US CPI Preview: Heading to irrelevance?

- Core CPI expected to be stable in May, headline CPI to fall

- Expectations for a Fed rate cut not primarily related to inflation

- Core CPI has been at or above 2% for 14 months

The Bureau of Labor Statistics will issue the May consumer price index on Wednesday June 12th at 8:30 am EDT, 12:30 GMT.

Forecast

The consumer price index is expected to gain 0.1% in May after April’s 0.3 % increase. Yearly inflation will drop to 1.9% from 2%. Core CPI is predicted rise 0.2% in May up from April’s 0.1% addition. Annual core inflation is forecast to be unchanged at 2.1%.

Inflation and the Federal Reserve

The underperforming May payrolls have given another and stronger note to the inflation, equity and global growth chorus clamoring for a Federal Reserve rate cut.

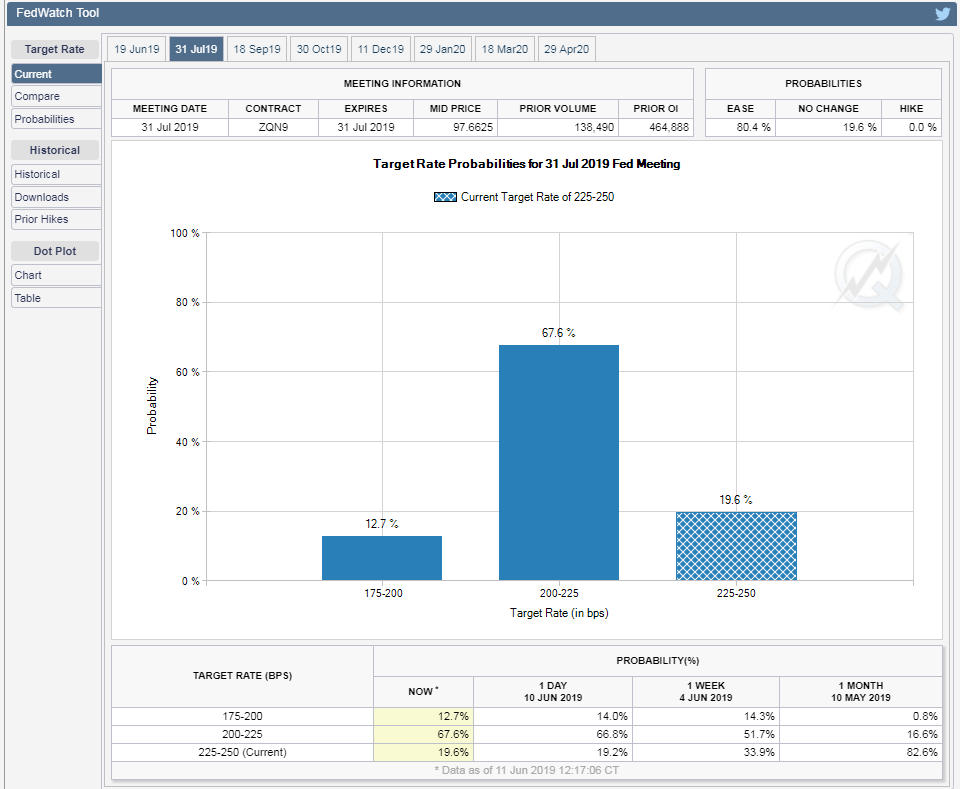

Expectations in the Fed Funds futures for a rate cut by the July 31st FOMC meeting were 80.3% as of this writing and for the December 19th meeting the last of the year, they are 98% for at least one decrease and the 83.3% for two or more.

