US CPI Preview: Economic growth not prices is the key to Fed policy

- Core CPI expected to be unchanged, headline inflation forecasted to be higher.

- Inflation to have minimal impact on Fed rate policy.

- Fed focused on economic growth to decide on the expected rate cut.

The Bureau of Labor Statistics will issue its consumer price index (CPI) for September on Thursday October 10th at 12:30 GMT, 8:30 EDT.

Forecast

The consumer price index is projected to rise 0.1% in September as it did in August. Annual inflation is expected to be 1.8% following August’s 1.7% increase. The core rate is estimated to gain 0.2% after a 0.3% rise in August. The yearly CPI rate will be 2.4% in September as in August.

Inflation and monetary policy history

The Federal Reserve operates under two Congressional mandates. The first is to maintain ‘maximum employment.” The second is promote “price stability.”

September’s unemployment rate of 3.5%, down 0.2% on the month, the lowest in five decades and at or below 4% for 18 months admirably fulfills the first policy requirement.

The Fed’s second mandate, ‘price stability’ was instituted more than a generation ago when 10% and higher inflation, the residue of deficit spending on the Vietnam War, threatened to derail the US economy.

The success of Fed Chairman Paul Volker’s restrictive monetary policy in curtailing runaway inflation and the price target policies of subsequent Fed boards have made inflation a negligible economic consideration. Whether inflation is running at 1.5% or 2.3% its impact on economic growth is minimal.

Current Fed inflation policy seeks price changes that are symmetric around 2%, that is, they are as often above or below. When the variations in inflation rates are consistently within 0.5% of the target rate policy monetary policy is at its practical limit.

The Fed has noted this by repeatedly focusing on long term inflation expectations. The problem with this approach is that the measures for inflation expectations are imprecise and unreliable. With inflation stable and within 0.5% of target the Fed’s goal has been achieved and the central bank has turned its policies to other endeavors.

US Inflation, PCE, CPI, PPI

Consumer inflation has been remarkably stable in the US.

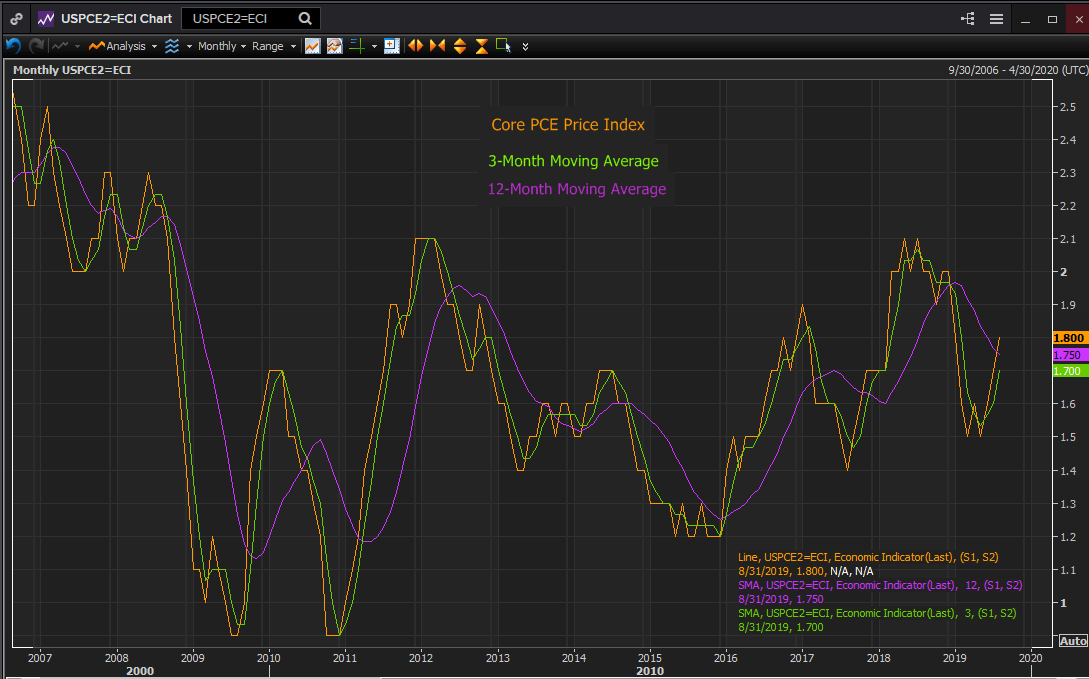

Starting in January 2012 the annual core personal consumption expenditure (PCE), the Fed’s preferred measure, has moved within a 0.9% range from 2.1% to 1.2%. The 3-month moving average has exhibited the same 0.9% variation. The 12-month moving average has wandered less than 0.7%, 0.683% to be precise, from 1.933% in June 2012 to 1.250% in December 2015. Of the 92 months in the period through August 2019, only 13 or 14% have seen core inflation at 2.0% or higher. The average core PCE inflation for the seven and a half years is 1.632%.

