US January CPI: A brief market primer

- CPI forecast at 7.3%, core at 5.9% in January.

- Markets watching CPI for indications of Fed policy.

- Higher inflation raises the possibility of a 0.5% hike in March.

Inflation is the markets’ new volatility goodness. Prices haven't dethroned payrolls but Thursday’s US Consumer Price Index (CPI) promises a good dose of excitement if the result strays very far from the 7.3% forecast for January.

The pandemic lockdown and the subsequent flood of liquidity from the Federal Reserve and the US government has combined, a year later, with labor and material shortages for manufacturing and a supply chain tangle that has stretched around the world, to produce the highest American consumer inflation rate in four decades.

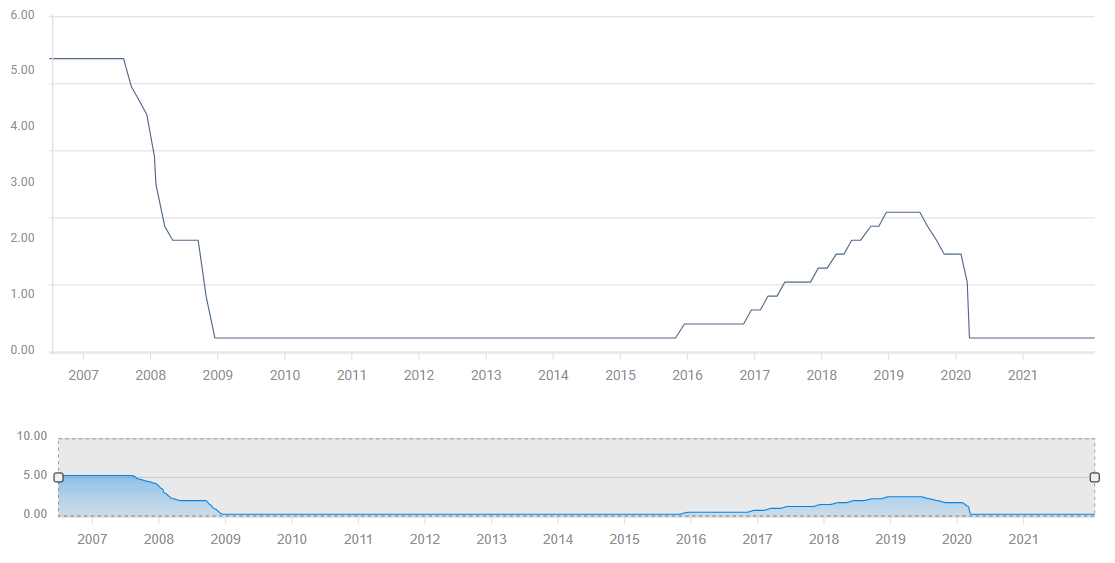

Federal Reserve policy has completely reversed in five months. From the first mention of an end to the $120 billion bond program in the September 22 Federal Open Market Committee (FOMC) statement, to the doubling of the monthly reduction in the December 15 statement, and an implied promise for a 0.25% fed funds increase, and a bruited balance sheet reduction at the January meeting, Fed policy has been at the center of the inflation storm.

