US Fed Interest Rate Decision April 28-29 Preview: It’s all about Projection

- FOMC will assess its policies of the past eight weeks, no initiatives expected.

- Confidence in its actions and the US economy and vigilance are the likely message.

- Fed is expected to release its quarterly Projection Materials originally scheduled for March 17-18.

- View forward will depend on the success in reopening the US economy.

After the extraordinary economic and policy events of the last two months the Federal Reserve will likely use its scheduled April meeting to assess the current and future states of the US economy and to project a message of vigilance, determination and hope to the financial community and the country at large.

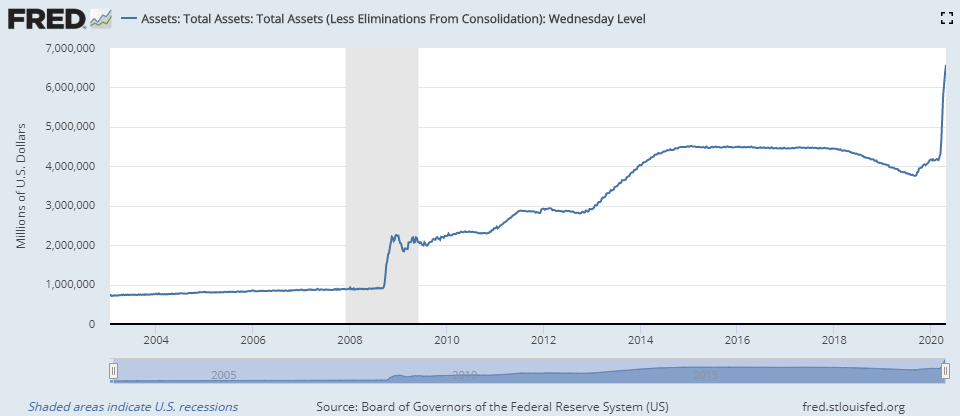

Fed policies and balance sheet

Since the beginning of March the Federal Reserve has cut the fed funds rate from 1.75% to 0.25%, restarted a $700 billion bond purchase program, instituted extensive swap lines with central banks around the world, opened unlimited quantitative easing and begun a $2.3 billion loan provision for business and local governments.

The two rate cuts on Tuesday March 3 and Sunday March 15 came before the first statistical indication of the enormous impact of the government ordered business shutdown on the labor market. The first notice came on March 26 with 3.283 million jobless claims followed by 6.867, the all-time US record, the next week. In making its decision the Fed governors relied on information from their extensive network of private and commercial contacts.

The FOMC has headed off a severe dollar funding crisis, stabilized global financial markets and projected an air of confidence in its actions and the US economy despite the enormous dislocations caused by the closure of large parts of American economic life.

In doing all this the Fed's balance sheet has risen to an all-time high of $6.6 trillion, surpassing the $4.5 total during the financial crisis. In two months (February 26 to April 22) the central bank has added $2.4 trillion in assets, meaning it has purchased that amount of financial instruments from the market. In six years of financial crisis purchases (September 2008 to January 2014) the bank added $3.6 trillion in assets.

Markets

Equity, credit markets and currency markets have calmed over the past two weeks with reduced volatility, helped by the Fed’s actions in providing essentially unlimited reserve dollars to the global financial system.

Risk aversion is still the basic scenario for the dollar though the longer without new negative economic or viral developments, the weaker the safety trade becomes.

Shutdown blues

Over the past eight weeks more than 26 million American have been thrown onto the unemployment rolls, many of them lower paid hourly or contract workers with few resources, as most but not all state government have shuttered business they deemed non-essential. The employment toll is expected to rise by 3.5 million more this Thursday bringing the total to 30 million workers, 18% of the labor force.

The 701,000 job losses in the March non-farm payroll report and the 0.9% jump in the unemployment rate to 4.4% are expected to be the precursors to far larger and higher numbers in April.

Most of these workers will be able to collect unemployment insurance for 26 weeks but damage to consumer spending was already evident in March’s consumer spending even though the layoffs did not begin until mid-month.

Retail sales and durable goods

Retail sales fell 8.7% in March, the largest amount on record, as wages losses and ‘stay-at-home orders drastically curtailed consumer spending despite the relatively normal economic activity in the first half of the month.

Retail sales

Durable goods orders dropped 14.4% with a portion of the decline due to car dealerships being closed across the country. Excluding the transport sector, Boeing Company of Chicago lost $16 billion on cancelled aircraft orders, goods orders slipped just 0.2%, far less than the -5.8% predicted.

GDP Q1 and the Fed’s Projection materials

The rapid collapse of employment in March kicked the consumption legs out from a US economy that is 70% dependent on consumers and had been expanding at an estimated 2.7% in January and February by the Atlanta Fed GDPNow model.

First quarter annualized GDP is expected to be -4% when released by the Bureau of Economic Analysis on Wednesday, with a range of estimates from the Reuters survey of -1% to -15%. Current projections into the second quarter vary widely from -5% to -30% and more as economist try to model the unique events of the last two months.

It is expected that the Fed’s own quarterly economic and rate estimates, its ‘Projection Materials’ will be issued this month. They were originally scheduled for the superseded and then cancelled March 17-18 FOMC meeting.

The Fed’s economists have had an additional five weeks to collect and analyze current data and project three years into the future. There will be exceptional interest in the Fed’s view though in the past the central bank’s prognostications have been no more accurate that others in the market.

Powell press conference

Federal Reserve Chairman Jerome’s Powell’s statement and press conference following the FOMC policy announcement will also be of exceptional interest.

The Fed’s actions during the health and economic disasters of the past two months have helped to calm markets and prevented a funding breakdown in the global financial system. But markets and traders always look ahead. The Fed’s information and power make it a fount of useful speculation, particularly in the current situation, where every prediction and calculation is, at best, an educated guess.

Conclusion

The Fed’s view into the next quarter and through the end of the year will be the paramount interest at Wednesday’s FOMC meeting.

An optimistic set of projections from the central bank and a hopeful and positive assessment for the US economy from Jerome Powell, especially with a number of states lifting restrictions, will reinforce the equity rally and could begin the end of the dollar panic trade.

Expect the Fed to be cautiously upbeat, confident of its policy choices and ready to act if needed.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.