U.S Dollar’s Glass Chin

Yesterday’s FOMC meeting minutes showed that U.S policy makers are somewhat split over whether inflation expectations are well “anchored.”

Some members continue to require confirmation that a drop in the inflation rate is only ‘transitional’ before there is another rate hike stateside.

Members agreed that the economic activity had risen and that the U.S labor market had continued to strengthen on average since the beginning of the year, but are stymied on why inflation remains subdued or benign.

In truth, yesterday’s minutes did not seem to offer anything much different than what the market already knew. Regardless of when the Fed next raises rates, it is widely expected to tighten monetary policy very “gradually” over the longer-term, and reason enough for investors to interpret the minutes as being a tad “dovish.”

European stocks slipped after a mixed Asian session while sovereign bonds have followed U.S Treasuries higher as the market digests the reduced odds of another rate hike this year.

Note: This morning’s ECB minutes (07:30 am EDT) will be eyed for clues of QE exit.

1. Stocks mixed results

In Japan, stocks felt the weight of a rebounding yen (¥110.00) and edged down overnight in thin trade. The Nikkei share average ended -0.1% lower while the broader Topix shed -0.2%. Turnover was only ¥1.806T, below the average daily ¥2T.

In Hong Kong, shares closed slightly down as profit-taking outweighed solid gains by the gaming and social media sector. The Hang Seng index fell -0.2%while the China Enterprises Index also lost -0.2%.

In China, industrial and materials stocks helped lift regional bourses higher as well as investor hopes that there will be significant changes to open up the economy more widely to foreign investors. The blue-chip CSI300 index rallied +0.5%, while the Shanghai Composite Index gained +0.7%.

In Europe, regional indices trade slightly lower following yesterday’s pullback on Wall Street, with corporate earnings remaining the focus.

U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx600 -0.2% at 378.2, FTSE -0.3% at 7411, DAX -0.3% at 12223, CAC-40 -0.4% at 5156, IBEX-35 -0.8% at 10468, FTSE MIB -0.3% at 21924, SMI -0.8% at 8973, S&P 500 Futures -0.1%.

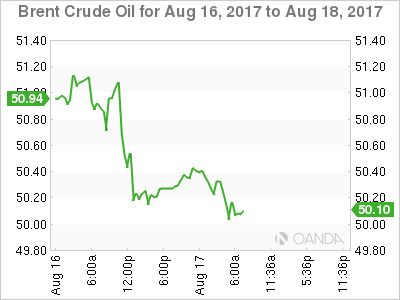

2. Oil steadies as high U.S output balances crude stock draw, gold higher

Ahead of the U.S open, oil prices trade steady after yesterday’s U.S data showed a big fall in crude stockpiles, but also an increase in production to its highest in more than two-years.

Brent crude is unchanged at +$50.27 a barrel, while U.S light crude (WTI) is -5c lower at +$46.73. Both benchmarks fell more than -1% Wednesday.

Yesterday’s EIA data showed commercial U.S. crude stocks had fallen by almost -13% from their peaks in March to +466.5m barrels. Stocks are now lower than in 2016.

But U.S oil output is rising fast as shale producers take advantage of a recent increase in prices – production jumped by +79k bpd to over +9.5m bpd last week, its highest level in two-years.

Note: Rising U.S output continues to undermine efforts by OPEC and non-OPEC producers to drain a global fuel glut.

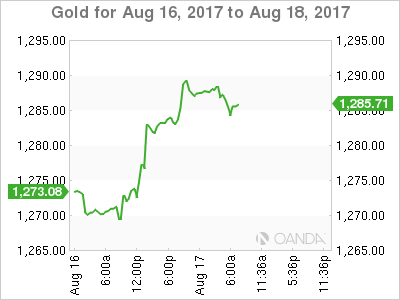

Gold has edged up on softer dollar. Spot gold is up +0.4% at +$1,287.90 per ounce, after gaining nearly +1% Wednesday.

3. Sovereign yields fall

U.S fed fund futures are now pricing in about a +40% chance that the Fed will raise rates by December, compared with just under +50% before release of yesterday’s Fed’s minutes.

The prospect of slower removal of stimulus is giving support to fixed income assets with Euro government bond and U.S Treasury yields heading lower.

The yield on U.S 10-year Treasuries fell -1 bps to +2.23%, while U.K 10-year Gilt yields dipped -2 bps to +1.087%. German 10-year Bund yields decreased -1 bps to +0.43%.

Note: The ECB may require more time and data before hinting at tapering its asset purchase program; therefore anyone who is hoping for more clarity in this morning’s ECB’s minutes (07:30 am EDT) could be disappointed.

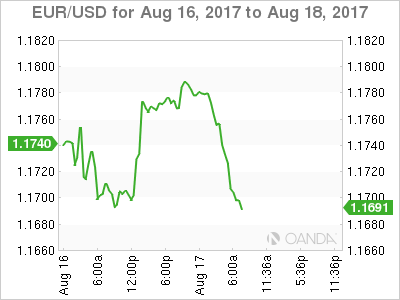

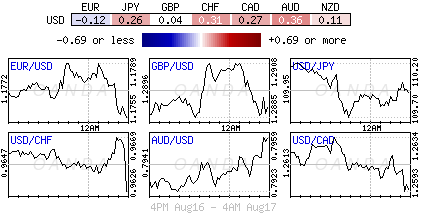

4. Dollar takes it on the chin

Along with yesterday’s Fed minutes, the ‘mighty’ dollar has also come under domestic political pressure when President Trump decided to disband two business councils after a number of members quit in protest over his comments on white nationalists.

Sterling (£1.2887) is trying to halt a five-day decline outright and against the EUR (€0.9100) after retail sales data (see below) beat expectations.

The EUR (€1.1721) is a tad lower, -0.45% ahead of the ECB release of its July minutes. The market is looking for more clarity, however, smart money would suggest that the ECB would not unveil any strategy for tapering, or when it is likely to make an announcement on its plan. EUR bears believe the single unit could possible test the €1.15 region if the ECB shows any signs of caution.

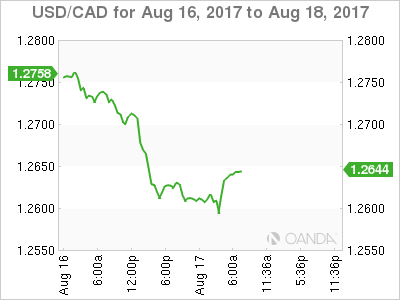

The loonie (C$1.2641) ended a brief losing streak outright yesterday as traders interpreted the latest minutes from the Fed’s July meeting as ‘dovish.’ The CAD is likely to see some volatility following the release of domestic manufacturing data this morning (08:30 am EDT) and any Nafta headlines.

5. U.K retail sales up modestly in July, Eurozone’s trade surplus widens

U.K retail sales rose modestly last month, with sales at food stores and household goods stores offsetting weakness elsewhere.

Sales rose +0.3% m/m and matched the monthly increase in sales seen in June. Sales were +1.3% higher on the year.

The figures point to continued spending by U.K consumers, albeit subdued, t the start of Q3 despite weak wage growth and rising prices.

Note: The U.K consumer requires some help and reason why business investment and exports will need to pick up to sustain growth this year and next.

Other data showed the eurozone’s trade surplus widened to a seasonally adjusted +€22.3B in June from €19B in May as exports fell less sharply than imports.

That suggests that while the EUR’s recent appreciation may be making life more difficult for eurozone’s exporters, the weakness of imports means that has not yet lowered economic growth.

Author

Dean Popplewell

MarketPulse