US CPI Preview: Higher is better

- CPI, core and headline, expected to rise in April

- Powell noted low inflation in his March press conference

- Core PCE has declined for three months

The Bureau of labor Statistics will release the April consumer price index on Friday May 10th at 8:30 am EDT, 12:30 pm GMT.

Forecast

Core inflation is expected to rise 0.2% in April following March's 0.1% gain. Annual core inflation is projected reach 2.1% from 2.0% prior. Overall inflation will be unchanged at 0.4% in April with yearly CPI rising to 2.1% from 1.9% in March.

Inflation and the Federal Reserve

The Fed’s March Projection Materials estimated that the core Personal Consumption Expenditure (PCE) price index, its preferred measure, would be 2.0% for 2019. In the first quarter actual core PCE price changes measured 1.7%. The projection for overall PCE inflation had been reduced to 1.8% in March from 1.9% in December. First quarter PCE prices were 1.4%.

More important than the level for Fed policy has been the direction, core PCE inflation has fallen 0.4% in three months from 2% last December to 1.6% in March. The six months last year when this core measure was at the Fed target of 2% was the first time since early 2012 (2.1% 12/11-3/12) when inflation reached the bank’s limit and only the second time since the financial crisis.

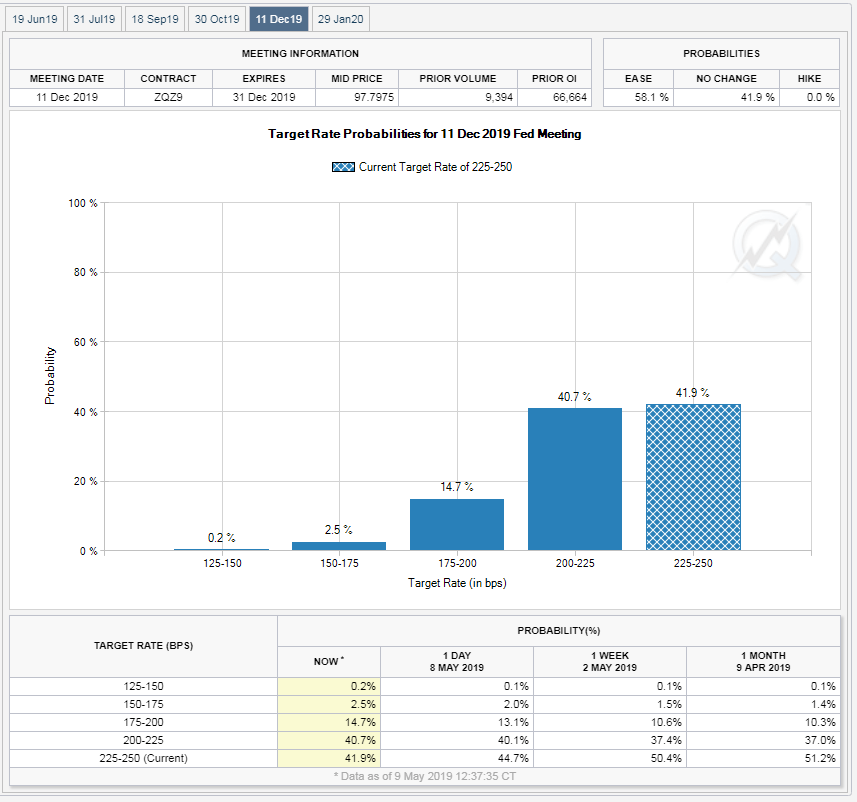

The adoption of a neutral rate policy that commenced in December after the FOMC hike to a 2.5% upper target has brought rate speculation full circle. The Fed Funds futures now (May 9th) score an equal chance for a rate cut by the December 11th meeting (40.7%) as for the current rate (41.9%), The balance (17.4%) plumps for an even lower Fed Funds by year end.

CME Group

Core PCE versus Core CPI

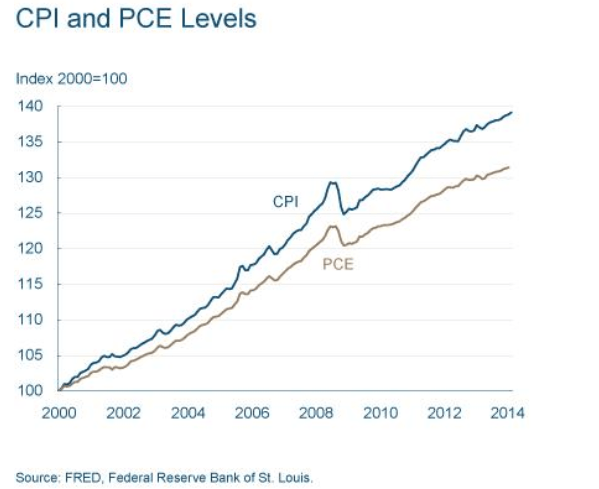

The Fed’s chosen inflation gauge, the core personal consumption expenditures price index, core PCE for short, is a modernized version of the venerable consumer price index, CPI.

The primary difference is in the composition of the basket of goods each index uses to calculate price changes. Different weights are given to different items in each basket. The CPI choices are based on what households are buying, the PCE uses what businesses are selling. The CPI also covers only out of pocket expenses, that is items and services directly purchased. It does not include for example medical care provide by employer insurance, Medicare and Medicaid. All of these are counted in the PCE.

The final major difference is that the PCE measure tries to account for goods substitution, when people lower purchases of one item because the price has gone up and choose another. If limes suddenly became more expensive and people started buying lower priced lemons, the PCE basket would count more lemons. The CPI keeps the basket items the same.

The differences between the two indexes generally results in higher CPI inflation. Since 2000 CPI prices have risen 39%, PCE 31% resulting in average annual inflation rates of 2.4% and 1.9%.

