US Dollar Weekly Forecast: Trade developments remain at centre stage

- The US Dollar Index advanced to three-month highs this week.

- The Federal Reserve kept its interest rates unchanged as estimated.

- Expectations of a potential rate reduction in September intensified.

The week that was

The US Dollar (USD) regained balance this week, setting aside the previous week’s losses and sending the US Dollar Index (DXY) back above the psychological 100.00 hurdle for the first time since late May.

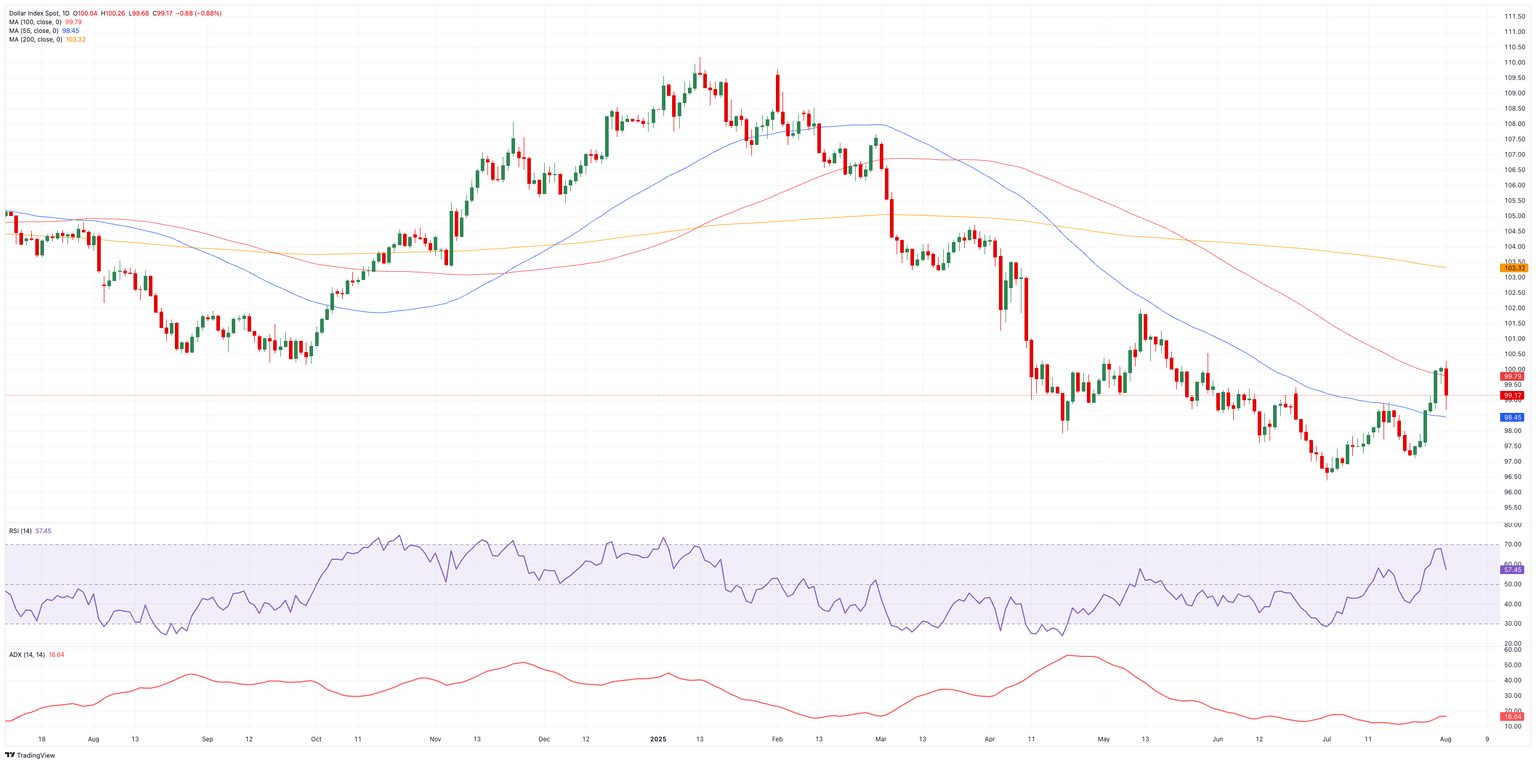

On the monthly chart, the index concluded July with marked gains, making a U-turn after five consecutive retracements. So far, DXY appears to have met quite a decent contention zone around the 96.40 region, its multi-year valley recorded on July 1.