CME Group

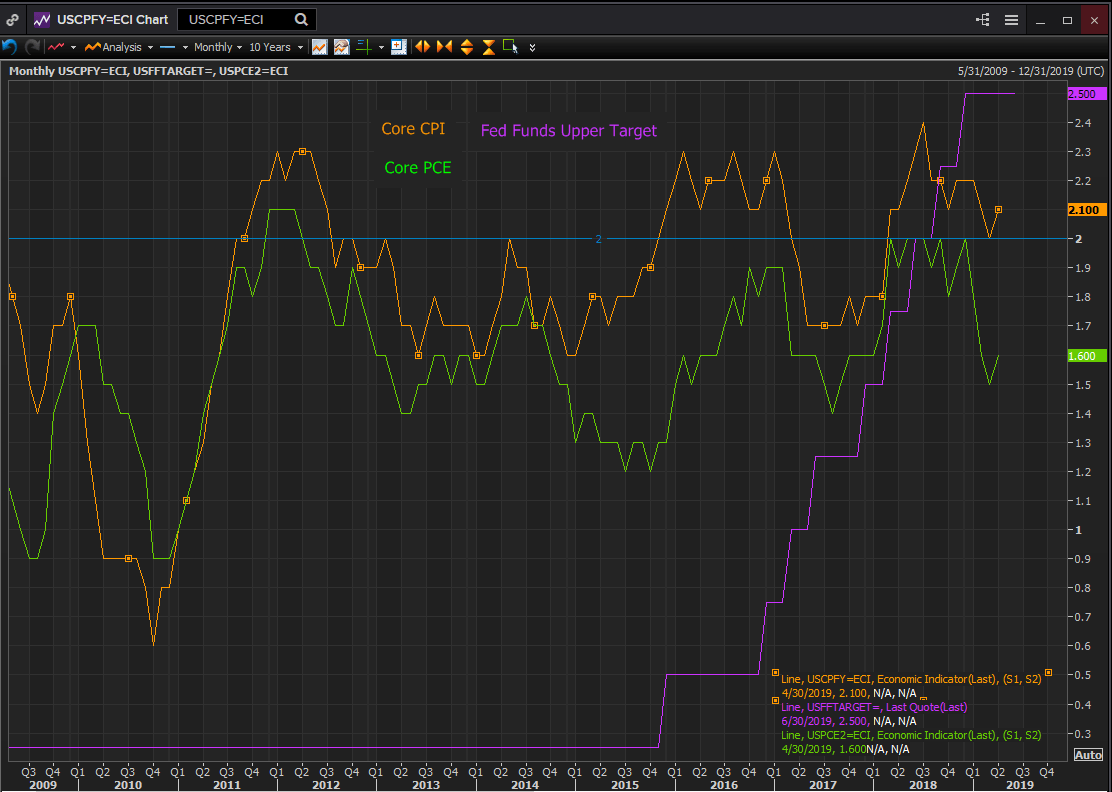

Inflation has not been the chief driver in this movement. It has been below the central bank’s 2% target for most of the last decade.

The Fed’s preferred personal consumption expenditure core price index was 1.3% at the FOMC’s first 0.25% post-recession hike in December 2015 to 0.5%. It did not reach 2% until April 2018 by which time the Fed funds target was 1.75%. It stayed between there and 1.8% as the Fed completed its course with three more increases to December 2018 and 2.5%.

Reuters

After the May 1st FOMC which came just after the core PCE rate for March registered 1.5%, down from 2% four months earlier, Chairman Powell said “We do not see a strong case for moving in either direction. He said “The weak inflation performance in the 1st quarter was not expected...some of it appears to be transitory or idiosyncratic,” in response to a question if low inflation might prompt a rate cut. He refused to speculate on whether inflation could lead to lower rates saying that the governors were united in considering the current policy appropriate.

Weak inflation has been a recurring global central bank problem since the financial crisis. The response from the Fed as from the ECB has been that inflation will return to 2% and will be symmetric around the target.

Federal Reserve, jobs and economic growth

Price stability is one of the Federal Reserve’s Congressional mandates, the other is maximum sustainable employment. Over the ten years since the end of the financial crisis recession inflation has not been the Fed’s chief concern. The focus has been economic growth and the job creation that attends it.

