US Consumer Price Index March Preview: Federal Reserve policy affirmed

- CPI forecast to climb to 8.5% annually, 6.6% for core.

- Prices expected to jump 1.2% and 0.5% for the month.

- Odds for a 0.5% hike at May 4 FOMC over 80%.

- Markets are undecided if expansion can continue under higher interest rates.

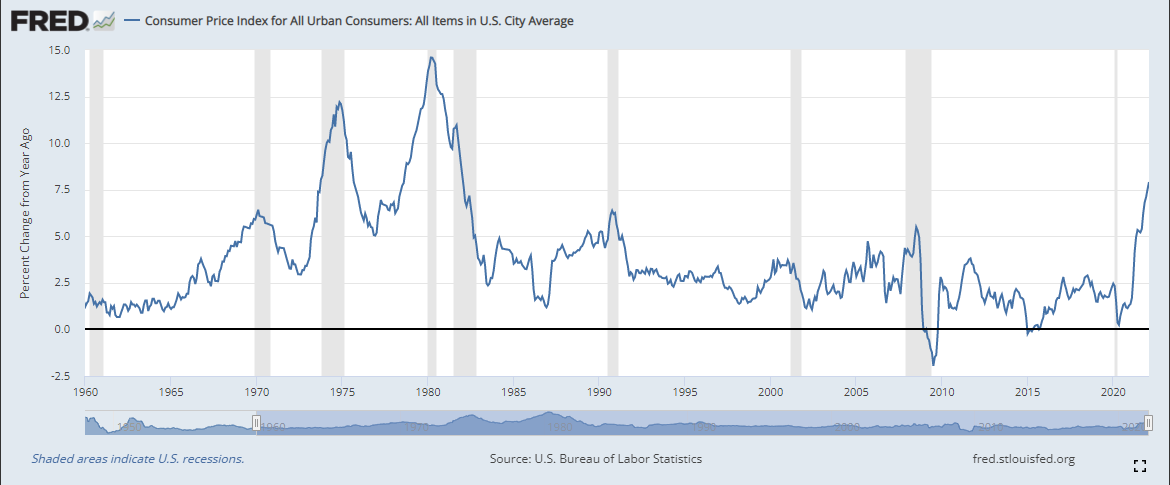

Inflation is set to give Federal Reserve policy a ringing endorsement, rising to a new forty-year record for the fourth month in a row.

The Consumer Price Index (CPI) is forecast to jump 1.2% in March, soaring to 8.5% for the year from 7.9% in February. That would be the fastest rate of price appreciation since 8.3% in January 1982. In January 2021 CPI was 1.4%.

The core index is expected to climb 0.5% in March bringing the annual rate to 6.6%, up from 6.4% in February. In January 2021 core CPI was 1.4%

Federal Reserve and Treasury yields

Federal Reserve monetary and economic policy has executed a complete reversal in the last four months. It was only on November 30 that Fed Chair Jerome Powell told a Congressional hearing, "it’s probably a good time to retire that word (transitory) and try to explain more clearly what we mean.”

Since then the Fed has ended its bond-buying program, raised the fed funds rate 0.25%, with a prospective 0.5% increase next month, and suggested, though not announced, a $95 billion reduction in its balance sheet each month.

Treasury rates have been even more emphatic in their assertion than official policy. From the open on that November Tuesday when Mr. Powell and Treasury Secretary Janet Yellen spoke to Congress, the Treasury yield curve has moved sharply higher, with the ascent at the short end of the spectrum one of the steepest on record.

The 2-year yield has added 198 points to 2.491% as of Monday morning in New York. The 10-year has jumped 124 points to 2.769% and the 30-year has climbed 91 points to 2.785%.

2-year Treasury yield

CNBC

The yields on the 2-year, 10-year and 30-year Treasuries have moved well beyond their positions in March 2020 at the start of the pandemic.