For some weeks now, geopolitical tensions have somewhat subsided, enabling the trade narrative to once again take the lead, largely driving both sentiment and price action.

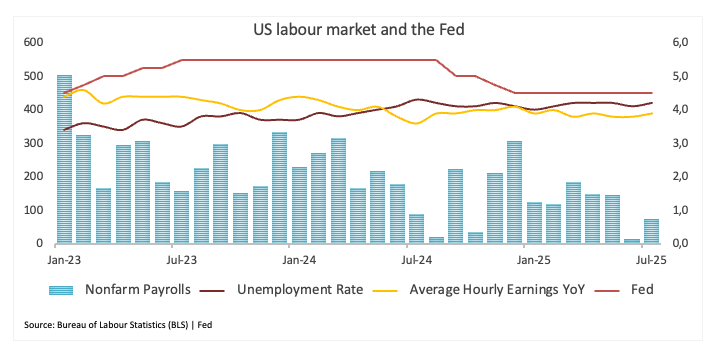

Contrary to previous data, the US calendar did not appear to support the Greenback this week, with results from the key labour market report primarily pointing toward further cooling.

A glance at the money market saw yields halting their gradual advance on the short end of the curve while intensifying their decline on the belly and end.

Hope trade deals dim ahead of the August 7 deadline

The Trump administration is once again ramping up trade tensions, announcing a fresh wave of tariff hikes that has triggered concern among major trading partners. Canada and Brazil were singled out for the sharpest increases, with tariffs on Canadian goods jumping from 25% to 35%, and Brazil’s rate rising to 50%. The White House justified the move by accusing Canada of “continued inaction and retaliation” in response to US trade policy.

Furthermore, a universal 10% tariff remains in place for countries running a trade surplus with the US. But under the revised framework, around 40 countries with trade deficits will face duties starting at 15%. The new measures are expected to take effect on August 7, allowing US Customs time to adjust enforcement protocols and collection systems.

Still around tariffs, US trade relations with Europe are under strain. The recently announced US-EU trade agreement is drawing criticism across the old continent, with France condemning the deal outright and German Chancellor Merz warning of its negative impact on exporters and economic growth. While the agreement was billed as a breakthrough, the markets reacted cautiously, recognising that it offered little near-term support for Eurozone prospects.

Meanwhile, hopes for stability in US-China trade relations received a modest boost. Senior officials from both sides held over five hours of talks in Stockholm on Monday, resulting in a tentative agreement to extend their 90-day tariff truce — pending final approval from President Trump. Officials described the discussions as “constructive,” though details remain limited.

Taken together, the week’s developments suggest a widening gulf between US trade policy and its global partners, with growing economic and diplomatic consequences on multiple fronts.

Tariffs: A costly cure for a deep trade imbalance?

Tariffs may still be a popular choice in Washington, but the long-term effects might be worse than the short-term political gains they provide. For now, consumers may be able to avoid big price increases, but if trade restrictions stay in place, the impacts might be seen in daily life: prices would go up in important areas, family budgets would grow tighter, and the economy would slow down overall.

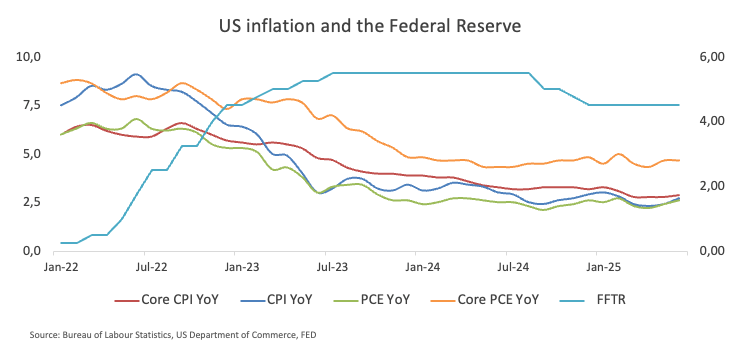

If inflation begins to rise again, that type of slow growth might make things hard for the Federal Reserve (Fed).

