U.S. Inventories: Cushion to Virus Impact

Executive Summary

Extended production stoppages and transportation bottlenecks in China have left the U.S. manufacturing sector as the area of the domestic economy perhaps most exposed to the coronavirus outbreak. Most industries are entering this period with high levels of input inventories so, generally speaking, most American industries have more cushion against production being disrupted than prior periods of supply chain shocks. That said, the computer & electronic products industry in the United States is notable. Not only does the industry source roughly 10% of its inputs from China, but it is an important cog in the production process of other industries, both in the industrial and service sectors. If Chinese factory shutdowns and transport issues persist long enough, production in the American manufacturing sector eventually could be adversely affected.

Still Reeling

The COVID-19 coronavirus, which burst on to the scene only a few weeks ago, has quickly become the center of attention in financial markets. In a series of reports that we have written over that period, we have analyzed potential economic implications from the epidemic. Our most recent report, which we published on February 12, discussed potential effects on the U.S. supply chain from factory closures in China. We extend that supply chain analysis in this report.

To recap, Chinese production usually shuts down during the Lunar New Year holiday, which was supposed to have ended on January 30 this year. However, Chinese officials extended the holiday to February 2 in an effort to more effectively arrest the spread of the virus. Certain regions and businesses further delayed the resumption of production and businesses specifically in Hubei province—the origin and epicenter of the coronavirus—extended closures until February 14. For companies that have reopened, they may not be operating at full capacity. The situation remains fluid, with the case and death toll unfortunately continuing to rise, and the extent to which Chinese production can resume in the very near term is still uncertain.

Not only is China the world's second largest economy, but U.S. supply chains are more entwined with China today than in the early 2000s during the SARS outbreak. A prolonged delay in Chinese production could cause adverse effects to global supply chains and certain U.S. manufacturing industries. In this report, we build on our February 12 report to analyze how the U.S. factory sector could potentially be disrupted.

U.S. Inventories of Input Products Generally High

The effect on the U.S. manufacturing sector from the coronavirus comes down to how integrated production is with China specifically, and the global economy more broadly. If manufacturers source inputs from China, then their production could be at risk of Chinese factory closures, or transportation delays in getting goods stateside. But, if U.S. manufacturers have high levels of inputs on hand, production should be able to weather a supply disruption, at least for a time.

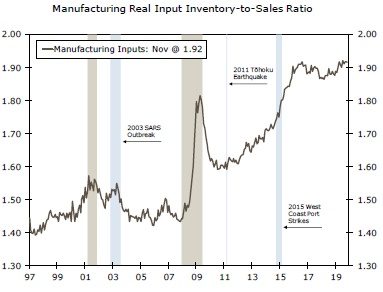

To ascertain how vulnerable the U.S. manufacturing sector is to a potential supply chain disruption, we first estimated how much input inventory manufacturers currently have in stock. 1 As shown in Figure 1, our estimated input inventory ratio has trended steadily higher since the advent of the Great Recession and currently stands at an all-time high. The ratio today stands at a significantly higher level than in prior periods of supply chain shocks, such as during the 2003 SARS outbreak, the 2011 Tōhoku earthquake and the 2015 West Coast Port Strikes, which should provide some cushion to manufacturers' production processes.

Source: U.S. Department of Commerce, Federal Reserve Board and Wells Fargo Securities

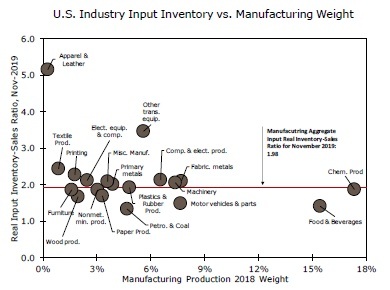

Notably, some of the largest industries have below-average inventories of inputs on hand relative to the entire manufacturing sector, suggesting an outsized risk to production. Take the chemical products industry as an example (Figure 2). Because chemical products account for the largest individual share of U.S. manufacturing production, at nearly 18%, a disruption to production in this sector could significantly curtail total U.S. manufacturing output.

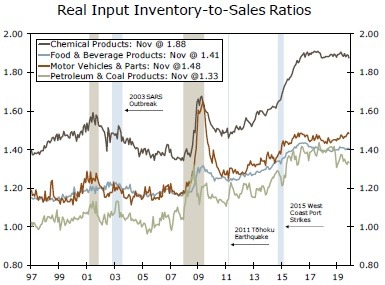

That said, despite its "lower" level of inventories, the chemical products input inventory ratio is still well above where it stood prior to past supply shocks (Figure 3). In fact, ratios in nearly every industry—besides the computer & electronics and wood products industries—stand above levels at prior disruptions.

High levels of input inventories could support chemical production in the short term and, as we emphasized in our February 12 analysis, the chemical product industry sources only a small share— less than 2 percent—of its inputs from China. Therefore, supply disruptions only from China should not pose a significant risk to production in the American chemicals industry. But as we also noted in our previous report, the American chemicals industry imports about 20% of its inputs (the remaining 18% come from countries other than China). Consequently, if the virus were to continue to spread and cause production disruptions on a global scale, then the U.S. chemical products industry could be more at risk of a production disruption.

Source: U.S. Department of Commerce and Wells Fargo Securities

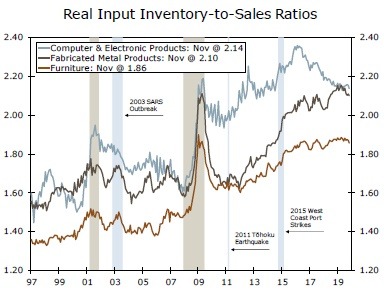

American industries that appear most immediately at risk are those that rely on inputs from China and have low inputs in inventory. For example, the computer & electronics industry imports nearly 10% of its inputs from China and input inventories in this sector are near their lowest level in five years (Figure 4). Consequently, production in the computer & electronics products industry in the United States could eventually be disrupted if it is unable to source imports from China. Because this industry accounts for roughly 6% of the manufacturing sector, overall manufacturing production in the United States would be adversely affected in a direct way if production in the computer & electronics products industry were to grind to a halt.

Furthermore, there could be knock-on effects across industries. That is, if computer & electronics production is curtailed, industries that rely on the sectors' output as their own inputs could also be adversely affected. For example, computer & electronic products are the largest inputs in industries such as other transportation equipment, electrical machinery and printing. Moreover, computer & electronics is the most commonly used durable input in the services industries, so any production disruptions could weigh on near-term service sector output. Although we cannot identify how much stock of computer & electronic products each industry holds in inventory, we do take some comfort from the observation that input inventory ratios in most industries are currently at their highest levels in years.

Conclusion: Starting Off on a Good Foot, but Much Still Up in the Air

In sum, high levels of input inventories gives production in most American industries some cushion against supply chain disruptions from China. That does not mean the current virus outbreak, however, will not have a bearing on overall GDP growth. As Chinese production and shipments are delayed, U.S. inventories will be pared down more quickly than they otherwise would be.

Moreover, production in the American manufacturing sector eventually could be adversely affected if Chinese factories were to shut down for an extended period of time (i.e., a month or more). In addition, while inventories of input products are at generally high levels, it may only take one part running out of stock to shut down production of certain products. Stay tuned.

Author

Wells Fargo Research Team

Wells Fargo