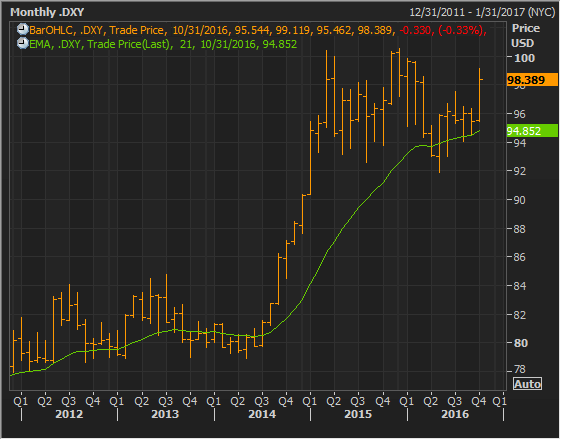

US dollar index hits fresh 8-month peak; brings it within reach of a 13-year high

The US dollar index reached its highest since early February on Tuesday at 99.11. From its August low of 94, the dollar index has therefore rallied more than 5%. The US dollar is now tantalizingly close to the 100.51 high of December 2015. If it manages to overcome this level, it would be a fresh 13-year high for the greenback. Such a development would certainly be a major event for foreign exchange markets in 2016. It would also mark a huge turnaround from the financial crisis lows of 2008 around 70-71 for the US dollar; a more than 40% rally.

The two recent attempts to scale the 100 level in the dollar index took place during the first and fourth quarters of 2015. Will it be third time lucky this time round? It is certainly possible, but unfortunately it looks like the current rally has already discounted most of the positives and the dollar could have a tough time breaking through to fresh highs above 100.51.

Firstly, in less than 2 weeks the US Presidential Election takes place. Financial markets seem to be positioned for a victory by Hillary Clinton which is seen as reducing economic and political uncertainty and easing the path for a December rate hike by the Fed. As this seems to be the main scenario, it is hard to envision the US dollar rallying hard because of a Clinton win. On the other hand, it would be a mistake at this stage to dismiss the chances of Donald Trump, whose possible victory could lead to some volatility and could hurt the US dollar by making the December rate hike less probable. The recent example of Brexit also showed markets expecting a victory by “remain” only to be shocked when “leave” won the referendum. Therefore, market predictions about political events can prove spectacularly wrong sometimes, as Brexit recently showed. To summarize this point, Clinton’s expected win might not boost the US dollar by much whereas a Trump victory could lead to more serious profit-taking by dollar longs.

The other point is the expected Fed rate hike in December. Right now markets are attaching a probability between 70 and 80% on a Fed rate hike. It is generally accepted by economists and analysts that plain sailing by the US economy in the next month-and-a-half will almost surely lead to a rate hike. So the first source of uncertainty that could lead to disappointment is something negative happening in this period. In the past it hasn’t taken much to shake the Fed off its tightening path; a poor employment report or a sudden dip in business confidence surveys or some global event. Given that Chair Fed Yellen does not sound 100% convinced that a rate hike is needed, she could also convince other committee participants - mainly the Board of Governors and not the more hawkish Regional Fed Presidents - to stand pat.

The second point of uncertainty with respect to the Fed is the future path of interest rates. If the Fed says that a quarter point hike to 0.50-0.75% is of the ‘one and done’ variety, this could also have a negative impact on the dollar. The message from various Fed officials is that the level at which they see rates plateauing has come down in the past 1-2 years. Therefore, if the rate hike in December is accompanied by dovish rate guidance, this could again hurt the prospects of more gains by the US dollar.

In conclusion, while overall sentiment seems to be favoring additional gains by the US dollar, it remains to be seen whether the dollar index will have enough strength go on and take out its 13-year high. The US dollar rally may have discounted the good news that could happen in the next 2 months like a Clinton win and a Fed December rate hike and will probably need fresh catalysts to push it significantly higher. In their absence, there could be some consolidation in the dollar’s uptrend.

Author

Manned by a powerful team of professionals, along with certified forex instructors, the XM Research and Education Center provides a full range of up-to-date marketing tools essential for profitable trading, including market analys