US Consumer Price Index Preview: The demand shock on prices

- Deflation expected in core and headline rates in April.

- Declining US consumption will press prices lower.

- West Texas Intermediate dropped 60% in March and April.

- Federal Reserve policies have already provided enormous liquidity to economy.

- Dollar likely to be aided by government and central bank economic support.

Working or not Americans are spending less. The great consumption machine that powers two-thirds of the US economy has been reduced to half-speed, flagged down by government orders, voluntary isolation and restrictions on almost all aspects normal life.

Demand is falling sharply and with it the cost of goods.

Consumer Price Index

The consumer price index in April is expected to drop 0.7% after fading 0.4% in March. This would be the steepest monthly drop since the height of the financial crisis when CPI plunged 0.9% in October 2008, 1.8% in November and 0.8% in December. Those three months were the deepest and fastest prices have declined in the 73 years of this series. In this entire history prices have only dropped 0.7% or more five times, the three above and 0.7% in March 1948 and 0.9% in July 1949.

Core CPI, which excludes energy and food costs, is forecast to drop 0.2% following a 0.1% slide in March. If accurate this would equal the largest monthly drop in core prices since July 1980 and November 1982. In the series which began in 1957 core prices have only fallen 0.2% in a month or more five times, the two mentioned above and 0.3%, twice in 1960 and once in 1963.

Annual CPI is expected to drop to 0.4% in April from 1.5% in March and the core rate is predicted to fall to 1.7% from 2.1%.

Demand destruction

The decline in the consumer sector that is forecast to deepen in April has put enormous pressure on retailers to reduce prices and clear inventory.

Retail sales are expected drop 10% in April after falling a record 8.4% in March, more than twice the previous low of -3.8% in October 2008. The ‘control group’ which mimics the consumption input to GDP is forecast to fall 3.9% after rising 1.7% in March. These statistics will be issued by the Census Bureau this Friday at 8:30 am EDT.

Industrial production which collapsed 5.4% in March, a 75 year record, is projected to more than double that in April at -11.6%. .

Although durable goods and personal spending for April will not be released until May 28 and 29, their March numbers, -14.8% and-7.5% were already the second largest and largest declines in their respective series. For personal spending March was more than three times the next biggest drop of 2.1% from January 1987. As with retail sales both April results are expected to be far worse.

Real personal spending, which is inflation-adjusted, fell 7.3%, the most in its 18 year history in March. The largest prior decreases were 0.9% in September 2009 and December 2018. It also is expected to follow the other metric down.

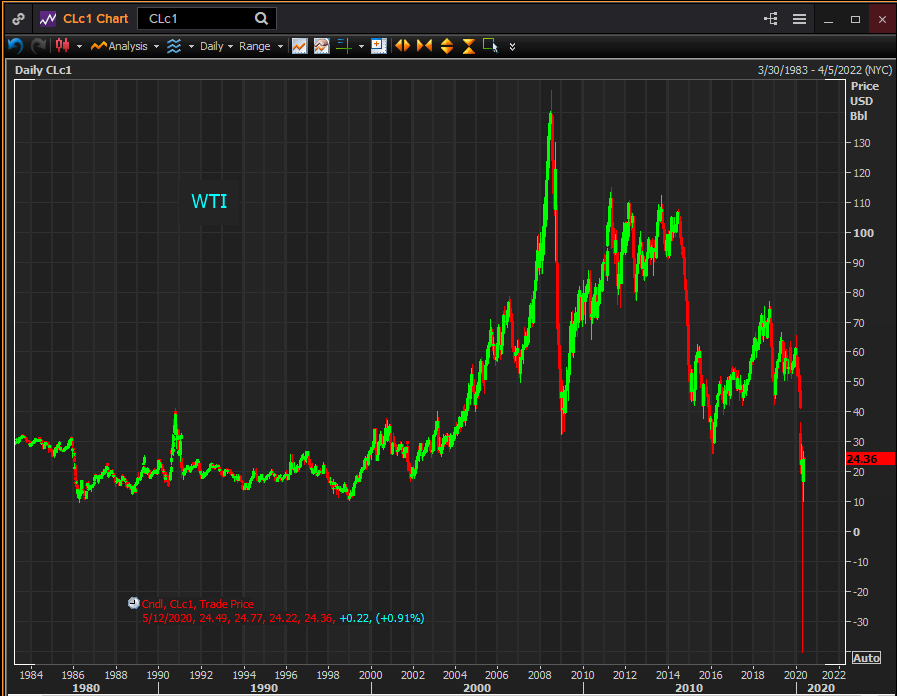

WTI

An enormous drop in demand is also behind the 60% fall in the price of West Texas Intermediate (WTI)), the North American crude standard, since the beginning of March.

Though the bulk of that decline came in March, April pricing included the run to $-37.63 on the 20th and the recovery to $18.84 by month end. That singular event will have an unknown impact on consumer prices, which have yet to see the full translation into pump prices of the overall WTI decline.

GDP

Gross domestic product contracted 4.8% in the first quarter despite the fact that the layoffs and shutdown orders did not start until mid-March and the economy had been expanding at an estimated 2.7% in January and February.

The latest estimate from the Atlanta Fed’s GDPNow model is for an astonishing 34.9% decline in the rate of annualized economic activity in the second quarter.

Fed, CPI and PCE

The central banks 2% core PCE target has mainly been met in the breach since the financial crisis. In the early days of the second round of quantitative easing in 2011 and 2012 one of the Fed’s main concerns was the potential for a damaging bout of deflation. The bank was wary lest a prolonged period of disinflation-decreasing price gains-or deflation-outright price declines-might ratchet long term inflation expectations down, making it harder and harder for the central bank to achieve its 2% target.

Between the liquidity pumped into the financial by the Fed’s quantitative easing programs and the slowly reviving economy the governors fears never materialized.

The Fed concerns this time are likely to be less pronounced.

First the shutdowns are ending and even if the return to normality is slow and fitful, the economy was strong and before the pandemic and will certainly regain a good portion of its former activity. Second the Fed and Washington have provided almost $6 trillion in financial, economic and payroll support to the US economy.

That is the same policy, zero rates and quantitative easing, prescribed by the Bernanke Fed. Jerome Powell and the current presidents started their version in early March before the economic debacle was even underway.

Conclusion: Powell rates the game

The April consumer price index will confirm the enormous impact of the economic closures on consumer pricing, whether CPI or the Fed’s preferred core PCE gauge. The central bank’s policy response has been in place for more than two months and will not change because of these anticipated deflationary months.

In the longer term, Fed policy and the dollar depend on the resilience of the US economy and consumer in this highly unusual situation. The governors, along with everyone else, are hoping for the best.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.