10-year Treasury yield

CNBC

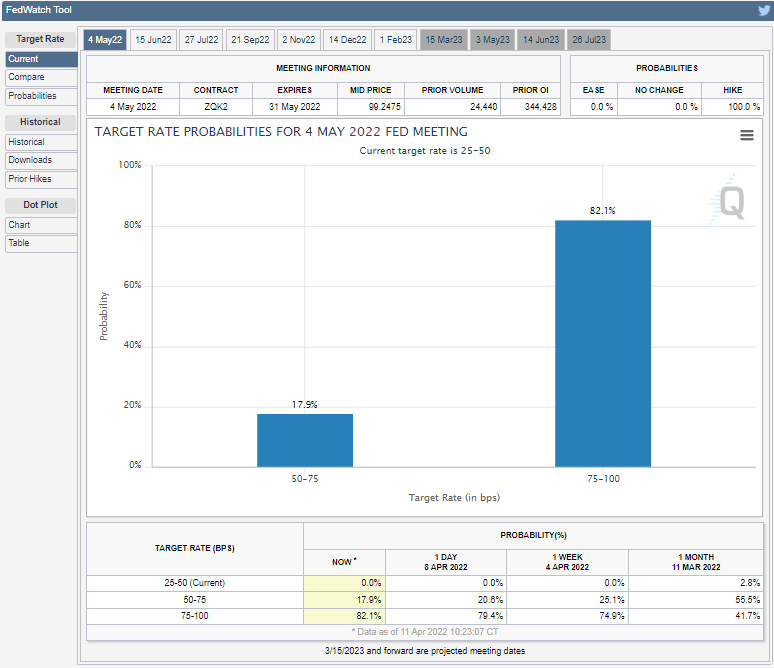

Treasury futures have the probability for a 0.5% increase at the May 4 Federal Open Market Committee (FOMC) at 82.1%. By the end of the year, credit markets expect the fed funds rate to be between 2.50% and 2.75%, implying 2.25% in total increases or the equivalent of nine 0.25% hikes.

CME FedWatch

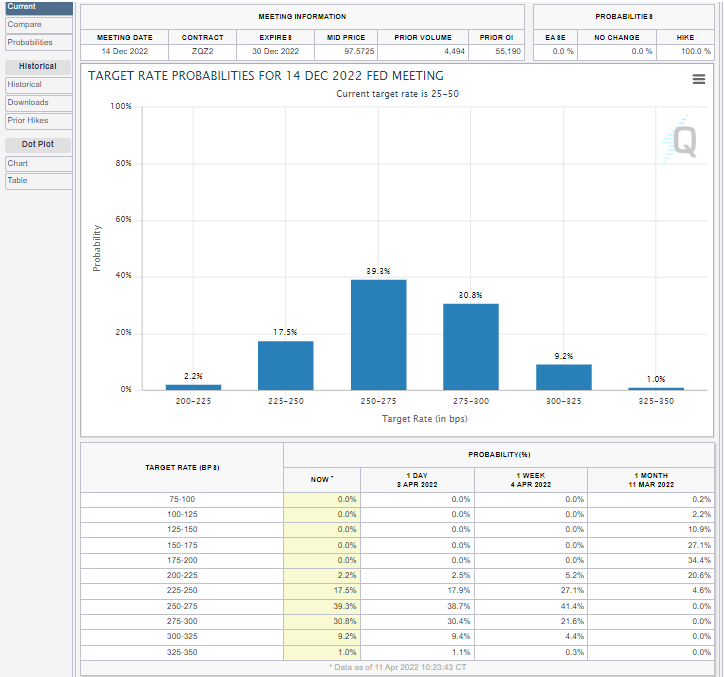

The odds for this outcome are 83.7%. The Fed own estimate, released at the March 16 meeting, has the year-end rate at 1.9% and the central tendency, which eliminates the three highest and lowest projections, at 1.6% to 2.4%.