Fed funds rate

FXStreet

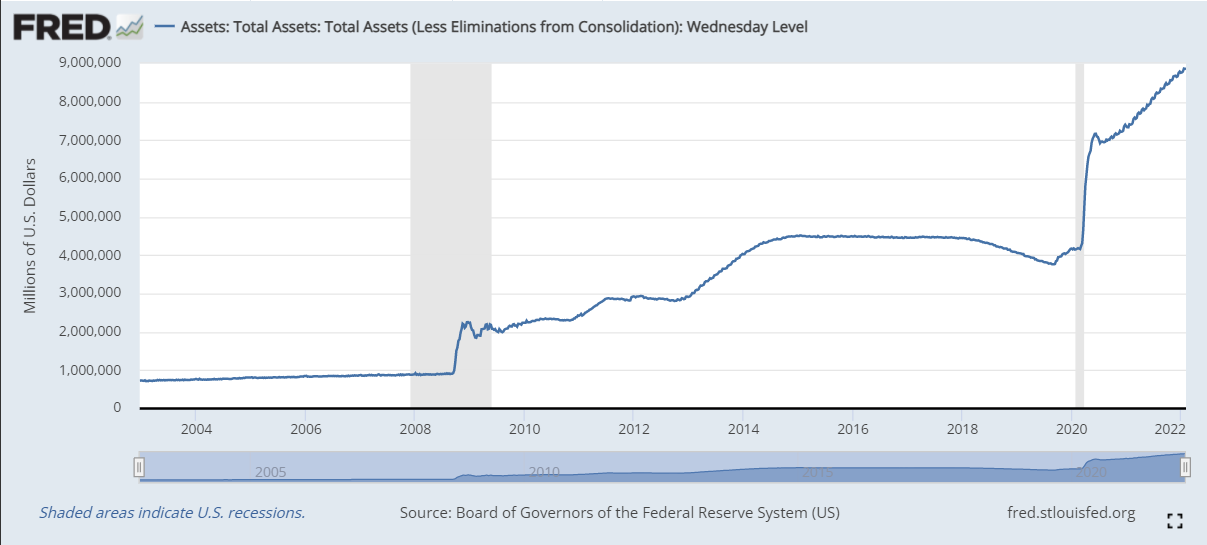

The bond program will end next month and the first rate hike in three years is universally anticipated at the March 16 meeting, but that does not end the options for this FOMC. The governors could choose to raise the fed funds rate 0.5%. That is a 24% chance according to the Chicago Board Options Exchange (CBOE). Federal Reserve Chair Jerome Powell has said the reduction of the almost $9 trillion balance sheet could begin once the bond program ends. Until recently that was assumed to be some future month after the end of purchases, but there is no reason it couldn't begin in March.

Federal Reserve assets

It is very likely that the fed governors have not yet determined the answers to those questions. Either or both actions would send a strong signal to the credit markets that the Fed wishes a faster appreciation of interest rates. Treasury yields, commercial interest rate, equities and the dollar would move dramatically.

Neither a half-point increase in the fed funds or a start to the portfolio reduction is currently expected. Economic statistics over the next four weeks will determine the Fed policies, and chief among that information are the inflation figures: January CPI on Thursday, PPI next Tuesday and PCE prices on February 25. Next month, February CPI will be out on March 10 and PPI on 15, before the FOMC meeting on 16.

Let’s look at the three scenarios for Thursday’s CPI and judge the likely markets’ response.

CPI from 7.1% to 7.3%, core from 5.7% to 5.9%.

Consider this the expected tranche. Inflation slightly less than forecast could be monthly variation, and does not necessarily mean a peak has passed. In August the index dropped 0.1% to 5.3% before accelerating to 5.4% and 6.2% in the next two months. With this result, inflation is still rising but it is probably not sufficient to prompt a further tightening in Fed policy. Market expectations for a 0.25% fed funds increase and future portfolio reduction, perhaps detailed, remain in place.

As these are the existing predictions, they are largely priced. Equities should continue their recovery, Treasury rates their slow rise and the dollar would likely lose modest ground as it needs faster Treasury yield increases for continued gains.

CPI higher than 7.3%, core above 5.9%.

This is the acceleration tranche. Markets will assume that speedier inflation will draw a more emphatic Fed response in the fed funds or the balance sheet or both. The higher CPI, the greater its trading impact. Equities will fall, particularly the rate sensitive stocks, Treasury yields will rise and the dollar should gain ground on its competitors.

CPI below 7.1%, core below 5.7%.

This is the deceleration tranche. A drop of 0.3% or more in CPI does not mean inflation has peaked but the lower the rate the greater the likelihood it is the start of a trend. Markets will assume a much lower probability for a 0.5% fed funds increase or balance sheet reduction at the March FOMC. Equities will forge higher, Treasury yields will abate and the dollar should fall.

Conclusion

One inflation report, even if dramatically ahead or behind forecasts, will not make Fed policy. It does however, alter the odds.Trading is nothing if not a bet on possibilities.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.