US Dollar: Excessive weakness or more to come?

Key points

-

Recent Dollar weakness: The US Dollar Index has slipped to year-to-date lows below 102, driven by shifting market expectations on the Fed's interest rate path and concerns about the U.S. economic outlook.

-

The why: Markets anticipate a dovish stance from Fed Chair Jerome Powell at Jackson Hole, with expectations of an accommodative monetary policy. Additionally, political shifts, such as Harris gaining ground in polls and the unwinding of "Trump Trades," are contributing to the dollar's weakness.

-

Key catalysts: Fed Chair Powell’s speech at Jackson Hole remains on watch to assess how he balances the two sides of the Fed’s mandate. More importantly, revisions to US payrolls for the year ending March 2024 could send a warning signal on the strength of the US labor market last year and bring more downside for the USD.

-

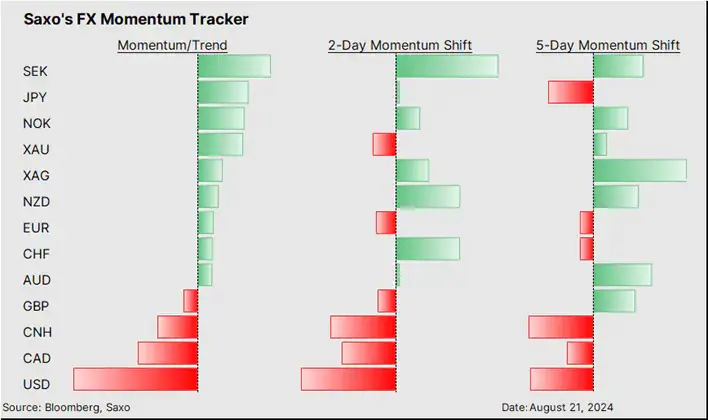

Potential for a short-term rebound: The dollar’s recent weakness might be overdone, with potential for a rebound if market expectations for Fed rate cuts prove excessive. Yen strength needs a fresh trigger to extend after the positioning has turned to a net long, while CAD faces risks economic and oil price risks.

The U.S. dollar has seen a notable decline recently, with the Dollar Index (DXY) falling below 102, its lowest levels since December last year. This downturn is attributed to shifting market expectations regarding the Federal Reserve's interest rate path and broader concerns about the U.S. economic outlook, particularly in light of softer inflation data and signals of a cooling labor market.

Why is the Dollar weak?

Let’s go back to the fundamentals of the “Dollar Smile” theory. This theory suggests that the USD performs well when the U.S. economy is either very strong and yields are going higher in anticipation of rate hikes from the Fed, or very weak with recession concerns fuelling risk aversion and haven flows into the USD. None of these two scenarios are the market’s base case as of now. The U.S. economy is rather expected to achieve a soft landing, where growth slows but a crisis is avoided, and this lands the USD in the middle of the Dollar Smile, resulting in weakness.

Another factor contributing to the dollar's weakness is Harris gaining ground in the polls, which is leading to the unwinding of "Trump Trades" that were put in place after the chaotic June TV debate between Biden and Trump.

Additionally, markets are positioning for a dovish message from Fed Chair Jerome Powell at the upcoming Jackson Hole Symposium, expecting him to emphasize the need for a more accommodative monetary stance. This expectation has led to increased selling pressure on the USD as traders anticipate a potential shift in the Fed's policy direction.

Jackson Hole: Powell’s dovishness is well priced in

At Jackson Hole, Powell is expected to focus on the effectiveness of current monetary policy, particularly in relation to the Fed's dual mandate of stable prices and maximum employment. He may acknowledge that the current monetary policy stance is quite restrictive, especially given the recent data indicating softer inflation and a cooling labor market. However, Powell is unlikely to put a 50bps rate cut on the table immediately, as doing so could disrupt the recent calm in financial markets.

Instead, he is likely to emphasize a balanced approach, cautioning against overreacting to any single data point and stressing the importance of considering the broader economic picture. After all, the August jobs report on September 6 and the CPI on September 11 will still be key indicators for the Fed’s next moves.

Jobs revisions: Renewed US Labor market concerns?

The Bureau of Labor Statistics (BLS) is expected to revise its employment data for April 2023 to March 2024. Some reports suggest that U.S. job numbers may have been overstated by around 600,000 to 1 million in the year ending in March 2024. Such an outcome could mean that the strength of the labor market during that period has been overstated, and could reignited concerns around a weaker employment picture. This is something that Chair Powell may need to address as well, and if the upcoming jobs report on September 6 shows significant weakness, it could bolster the case for a 50bps rate cut by the Federal Reserve, potentially leading to further USD weakness.

If USD gains, what gives?

The dollar's recent weakness might appear excessive considering the current US macro backdrop, especially if market expectations for aggressive Fed cuts are overdone.

That raises the question about what gives if the US dollar gains from here. Below are some considerations:

JPY: The Japanese yen (JPY) has strengthened following a BOJ research paper that discussed rate hikes. However, it is worth noting that the paper covers discussions from May, possibly justifying past decisions rather than signalling new ones. Meanwhile, yen shorts have been cleared out as indicated by the latest CFTC COT report, and the currency would need a strong recession trigger to attract new longs given the carry is so overbearingly negative to go long yen.

EUR: The euro (EUR) has seen substantial gains with EURUSD rising to YTD highs of 1.11+. However, recession concerns in the Eurozone are likely more substantial than the US, and the ECB rate cut cycle is unlikely to be any less aggressive than that of the Fed. Other headwinds for EUR stem from a sluggish China economy and the upcoming US elections.

CAD: The Canadian dollar (CAD) faces downside risks, such as the impact of fluctuating oil prices and the potential for a large M&A deal between Couche-Tard and 7-Eleven, which could introduce significant FX risk. The potential for a rail worker strike in Canada adds another layer of downside risk to the CAD.

In conclusion, while there is a case for continued USD weakness, it is crucial to monitor key data releases and Fed communications. The US dollar's weakness might be more about over-optimism regarding other currencies than an actual deterioration in the U.S. economic outlook. The market may have priced in too much dovishness from the Fed, leaving room for a potential rebound in the dollar if the economic data or Fed commentary surprises to the upside.

Read the original analysis: US Dollar: Excessive weakness or more to come?

Author

Saxo Research Team

Saxo Bank

Saxo is an award-winning investment firm trusted by 1,200,000+ clients worldwide. Saxo provides the leading online trading platform connecting investors and traders to global financial markets.