Reuters

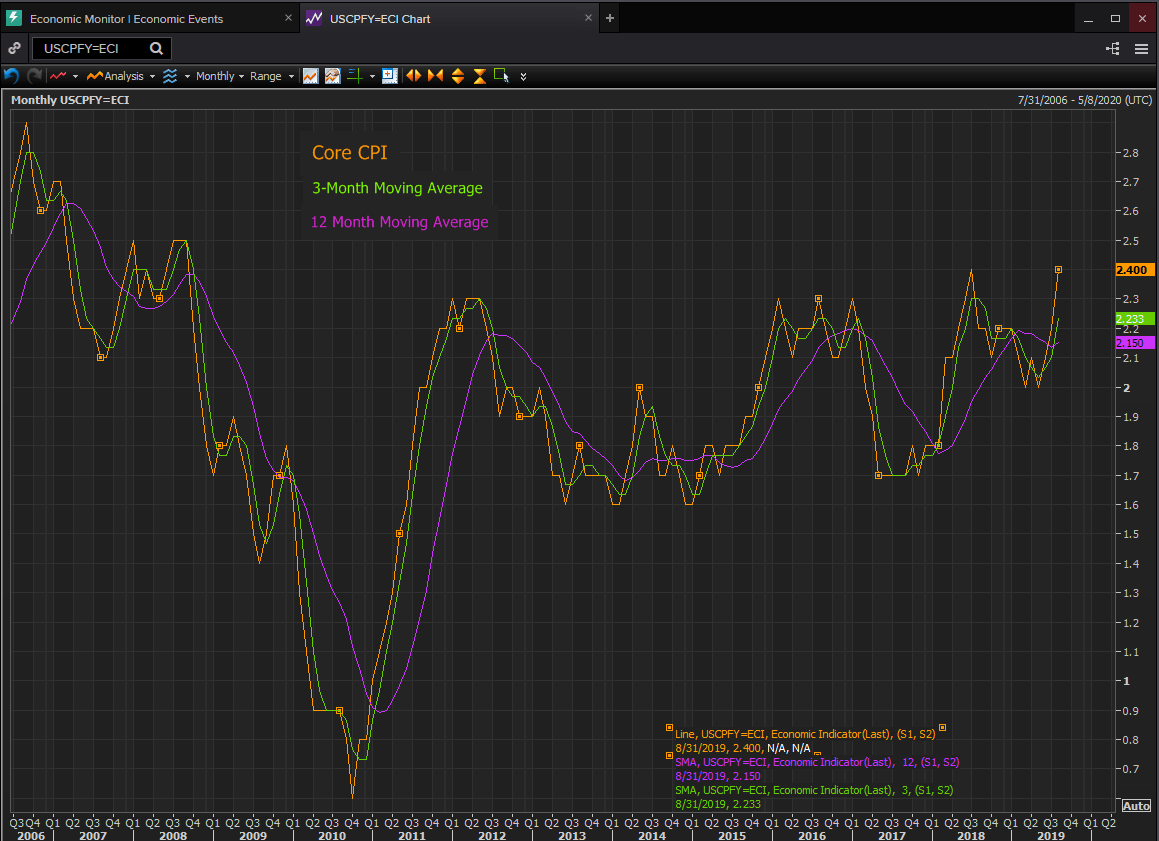

The yearly core consumer price index (CPI) an older gauge that the Fed considers less reflective of price changes in the economy, has had a similar though higher range. It has moved from 1.6% in various months in 2013, 2014 and 2015 to 2.4% in July 2018 and August 2018. The 3-month moving average range has been 1.633% to 2.3% and the 12-month one has been 1.683% to 2.2%. The average for the period from January 2012 through August 2019 is 1.963%.