Inflation and the economy

When the Fed backed away from their tightening regime in December they noted several global threats to the US economy, Brexit, the US/China trade spat and the general slowing of growth. All three remain but the US economy expanded at a 3.2% annualized rate in the first quarter, much faster than the 2.0-2.5% expected by analysts.

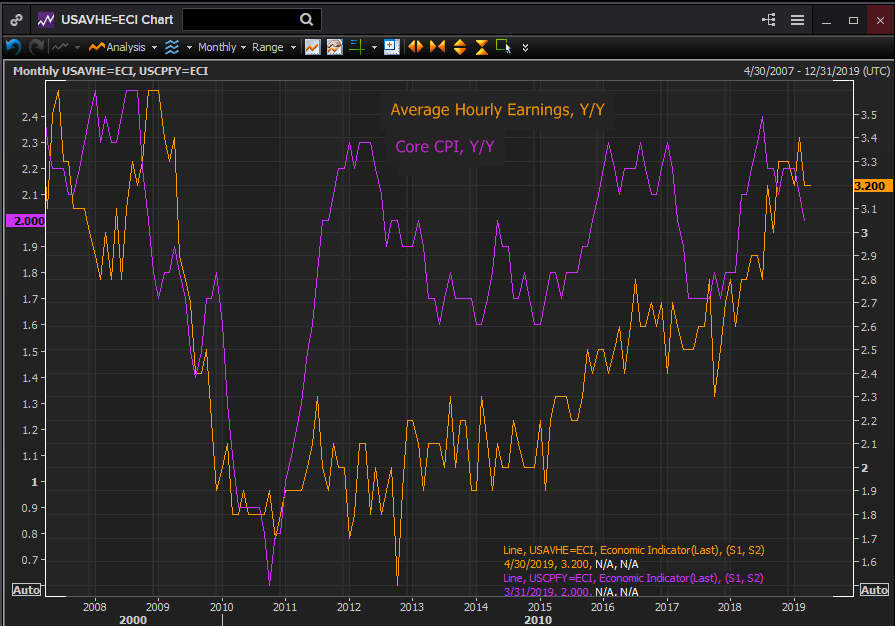

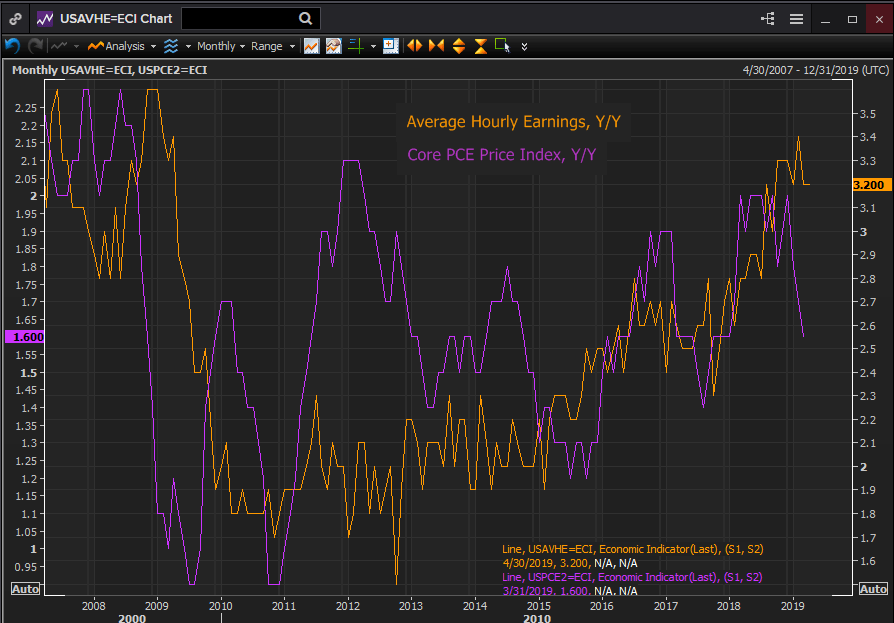

Payrolls added 263,000 workers in April 40% more than the median estimate. The unemployment rate fell to 3.6% a five decade low. Wages rose 3.2% completing their ninth straight month above 3%, the best performance in ten years.

The puzzle for the Fed is that while wages are rising, driven by a tight labor market, consumer prices are not.

Reuters

Fed Chairman Powell addressed this issue in his news conference after the May1st FOMC meeting. While stating that “We do not see a strong case for moving [rates] in either direction,” he acknowledged that “The weak inflation performance in the 1st quarter was not expected...some of it appears to be transitory or idiosyncratic."

The chairman said he expects that “Inflation will return to 2% over time and then will be symmetric around our target,” but that if it did not happen that would be a concern for the Fed.

Low inflation has been an issue for central banks around the world since the financial crisis. The Fed has long maintained, as evidenced in its projections, that inflation will attain its 2% target. However, the Fed’s inflation estimates over almost a decade, have consistently overstated the speed and the level of returning inflation.

Inflation and the dollar

The consumer price index market interest is as a predictor to the PCE. The expected rise in the core CPI rate to 2.1% from 2.0% in March or a stronger performance will reinforce expectations that PCE is set to rise as well. The April PCE figures will not be released until May 31st.

Chairman Powell was asked several times in his May news conference whether underperforming inflation could lead the Fed to consider cutting rates as a remedy. He refused to be drawn out on this point, saying only that the governors were unanimous in thinking that the current policy is appropriate. A rise in April CPI will help support that assertion.

The dollar remains supported by the better than expected performance of the US economy. An increase in inflation will help allay the notion, however slight, that the Fed’s next move will be a rate cut. The dollar will gain accordingly.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.