US ISM manufacturing slips to 48.5 in May from 48.7 the month prior

The U.S. Institute for Supply Management (ISM) reported a reading of 48.5 for May 2025, down slightly from 48.7 in April 2025. This decline may reflect the fluctuating tariff policies of President Donald Trump. Although the decrease is marginal, the ongoing contraction in the nation’s manufacturing sector, coupled with supply chain disruptions and changing demand dynamics, is having ripple effects throughout the global economy. In this article, we will take a closer look at the breakdown of the report and examine the broader implications for the global economic environment.

The clearest evidence that tariffs are weighing on manufacturers comes in the form Responses from respondents to the latest ISM survey indicate several key concerns. Many suppliers are fully passing on the costs of tariffs, and the uncertainty surrounding tariffs is affecting international orders. Additionally, tariffs have caused supply chain disruptions that are comparable to the impact of the pandemic. Furthermore, the unpredictable nature of tariffs makes planning challenging, as contingency measures are diverting attention from more strategic initiatives.

Construction activity has been stagnant, remaining under contract for a third consecutive month, with this trend expected to continue into April 2025. This decline is largely attributed to a slowdown in the private sector. Rising tariffs have likely increased construction costs, contributing to growing uncertainty and diminishing confidence in the building sector. As a result, we anticipate further weakening in the manufacturing sector for the remainder of 2025.

In light of recent ISM manufacturing data, market participants should pay close attention to the economic calendar for additional insights. Upcoming reports for the United States include April’s job report, which is anticipated to show a modest decline in job openings and labor turnover. Additionally, job growth is expected to be reported at 120,000 for May, following an increase of 177,000 jobs in April.

Market and economic implications

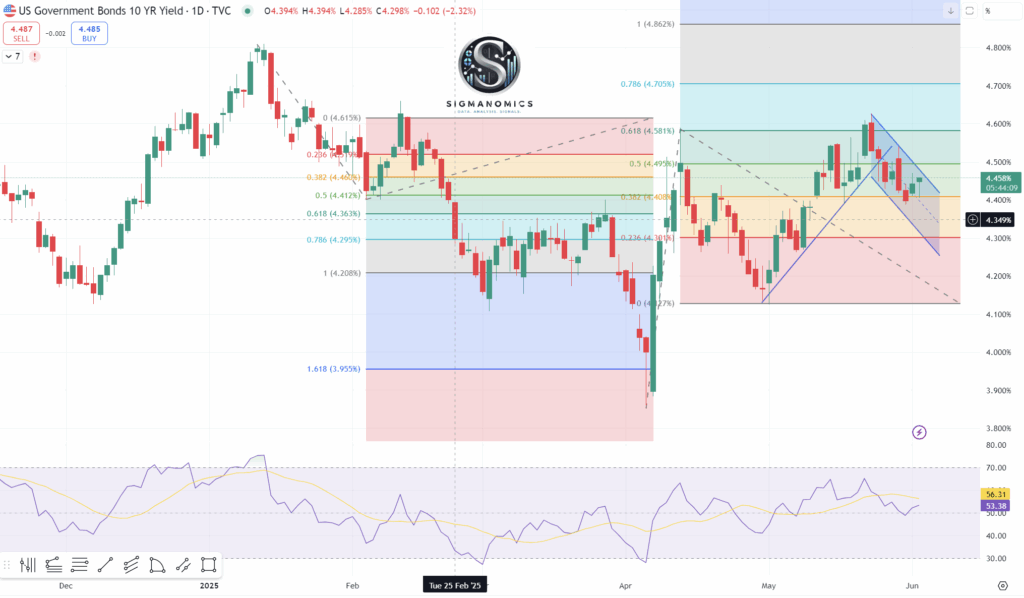

Recent price movements of U.S. 10-year Treasury bonds have stalled at the 61.8% Fibonacci extension level, which corresponds to the swings between 3.86% price and 4.59%, as well as 4.12%. The reversal at 4.60% also coincides with the 78.6% Fibonacci retracement level from the downswing between 4.80% and 3.86%. Overall, our analysts at Sigmanomics forecast that as long as the level of 4.80% remains unbroken, a decline below 4.10% by the end of 2025 is possible, with a potential target of 3.90% thereafter.

Michael Delgado, Senior Portfolio Manger at Pimco recently stated “We recommend underweighting long-duration positions. The Fed’s inflation fight is not yet won, and core services inflation remains elevated. We favor floating rate notes (FRNs) and short-dated TIPS to protect against unexpected rate hikes.” Likely to witness a negative effect from this outlook are Utilities and Real Estate Investment Trusts, long-duration bond holders, and high-growth tech stocks.

May 2025 ISM manufacturing report signals that the U.S. industrial sector remains in a delicate position between supply chain recalibrations, softening demand in the United States, and tariff-driven cost pressures. On the back of a third straight monthly spending contraction and rising costs, we do not rule out a broader slowdown in private investment. At the same time, as hiring cools, consumer and business sentiment has softened, which has heightened the risk that consumer spending will decelerate more than previously forecasted. Much of the remaining 2025 hinges on the U.S. administration and seeing if a agreement regarding trade policy can come to light. It is advised for traders to maintain vigilant risk management and a readiness to recalibrate allocations as conditions evolve.

Author

Sigmanomics

Sigmanomics

Sigmanomics is a financial intelligence platform that delivers expert insights, data-driven analysis, and real-time trading signals across global markets.