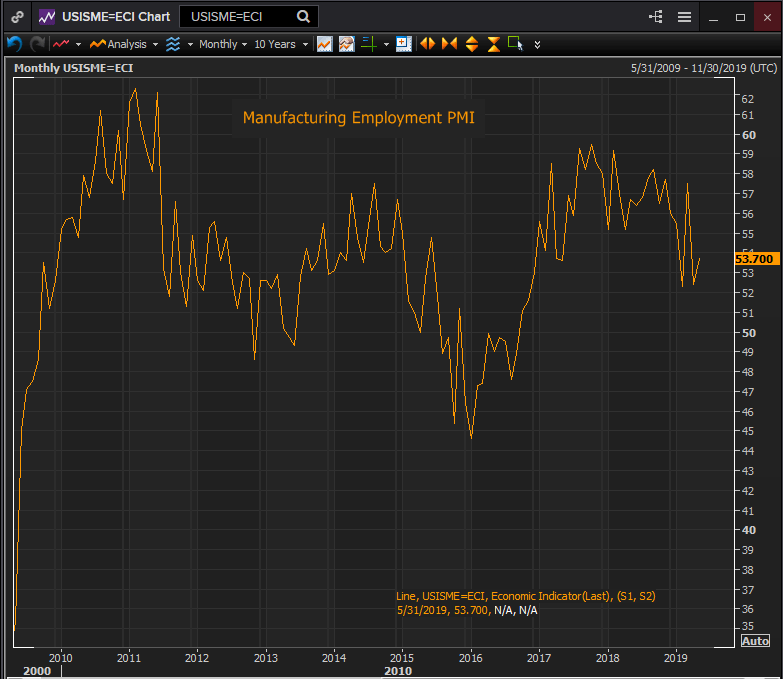

Business Employment Sentiment

Business optimism in the service and manufacturing sectors over hiring and employment has recovered in May after falling for most of the previous six months. The service score of 58.1 is in the middle of the post-recession range while the manufacturing reading at 53.7 is in the lower reaches.

Reuters

Reuters

Conclusion

The most important factors in consumer attitudes employment and wages remain at their best levels of the past ten years.

It is unclear whether the recent stuttering in non-farm payrolls is the result of a change in business outlook, evidenced by the decline in business employment sentiment of the past-half year, a pull-back after two exceptionally strong years of employment expansion or a sign of future decline, and that is without noting the recovery in optimism in May. Over the last decade the cycles of this index have not generally predicted variations in hiring.

The drop in business hiring sentiment has occurred as the reality of hiring continued apace. There is potential for a similar if reversed disconnect in consumer attitudes and spending. The weakness in April’s retail sales and their recent volatility may be a sign of pratical caution in consumption that has not, as yet, reached the underlying consumer optimism.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.