US Initial Jobless Claims: Can claims and payrolls rise at the same time?

- Initial claims expected to remain stalled at 1.408 million.

- Continuing claims to drop to 16.839 million from 17.018 million.

- Dollar weak on US second wave and economic worries.

Initial jobless claims are forecast to show little improvement in the latest week as businesses continue to lay off workers or fail in the uneven economic recovery from the pandemic shutdown.

First time filings for jobless benefits are forecast to be 1.408 million in the July 31 week, a small drop from 1.434 in the prior period and exactly where they were six weeks ago on June 26.

Continuing claims projected to dip to 16.839 million from 17.018 million. The low has been 16.151 million the week of July 10.

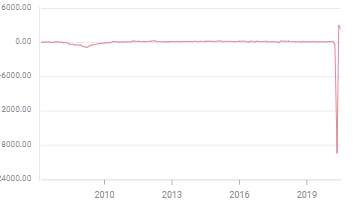

Initial and continuing claims

Claims peaked on March 27 at 6.867 million and over the next three months to June 26 they fell 79% to 1.408 million. Since then there has been minimal improvement to 1.307 million on July 10 followed by two weeks of higher volume, 1.422 million on July 17 and 1.434 on July 24.

Initial jobless claims

The pattern for continuing claims is similar. The high of 24.912 million came on May with a 35% decline to 16.151 million by July 10 and then a small rise to 17.018 million on July 17.

The four-week moving average for initial claims reached a low of 1.362 million on July 17 then rose to 1.3685 on July 24.

Second wave and high frequency data

The rise in Covid cases in several Southern and Western states since the beginning of June eventually required some tightening of business operating rules. That partial pullback in Texas, Florida and elsewhere combined with a number of states that have been slow to release their businesses from restrictions has resulted in a steady stream of new layoffs and unemployment claims.

The lengthening slowdown and weak consumer traffic for many businesses is forcing small stores into bankruptcy, permanently ending employment for their workers. The longer consumer life remains weak the more business will fail and the greater the number of employees thrown back onto jobless benefits.

Some high-frequency data, meaning weekly numbers, from credit cards, restaurants and travel bookings, seem to indicate that there has been a slackening of consumption in July after strong gains in June.

The rise in initial claims from 1.307 in the July 10 week to 1.434 on July 24 is part of that high frequency shift.

ADP and non-farm payrolls: Claims and consumer confidence vs July PMI and Fed surveys

The July rise in initial claims is expected to presage a substantial decline in July hiring.

Private payrolls from Automatic Data Processing (ADP) are forecast to fall by 37% from 2.369 million in June to 1.5 million in July. National payrolls are projected to drop by two-thirds from 4.8 million in June to 1.6 million in July.

ADP employment change

Other than the initial claims figures in the second half of July direct evidence for a large fall in new payrolls is thin. The drop in consumer confidence in the Michigan survey from 78.1 in June to 72.5 in July and in the Conference Board gauge from 98.3 to 92.6 indicates a change but it could be from any number of causes aside from a fading job market.

Michigan consumer sentiment

Business sentiment measures continued to improve in July.

Manufacturing activity improved in July. The ISM purchasing managers’ index climbed to 54.2 from 52.6 in June, passing the 53.6 forecast. New orders jumped to 61.5, the highest reading since September 2018, from 56.4 in June and far ahead of the prediction for a drop to 46.8%. Only the employment index at 44.3, though an improvement from June’s 42.1, missed its 48.3 forecast and remained in contraction.

Manufacturing PMI

Survey indexes for regional manufacturing from the New York, Richmond and Kansas City Federal Reserve banks rose sharply in July and only the Philadelphia index had a small decline, though it was better than forecast.

Conclusion and markets

One possibility is that the initial claims and payrolls figures are responding to two different labor market trends. The continuing layoffs represented by the claims numbers may come from struggling and failing small businesses that cannot exist without substantial foot traffic, something still missing in many cities.

Payrolls on the other hand may show the growth, expansion and hiring in the larger businesses covered in the improving manufacturing PMI figures and the likely gains in the larger service sector.

Currency markets have sold the US dollar against the majors over the last three weeks on expected economic weakness from the second wave of Covid cases. The stalling labor market is a main component of that scenario with non-farm payrolls on Friday the key metric but claims will set the stage.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.