CME FedWatch

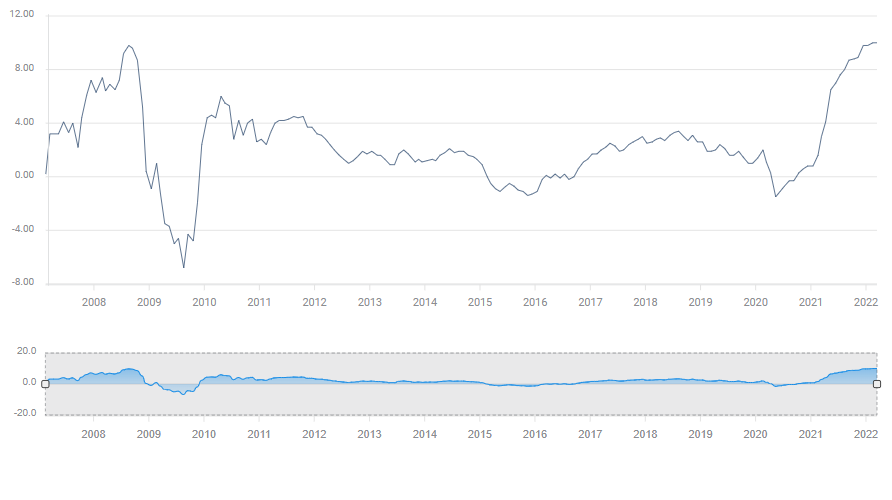

Producer Price Index

As rampant as consumer inflation has been over the past year, the Producer Price Index (PPI), which tracks manufacturing commodity costs, is still accelerating. This promises more retail pain ahead. Producer prices are predicted to rise 1.1% in March, up from 0.8% in February. Over the past 12 months increases have averaged 0.8%. Annual PPI is expected to rise to 10.5% in March from February’s 10.0%. From November 2021 PPI has averaged 9.9% a month, higher than the previous peak in July 2008 of 9.8%.

PPI

In January 2021 PPI was 1.6%. The increase to 10% in February is 625%. An identical gain in CPI would put the March rate at 8.75%.

Core PPI is projected to rise 0.5% on the month, up from 0.2% in February and to be unchanged for the year at 8.4%. The March PPI data will be released on Wednesday April 13.

Federal Reserve and markets

Rising inflation reinforces the Fed’s newly minted rate policy. As long as consumer prices continue to accelerate, markets will offer little resistance to the central bank’s prescription for fighting inflation.

The fear that higher rates could trigger an economic slowdown or recession is balanced by the concern that ever-rising consumer prices will themselves force a cutback in consumption that could have the same negative result on growth. Retail Sales and Personal Consumption Expenditures were soft in February but are projected to rebound in March.

Retail Sales

Interest rate policy works to restrict inflation with a six to 12-month delay. The Fed’s policy dilemma is that inflation may cut sharply into consumer spending long before its rate hikes can have the least chance of damping price increases. Fed governors are hoping to short-circuit inflation expectations before they become embedded in a reinforcing wage-price spiral and betting that consumers will continue to spend until inflation subsides.

Dollar strength and Treasury yields are two sides of the same coin. Since Fed Chair Powell's ‘transitory’ comment last November, the Dollar Index has gained 3.7%.

Movement in the major pairs has been split between the commodity currencies, the loonie, aussie and kiwi, which have risen on soaring materials prices and the euro, sterling, yen and Swiss franc which have all lost ground against the dollar.

Equities have recovered dramatically from the pandemic collapse in March 2020. Higher interest rates are not necessarily a determinant of lower stock prices, if the global economy can sustain a recovery despite interest rates approaching their historical norms.

The Russian invasion of Ukraine has scrambled markets but with the conflict appearing headed toward stalemate, oil prices have rescinded most of their war premium. China's draconian Covid lockdowns may drag her economy and the world into recession.

There is uncertainty aplenty in the economic future. Unfortunately, US inflation has ensured there is none about Federal Reserve policy.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.