US CPI Preview: Upside surprises likely to boost US Dollar sharply

- The July Consumer Price Index is expected to show more evidence of softening inflation, despite a rebound in the annual rate.

- The annual inflation rate is seen advancing from 3% to 3.3%.

- The US Dollar is set to rally if the numbers surprise to the upside.

The US is scheduled to release the Consumer Price Index (CPI) for July on Thursday, August 10 at 12:30 GMT. This report is expected to be the most significant economic release of the week. Additionally, the weekly Jobless Claims report will be published simultaneously. Furthermore, more inflation data will be available on Friday with the release of the Producer Price Index (PPI).

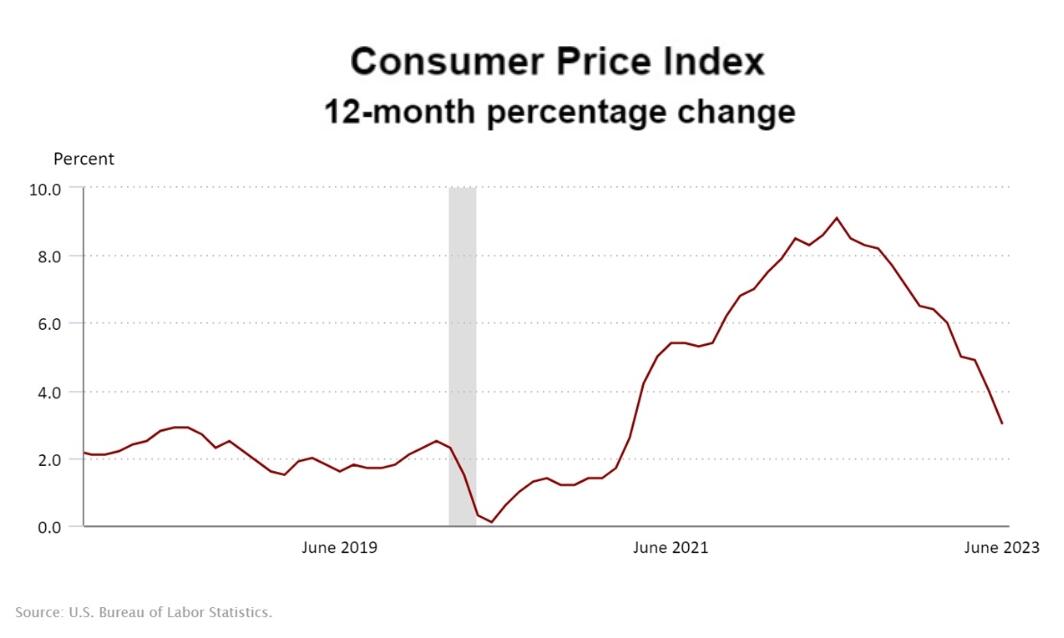

The market consensus is for the CPI to have risen 0.2% in July, with the annual rate increasing from 3% in June (the lowest since March 2021) to 3.3%. This would mark the first increase in the annual rate since June 2022, when it peaked at 9.1%, the highest in 40 years.

Equally important is the Core CPI, which is expected to increase by 0.2% on a monthly basis. The annual Core CPI rate is anticipated to remain at 4.8%.

Numbers above expectations will indicate that the recent deflationary trend is starting to face difficulties, and concerns about persistent inflation may resurface. Conversely, if the figures align with estimates, it could suggest that inflation pressures are normalizing. In both scenarios, inflation would remain below the 2022 peak but above the Federal Reserve's 2% target.

Turn for the data to speak

Last week, the Fed raised its key interest rate by 25 basis points. The market expected this to be the last hike of the cycle. For that expectation to materialize, the first requirement is for inflation to continue declining. Therefore, the upcoming CPI number will be crucial.

If the figure shows that inflation remains above expectations or rises more than anticipated, the likelihood of another rate hike before year-end will significantly increase. Despite Fed’s tightening, the US economy has demonstrated resilience. During the second quarter, GDP grew at a 2.4% annualized rate, surpassing the estimated 2%. Labor data indicates a softer labor market, but job creation persists and provides little evidence of a recession. Payroll numbers are decreasing to normal levels, while wage growth exceeded expectations in July.

A few months ago, analysts were concerned about the possibility of a US recession.

However, the current forecast indicates a shift towards a successful soft landing. Lower inflation readings would further bolster this outlook, and would be favorably received by the Fed. Such figures would enable the central bank to maintain its current stance and take time to evaluate the effects of its measures.

Before the next FOMC meeting, there will be additional inflation reports, including the August CPI. Therefore, there is still a long way to go. One other factor to consider is Crude Oil. The price of WTI Crude Oil has reached its highest level since November 2022, surpassing $83.00 per barrel after rising 15% over the past 45 days. If the rally continues, it could add pressure to energy prices and push up CPI in general.

How could the Dollar react?

The US Dollar awaits the upcoming data looking strong, primarily supported by the latest round of US economic data, particularly indicators related to growth and employment. Suppose the CPI surpasses expectations by a significant margin. In that case, a sharp rally in the US Dollar is likely to occur, as it would increase the probability of another rate hike by the Fed. In such a scenario, the stock market could experience a decline, while US yields would rise, providing additional momentum to the USD.

If the data aligns with expectations, the US Dollar could experience a decline, considering the positioning leading up to the report. Even if it meets estimates, volatility is likely to rise along with trading volume.

Another possibility is that the annual CPI rate slows unexpectedly. Such a scenario would increase the likelihood that the Fed has concluded its tightening cycle. While this could harm the Dollar in terms of interest rates and bond yields, the decline may be limited as it could be viewed as a positive development for the US economy. In this case, it could trigger a rally in Wall Street, thereby restraining the demand for the Dollar.

DXY’s rally needs fuel

The US Dollar Index (DXY) has been moving upward since mid-July, recovering from its lowest levels in over a year, and the short-term bias remains to the upside. However, the DXY remains within a downward channel.

During the upward move, the DXY encountered resistance below the 103.00 area and around the 55-day and 100-day Simple Moving Averages (SMAs). If the DXY manages to break above this resistance, it would likely continue its ascent and test the 200-day SMA at 103.45, followed by the upper trendline of the downward channel at 103.75.

On the other hand, a key support level lies at 101.90. Below this support, it could expose the 20-day SMA at 101.35. If consolidation continues below this level, it would confirm the continuation of the downward channel, potentially exposing the next support at 100.90.

DXY Daily chart

-638271842334811654.png)

Author

Matías Salord

FXStreet

Matías started in financial markets in 2008, after graduating in Economics. He was trained in chart analysis and then became an educator. He also studied Journalism. He started writing analyses for specialized websites before joining FXStreet.