US Dec ISM Manufacturing PMI Preview: Encouraging sub-indices could temporarily boost US Dollar

- The US ISM Manufacturing PMI is seen dropping further to 48.5 in December.

- A potential improvement in US ISM components could drive the US Dollar trades.

- Moves could be restricted ahead of the Federal Reserve December meeting minutes.

The US manufacturing sector contraction is set to deepen further in the final month of 2022, having shrunk for the first time in November after May 2020 when the economy began to recover from the Covid lockdown-induced downturn. The US data will be published on Wednesday at 15:00 GMT.

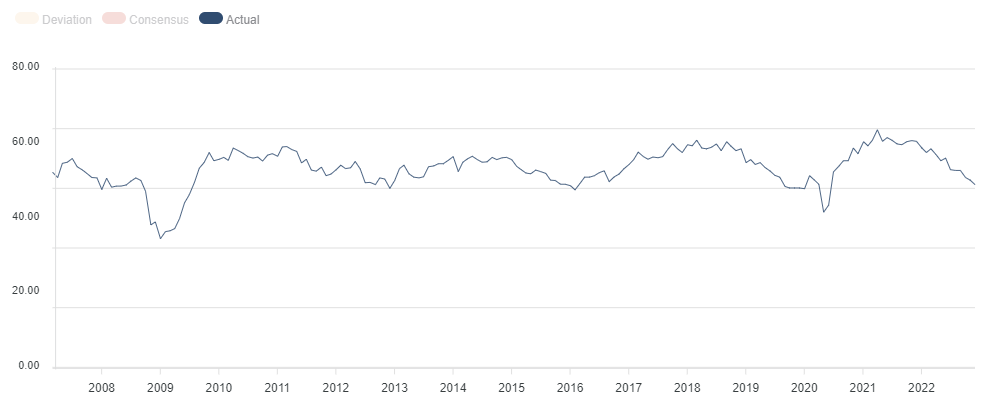

The November ISM report showed that manufacturing registered an overall 49.0, down sharply from October’s 50.2, with New Orders and Employment sub-indices registering further deterioration.

In December, the headline ISM Manufacturing PMI is seen lower at 48.5 while the New Orders Index is expected to improve to 48.1 alongside the Employment Index at 49.1. The US ISM Prices Paid component is likely to continue its downtrend, foreseen at 42.5 in December when compared to the previous reading of 43.0.

Source: FXStreet.com

Despite expectations of a softer headline figure, an improvement in new orders could provide the much-needed respite to the US Dollar buyers at a time when the European demand for orders is seen dwindling, with the full impact of winter and the Russia-Ukraine war coming through. Even domestic demand and exports are expected to be badly hit due to the stubbornly-high inflation in the US economy.

The US labor market continues to show an uptrend but remains at risk of layoffs, with the global economy heading closer to a recession this year. However, the temporary signs of recovery in the sub-indices could revive the demand for the US Dollar. However, the US Dollar price reaction could be short-lived amid the extended retreat in the Price Paid component, suggesting a further easing of inflationary pressures in the world’s largest economy.

Also, investors will gear up for the US Federal Reserve December meeting minutes due for release at 19:00 GMT, limiting the US Dollar price action on the US ISM data release. Minutes of the Fed’s December meeting are likely to show that members see the need for interest rates to go higher for longer but markets will look for hints on any talk of pausing the tightening cycle or debates surrounding rate cuts later this year. It’s worth noting that markets are pricing in rate cuts for late 2023, with Fed fund futures implying a range of 4.25 to 4.50% by December.

To conclude, mixed US ISM Manufacturing survey findings could fuel temporary buying in the US Dollar, which could fizzle out as the Fed expectations will lead the way starting out 2023.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.