US CPI Preview: Inflation remains secondary to Fed policy

- Annual core and headline CPI stable in October.

- Federal Reserve rate pause does not reference inflation.

- Core CPI has averaged 2.17% through September this year.

The Bureau of Labor Statistics will release its consumer price index (CPI) for October on Wednesday November 13th at 1:30 GMT, 8:30 EST.

Forecast

The consumer price index is predicted to rise 0.3% in October after being unchanged in September. Annual inflation is expected to increase 1.7% last month as in September. Core inflation is projected to increase 0.2% in October and 2.4% on the year as in September.

US Inflation: CPI, PCE

Ove the past three years US inflation has been largely without trend.

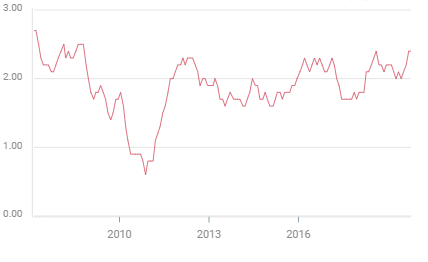

From January 2017 through September 2019 core annual CPI has averaged 2.039% with a range of 1.7% to 2.4%. In January 2017 the rate was 2.3% in September 2019 2.4%.

Core CPI

Overall CPI has averaged 2.133% in those 33 months with a range of 0.8% to 2.9%. In January 2017 the rate was 2.5% in September 2019 it was 1.7%.

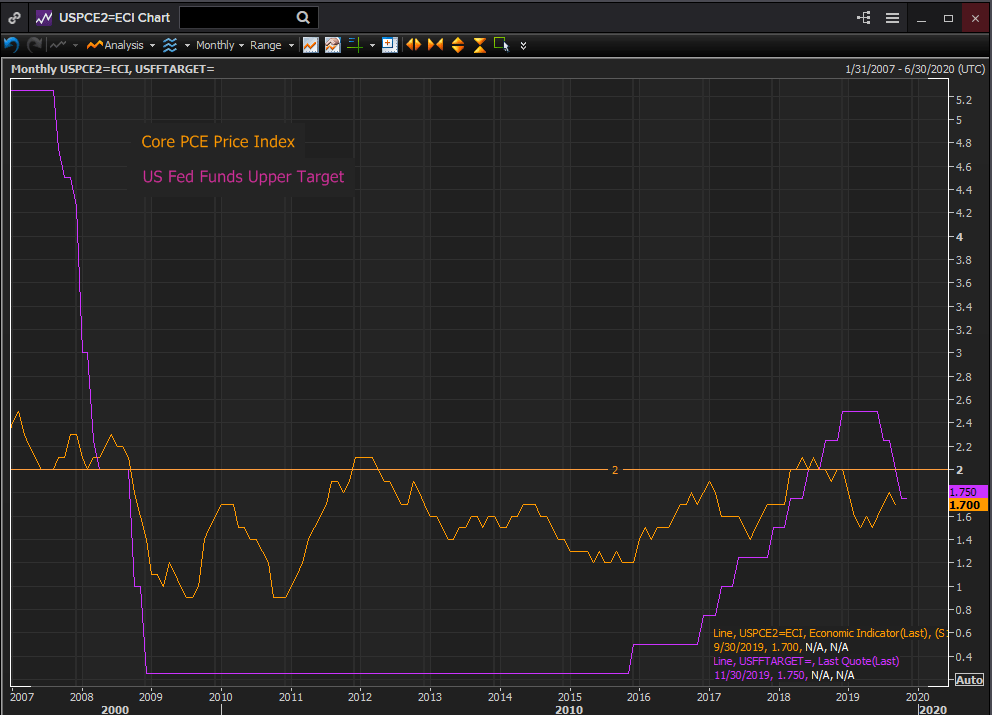

The personal consumption expenditure price index (PCE) has averaged 1.785% since January 2017, with a range from 1.3% to 2.5%. In January 2017 it was 2.0%, in September 2019 1.3%.

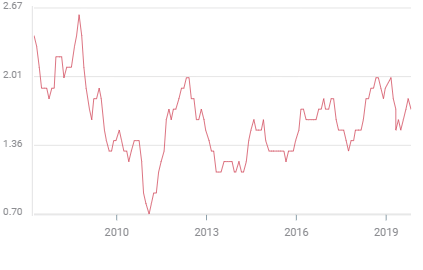

The core PCE price index, the Federal Reserve’s chosen measure, has averaged 1.752% with a range of 1.4% to 2.2%. In January 2017 the core PCE rate was 1.9% in September it was 1.7%.

Core PCE

FXStreet

Over the 33 month period from January 2017 to this September the variation in the annual core inflation rates has been negligible. In the older gauge it was 2.3% in the beginning of 2017 and 2.4% in September 2019. For the Fed’s preferred gauge the change was just 0.2% from 1.9% to 1.7%.

Inflation and Federal Reserve Policy

Consumer price inflation in the United States over the past few years has received much attention and little action from the Federal Reserve.

Inflation is mentioned in each FOMC statement, usually in the context of returning to the symmetric 2% target sometime in the future.

This quote from the October 30th meeting could stand in for almost any FOMC statement in the last three years. “This action supports the Committee’s view that sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective are the most likely outcomes, but uncertainties about this outlook remain.”

Throughout the last decade the Fed’s overriding concern has been economic growth. Under Chairman Jerome Powell that has become more specific, defending the economic expansion and its labor market benefits against external threats.

The logic behind lopping 0.75% from the fed funds rate this year was to take out an “insurance policy’ against the trade and global growth problems that might derail US growth. The domestic economic conditions that in the past had triggered a central bank supporting cycle were absent. This was acknowledged by the Fed as its justification shifted to its maximum sustainable employment mandate from price stability.

Inflation’s role in Fed policy has been a poor rhetorical cousin, paraded on the stage but never given a speaking part. Interest rate policy, whether in the long period of zero from late 2008 through the end of 2015, in the ascent to 2.5% or from December 2018 until now has proceeded regardless of the level of inflation.

Reuters

There is little doubt that had inflation moved higher, as many in the economic community had expected after the various rounds of QE, the Fed’s hard choice between promoting the recovery and reining inflation would have come down on the side of economic growth.

It has been fortunate, and a modest surprise, that inflation has remained quiescent for a decade. The pressures on Fed policy would have been considerably more difficult had prices moved noticeably higher.

With the Fed on hold through at least the end of the year, inflation’s impact on policy is remains minimal.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.