There are signals that the government is secretly leaning toward a lower US currency. This may boost exporters in a move to close the trade imbalance.

The attempt to bring manufacturing back home is a big goal, but it won't happen quickly. It will take time, a lot of money, and some changes to tariff policy to rebuild America's manufacturing foundation.

Tariffs could be part of the strategy in the end, but they aren't the answer to everything.

Fed mandate vs. data

The Federal Reserve (Fed) kept interest rates unchanged on Wednesday, opting for caution in a split decision that offered little clarity on when — or if — borrowing costs might come down. The benchmark rate remains at 4.25% to 4.50% for the fifth straight meeting, as policymakers navigate the delicate balance between inflation risks and a cooling economy.

“The unemployment rate remains low, and labour market conditions remain solid. Inflation remains somewhat elevated,” the Fed said in its post-meeting statement.

However, not all members of the committee were in agreement. Two members — Vice Chairperson for Supervision Michelle Bowman and Governor Christopher Waller — broke ranks, favouring an immediate quarter-point rate cut. Both were appointed by former President Donald Trump and have echoed his view that interest rates remain too restrictive.

Waller, in particular, has drawn attention as a potential successor to Fed Chair Jerome Powell, whose term ends next May. His dissent, alongside Bowman’s, signals growing pressure within the Fed to loosen policy despite the central bank’s cautious tone.

At his usual post-decision press conference on Wednesday, Fed Chair Jerome Powell said the labour market remained strong and was effectively at full employment, suggesting that part of the central bank’s dual mandate was being fulfilled. However, he noted that inflation was still running above target and the outlook remained uncertain — partly due to the effects of tariffs — meaning the Fed had yet to meet its inflation objective. Given those conditions, Powell said it was appropriate for policy to remain “modestly” restrictive.

Back to US fundamentals, the firmer-than-expected flash Q2 GDP readings were not enough to offset a modest uptick in weekly claims, let alone mask the disheartening Nonfarm Payrolls data released on Friday. The US economy missed consensus big time after adding 73K jobs in July, while June’s revised print showed a meagre 14K job creation (revised from 147K). Still, inflation, this time tracked by the Personal Consumption Expenditures (PCE), ticked higher in July.

It seems that, taken together, a potential rate cut by the Fed at its September meeting could still materialise.

What’s next for the US Dollar?

Next week’s lack of salient data releases should leave trade developments at the centre of the debate, with President Trump’s new August 7 deadline in the spotlight.

That said, investors will then closely follow the ISM Services PMI alongside the usual weekly claims and occasional remarks by Fed officials.

What about techs?

A break below the multi-year low of 96.37 (July 1) could pave the way for a move toward the February 2022 floor at 95.13 (February 4), followed by the 2022 base at 94.62 (January 14).

On the upside, initial resistance is seen at the weekly peak of 100.25 (August 1). A clear move above that level could lead to the weekly top of 100.54 (May 29), prior to the May ceiling at 101.97 (May 12).

For now, DXY is expected to stay under pressure while it remains below both the 200-day and 200-week SMAs, currently at 103.30 and 103.09, respectively.

Momentum indicators point to a loss of impulse in the recent uptrend. The Relative Strength Index (RSI) has deflated to nearly 55, while the Average Directional Index (ADX) remains around 16, signalling weak trend momentum.

US Dollar Index (DXY) daily chart

All in all

The US Dollar’s recent slide seems to have taken a breather — for now.

But even with the occasional show of strength, the Greenback still looks weighed down by growing uncertainty in Washington. Trade policy remains unpredictable, and concerns are mounting over the ballooning federal budget, especially now that Trump’s headline-grabbing “Big and Beautiful Bill” is on the books.

The Fed isn’t rushing to cut rates again, but its decisions are tightly bound to the data. That means any policy shift could just as easily offer a brief lift as another setback for the currency.

With no major positive catalyst on the radar, there’s little reason to expect a strong US Dollar comeback anytime soon. Given the ongoing trade deficit, political incentives may favour maintaining a weaker currency, which could benefit exporters and alleviate America's trade imbalance.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.