Reuters

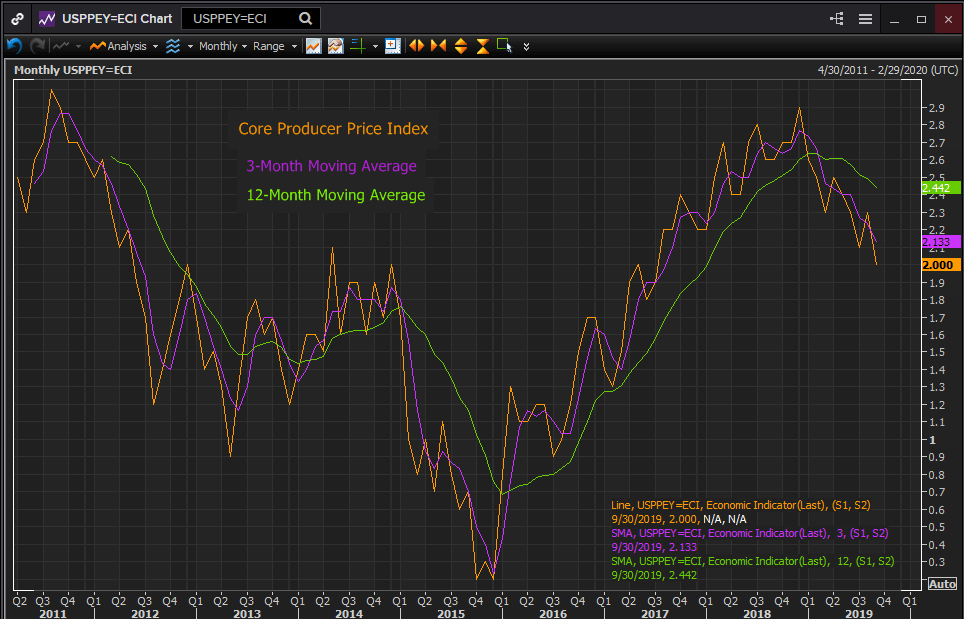

Prices at the business level have been more volatile. The annual core producer price index (PPI) has ranged from 0.2% in late 2015 to 2.9% in December 2018. The 3-month moving average has shifted from 0.233% to 2.767%; the 12-month from 0.683% to 2.633%. The average for the January 2012 to August 2019 term is 1.720%.

Reuters

The more expansive price variation for business has not carried over to consumer pricing as firms have chosen market share over short-term profits.

Inflation and Federal Reserve Policy

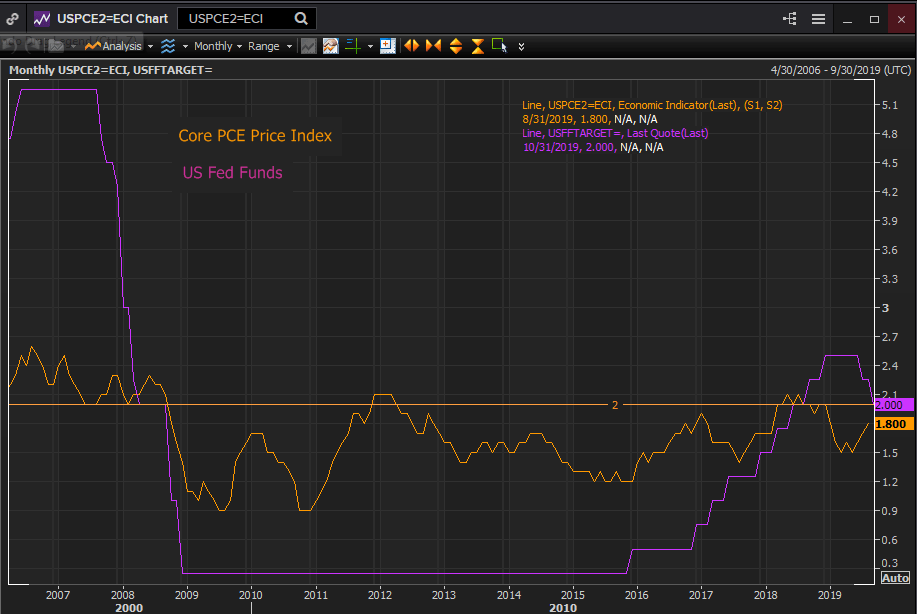

Throughout the post-recession and financial crisis decade, the Fed’s main policy focus has been economic growth. From 2008 to 2015 rate policy supported the economy and from December 2015, when rate normalization began, the economy was monitored to make certain that growth was not curtailed by rate policy.

In neither period, that of quantitative easing from 2008 to 2014 or the three years of rate increases from December 2015 to December 2018, was inflation a top priority. The core PCE rate, except in the initial two years after the recession, varied almost without reference to Fed policy. It is the same whether the Fed is pumping the economy with QE or raising the fed funds rate from 0.25% to 2.5%.

Reuters

For the best part of a decade, Fed officials have paid rhetorical attention to inflation without basing policy on it. The response to inflation variation has been uniform. The FOMC statement says that long term expectations are that inflation will be symmetric around the2.0% target. Such is repeated by Fed officials from the Chairman down.

In general, that description of US inflation has been true, if optimistic. Inflation has been steady, though weaker than the Fed’s projections.

The governors are expected to cut the fed funds rate another 25 basis points at the October 29-30 FOMC meeting. As with the last two decisions, the economic logic will not be founded on inflation. The Fed’s monetary policy is not price dependent, to borrow a popular phrase from Fed discourse.

If CPI and by implication PCE are lower than forecast, they will serve to reinforce the logic for a rate cut. If they are higher they will be discounted.

Inflation is a policy sidelight, its market impact is close to nil.

The core PCE index for September will be issued on October 31.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.