US – Fed preview: Not stealing the spotlight

-

We expect the Federal Reserve to maintain the Fed Funds Rate unchanged at 4.25-4.50% in the January meeting, in line with wide consensus and market pricing.

-

The Fed communicated back in December that the January meeting would very likely mark a pause in the easing cycle. We still believe in the next cut in the following March meeting, but do not expect to hear strong forward guidance yet.

- Upcoming fiscal and trade policies are already playing a role in the participants' projections, and Powell will remain cautious in his remarks amid the current high uncertainty. We think risks are skewed towards higher EUR/USD over the coming month, but do not expect strong reaction around the rate decision.

Incoming data has provided Powell with no reason to deviate from the course outlined in December. After reducing restraint by 100bp and as downside risks to economic growth have eased, the Fed will pause its cutting cycle in January to evaluate incoming data and not least the upcoming fiscal and trade policies from the new administration.

Trump has so far announced a likely 10% increase to tariffs against China alongside 25% for Canada and Mexico. While we believe more tariff hikes will eventually be in the pipeline, markets have found comfort in Trump avoiding more erratic changes for now. Importantly, we still have little detailed information on the other items on the fiscal policy agenda, such as the upcoming tax reform. Hence, while the December minutes revealed that some participants have already made preliminary assumptions on the policies, Powell will likely refrain from strong forward guidance for now.

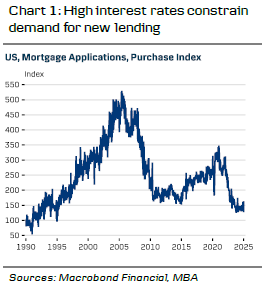

We still doubt tariff hikes alone will lead to persistent boost to inflation unless they are coupled with significant easing to domestic tax policies. For now, the current level of interest rates continues to have a restrictive effect on credit growth, which is evident in low mortgage application volumes (chart 1) and weak business loan demand in the Fed's latest SLOOS survey. Aggregate bank lending growth has stabilized close to 2.5% y/y, still clearly below the typical 5% pace observed before the pandemic.

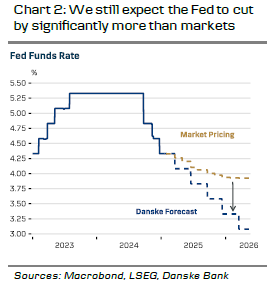

As such, we think current rates remain somewhat above neutral. As realized inflation data has continued moderating, we think the Fed can continue cutting rates when the next round of economic forecasts is released in the March meeting. We continue to forecast quarterly 25bp cuts until the policy rate target reaches 3.00-3.25% level in March of 2026 (chart 2). We will also continue monitoring any comments about QT towards the spring, although we do not expect any exact guidance quite yet. The government debt ceiling became binding again from the start of the year, which forces the Treasury to draw down its cash balance at the Fed to fund the ongoing deficits. This will counteract most of the liquidity tightening effect from QT for next few months, but we think either tapering or even ending QT might become timely sometime during the 2nd half of 2025.

For the time being though, the Fed has little reason to shake the markets. We continue to see near-term (1-3M) downside risks to UST yields and upside risks to EUR/USD but have no strong convictions for the Wednesday evening.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.