The rising tempo of economic growth and job creation since the election but particularly last year and into the first quarter let the Fed governors quicken the tightening pace. They increased rates four times in 2018, the first time the central bank has added a percentage point to the Fed Funds rate within 12 months since 2004 and 2005.

It was the threats to US economic growth, the trade dispute with China, the potential impact of Brexit and the general drop in global economic activity combined with the record length of the expansion that brought three years of rising rates to a standstill in December.

Economic growth in the second quarter seems to have slowed abruptly from the 3.1% annual pace in the first three months of the year. The Atlanta Fed GDPNow model is tracking at just 1.4% less than half the earlier pace.

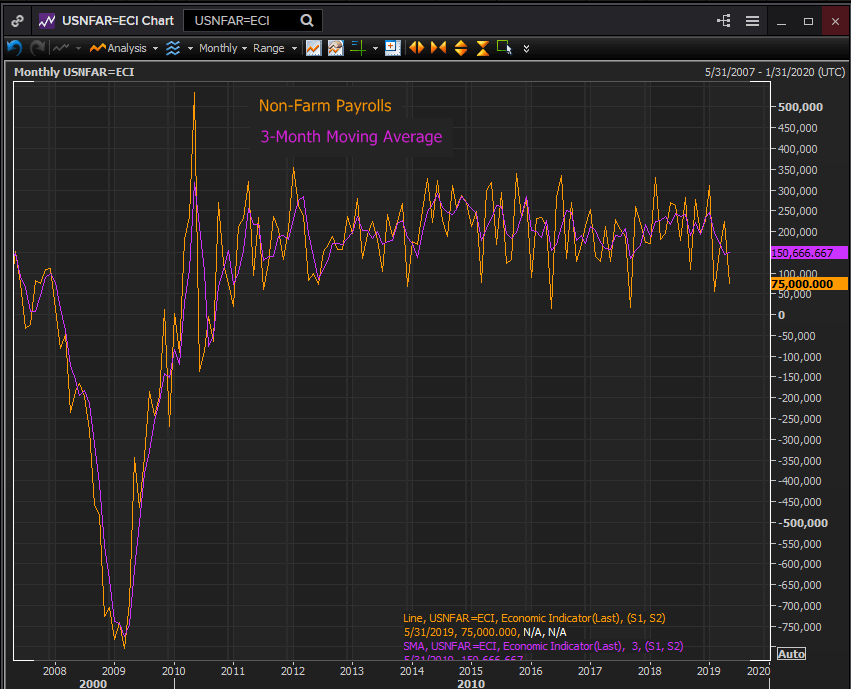

In the context of overall economic growth the May payrolls of 75,000, the second weak month in four, February saw 56,000, is of far greater concern to the governors than perennially underachieving inflation.

Reuters

The three month moving average for payrolls has fallen from 245,000 in January to 150,700 in May. Despite the near record lows in initial jobless claims and wage gains just 0.1% away from the best post-recession levels, the recent decline in payrolls has probably given the Fed as much concern as a decade of low inflation.

In response Chairman Powell said, “But what I do know is that we will be prepared to adjust policy quickly and flexibly and to use all of our tools to support the economy should that be appropriate to keep the expansion on track." That is a very different answer than the blasé reassurances about inflation repeated so often over the last decade.

Inflation, Fed policy and the dollar

The main market interest in the consumer price index is as a predictor to PCE. The expected stability in the core rate at 2.1% and the slight decline in the overall rate to 1.9% from 2% will augur for a similar PCE result when the May numbers are released on June 28th.

Fed policy and the tilt to a rate cut will not be affected if CPI comes in stronger than expected because the change in Fed policy to neutral was not arbitrated by low inflation but by perceived threats to the US expansion.

A weaker result will provide added rational for a rate cut because it is reinforcing the current policy inclination.

Likewise the dollar will not benefit from higher CPI but could well be damaged by a weaker than expected report.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.