US Conference Board Consumer Confidence September Preview: Neither happy nor sad

- Consumer Confidence expected to rise to 89.2 in September.

- Michigan Consumer Sentiment at 78.9 this month, a post-lockdown high.

- Retail Sales slowed in August, six month average 0.87%.

- Currency markets view sentiment numbers as background.

American consumer attitudes have recovered from their April pandemic low but they remain stalled far below their levels of last year.

The Conference Board (CB) Consumer Confidence Index is predicted to rise to 89.2 in September. August’s reading of 84.8 was the lowest of the lockdown era and aftermath and a surprise drop below the April score of 85.7.

In February, before the closures began, the CB Consumer Confidence Index registered 132.6, that fell to 118.8 in March then the April result mentioned above. By June the outlook had jumped to June to 98.3 the highest post-closure but then it slipped to 91.7 in July.

American’s have neither panicked over the virus nor have they returned to their normal optimism.

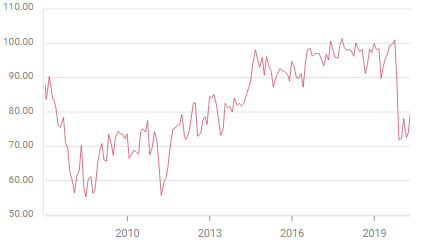

Michigan Consumer Sentiment

Consumer outlook in the Michigan Survey Index was 78.9 in September, up from the pandemic low of 71.8 in April but, like its older counterpart from the Conference Board, well beneath the February listing at 101.

The range since the pandemic struck in March is similar to that of 2012 through 2014 and higher than the three years after the financial crash of 2008-2009.

Michigan Consumer Sentiment

Non-farm Payrolls vs Initial Claims

Employment is the most important factor in consumer attitudes. If jobs are plentiful and wages rising consumers respond with the purchases that drive the economy.

Payrolls have recovered about half of the jobs lost during the shutdown months and government support measures have helped maintain consumption.

But despite the return of many workers layoffs have continued at nearly one million a week since they began in late March. In the week of September 11 the four-week moving average was 912,000, the lowest it has been since the crash but higher than in any previous week on record including the peak of the financial crisis a decade ago.

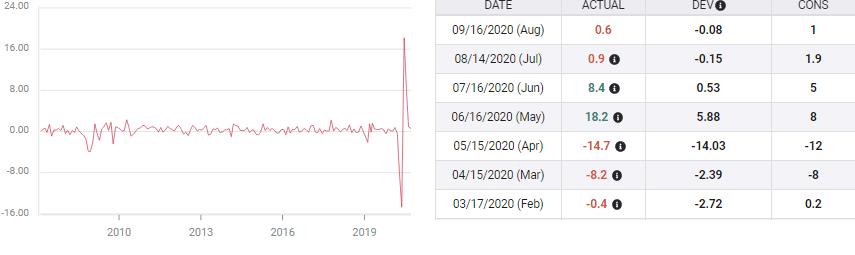

Retail Sales

Sales slowed in August, rising 0.6% on a 1% forecast and down from July’s 0.9% gain.

In normal times a 0.6% increase, a six-month average of 0.87% and an overall gain of 5.2% for half-a-year would be evidence of a robust if not booming consumer economy.

Retail Sales

The May and June rebound in sales was not surprising, large sections of the US economy were closed in March and April but life did not halt, it was just on hold. More important will be the continuation into September and the fourth quarter. If the July and August reductions are not a return to normal levels of consumption but a declining trend that manifests into the Christmas season then the prognosis for the US economy will darken considerably.

The September Retails Sales numbers will be issued by the Commerce Department on Friday October 16.

Conclusion and markets

Consumer sentiment numbers are background information. Even though consumption is about 70% of US economic activity it is the direct readings from Retail Sales and Personal Consumption Expenditures that move markets.

With the Michigan sentiment number already released, little deviation is expected from the Conference Board result. American consumers have yet to regain their verve. Markets are waiting.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.