Big week ahead: Fed poised to cut as Canada, Australia and Switzerland hold steady

Outlook

This week we get a lot of data releases but the biggie is all those central bank decisions. Canada, Australia and Switzerland are expected to stay on hold, but the Fed is expected to cut. More important now than the decision itself is (1) who dissents and in which direction, with perhaps more members preferring a hold than last time (when it was one) (2) what Mr. Powell says at the press conference. Some smart people think he will suggest a hold for the first quarter or two as we wait for actual inflation data to show up.

Reuters calls this a "hawkish cut" and Powell’s language plus the median forecasts will “point to a higher bar for further rate reduction.

“That could support the dollar if it pushes investors to dial back expectations for two or three rate cuts next year, though messaging could be complicated by policymakers' divisions; several have already all but indicated their voting intentions.” Dissent could come from both sides, meaning a preference for zero cuts and 50 bp. “The Federal Open Market Committee has not had three or more dissents at a meeting since 2019, and it has happened just nine times since 1990.”

Well, get ready for more. We have not yet seen any hard market response to the notion Trump is going to take control of the Fed and obliterate its independence, which has been at risk many times over the past 100+ years. A Bloomberg opinion last week had it that the Fed losing independence is not of actual concern. Given the cuts (Oct and this week),

“There are some who think the Fed has already given up the fight to get back to 2%. And then layer into this the changing the political environment, where inflation fighting may get harder for various reasons.”

Looking at surveys and how people are actually conducting themselves in markets, “there’s no evidence yet that these [Fed’s loss of independence] concerns [are] actually filtering into the real world.”

Ah, if only. It’s true that markets are not showing angst over the power grab. It hasn’t happened yet. But everyone knows it’s coming. Equities don’t care because they like lower interest rates. But we have had plenty of warnings from important institutions that they fear it and are repelled by it.

It's interesting we get the Jolts report before the Fed decision, with everyone looking at layoffs but also voluntary quits. People don’t quit unless they have or think they can get another job fairly easily. Surveys shows jobs “easy to get” on the downswing but surveys are not reliable.

Forecast

The dollar is soft but remember that after the rate cuts last fall, it recovered nicely, presumably on the assumption the economy is so robust and resilient that a cut can only contribute even more fuel. From Sept 16 at 1.1189, the dollar gained to 1.0178 by Jan 13.

So, it ain’t necessarily so that rate cuts are a dollar weakener, especially if the longer yields like the 10-year stay firm and even go up. Rising yields can reflect inflation expectations but also uncertainty over a slew of policies, including the Trump power grab for the Fed. Sa, conventional thinking may have already left by the rear window. We’d stay out.

Tidbit: The BIS is concerned about a double bubble in equities and gold. Reuters reports “The combination of gold and share prices soaring in unison is a phenomenon not seen in at least half a century and raises questions of a potential bubble in both, global central bank umbrella body, the Bank for International Settlements, says.

“While equity markets continue to be driven by AI and tech gains, gold's 60% surge this year is set to be its biggest since 1979, fuelling debate about whether its traditional role as a safe-haven asset has changed.

The BIS top asset guys says "The interesting phenomenon this time has been that gold has become much more like a speculative asset."

Reuters: “Where would investors shelter if stocks and gold both crash. And what could it mean for central banks and other reserve managers given some have been heavy buyers of gold. The BIS' analysis concluded that this year has been the first time gold and the S&P 500 have jointly exhibited ‘explosive behaviour’ in the last 50 years.

“Not only is gold up 60% this year, it is up more than 150% since 2022 when the post-COVID pandemic surge in inflation began to impact markets, alongside Russia's invasion of Ukraine and subsequent Western sanctions on Moscow.”

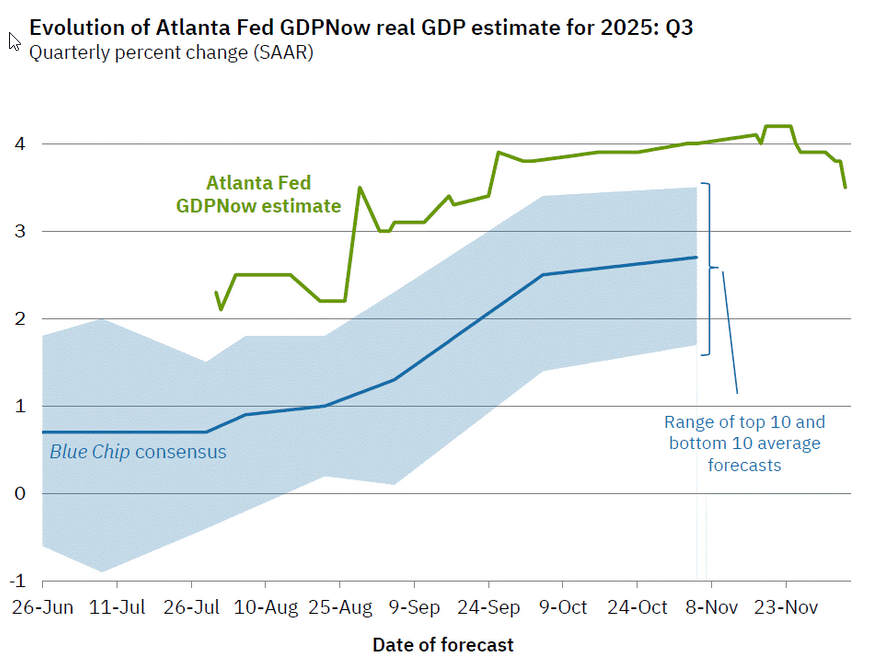

Tidbit: Does main Fed look at the Atlanta Fed GDPNow? Plenty of regional Feds come out with forecasts, of which the Atlanta and Cleveland Feds are probably the leaders. Last week the Atlanta Fed issued a Q3 GDPNow showing a drop from 3.8% on Dec 4 to 3.5% on Dec 5 due to a drop in personal consumption growth from 3.1% to 2.7%. We get another one “no later than Thursday, Dec 11” and the first model for Q4 not before Dec 23.

Can you get high growth with falling employment? Sure, if a rise in productivity offsets.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat